PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907341

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907341

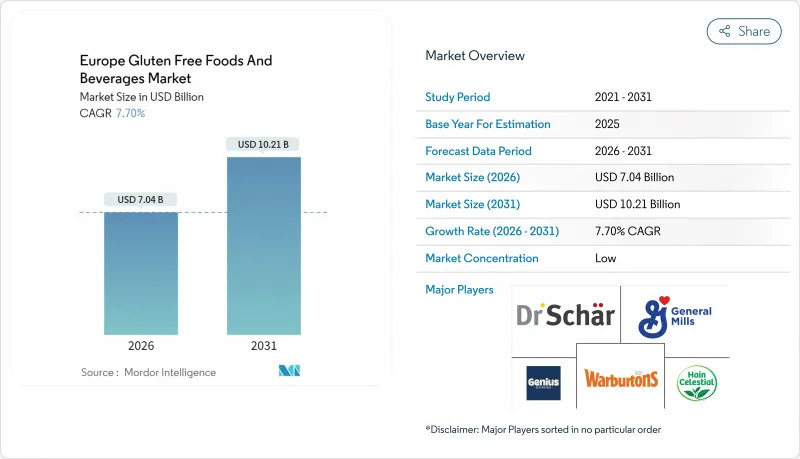

Europe Gluten Free Foods And Beverages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe gluten-free foods and Beverages Market is expected to grow from USD 6.54 billion in 2025 to USD 7.04 billion in 2026 and is forecast to reach USD 10.21 billion by 2031 at 7.7% CAGR over 2026-2031.

This growth trajectory reflects the convergence of medical necessity and lifestyle adoption, as over 5 million Europeans live with celiac disease requiring strict gluten-free diets. The market's expansion is further amplified by the broader population embracing gluten-free options for perceived health benefits, despite price premiums that can exceed 300% compared to conventional alternatives for staple foods.

Europe Gluten Free Foods And Beverages Market Trends and Insights

Rising Prevalence of Celiac and Non-Celiac Gluten-Sensitivity

Celiac disease affects a notable portion of the European population, with regional differences in prevalence and rising incidence, particularly among young women and older adults. Despite this trend, a significant diagnostic gap persists, indicating a large number of undiagnosed cases and highlighting the potential impact of expanded screening programs. Beyond medically diagnosed celiac disease, non-celiac gluten sensitivity contributes to a broader consumer base seeking gluten-free options. This growing demand is further supported by healthcare professionals who increasingly advocate for early dietary intervention to mitigate long-term health risks such as bone density loss and certain malignancies.

Growing Mainstream Awareness and Healthy-Eating Positioning

Consumer perception of gluten-free products has evolved beyond medical necessity to encompass wellness lifestyle choices. While celiac disease patients require strict gluten-free diets, these products now attract consumers without medical conditions. This broader market acceptance creates growth opportunities but increases competition for retail visibility. The market also benefits from overlapping consumer interest in gluten-free and plant-based products, which strengthens demand in both segments. . Marketing strategies increasingly emphasize nutritional benefits and lifestyle alignment rather than medical compliance. However, this trend also creates challenges in maintaining product authenticity and managing consumer expectations regarding taste and texture compared to conventional alternatives.

Premium Price Positioning Limits Mass Adoption

Gluten-free products command significant price premiums, with staple foods costing 300-400% more than conventional equivalents, creating affordability barriers that restrict market penetration beyond medically necessary consumers. Portuguese market research reveals that high prices and limited product variety represent primary challenges for gluten-free adoption, particularly affecting bread and pastry categories. The cost differential stems from specialized production facilities, smaller batch sizes, alternative ingredient sourcing, and certification requirements that increase manufacturing complexity. Polish celiac patients report significant accessibility issues in urban areas, with cost constraints contributing to adherence challenges and limiting dietary variety. Economic pressures from inflation and global trade tensions further exacerbate affordability concerns, potentially constraining market expansion among price-sensitive consumer segments despite growing health awareness.

Other drivers and restraints analyzed in the detailed report include:

- Expansion in Product Innovation

- Enhanced Labelling Regulations and Certification Schemes

- Micronutrient Gaps in Many Gluten-Free Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bakery products command 44.78% market share in 2025, reflecting consumer prioritization of bread alternatives and technological advances addressing traditional texture limitations. Increasing innovative product launches demonstrate continued innovation in this dominant segment. Beverages emerge as the fastest-growing segment at 8.85% CAGR through 2031, driven by innovations in oat-based beers utilizing lactic acid bacteria to reduce immunoreactivity for celiac patients. Meats and meat substitutes benefit from plant-based convergence trends, while dairy and dairy substitutes capitalize on lactose-free crossover demand.

Sauces, dressings, and seasonings represent stable growth opportunities through clean-label reformulations, while snacks and ready-to-eat products gain traction via convenience positioning. The "Other Product Types" category encompasses emerging innovations including 3D-printed alternatives and novel protein sources approved under EU regulations. Recent research on gluten-free pasta formulations using brown rice, quinoa, and chickpea flours demonstrates segment evolution toward nutritionally enhanced offerings. Regulatory compliance under EU food additive specifications affects formulation strategies across all product categories, particularly for texture-enhancing ingredients.

The Europe Gluten Free Foods and Beverages Market Report is Segmented by Product Type (Bakery Products, Meats/Meat Substitutes, Dairy/Dairy Substitutes, and More), Nature (Conventional, Organic), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Distribution Channels), and Geography (Germany, United Kingdom, France, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Dr. Schar AG/SPA

- General Mills Inc.

- Warburtons Ltd (Gluten-Free)

- Genius Foods Ltd

- Hain Celestial Group

- Conagra Brands Inc.

- Nestle SA (Cereal Partners, Maggi GF)

- Amy's Kitchen Inc.

- Bob's Red Mill Natural Foods

- Barilla Group (Mulino Bianco GF)

- Kraft Heinz Company

- Kellogg Company

- Hero Group (Juvela)

- Dawn Foods

- London Food Corporation

- Golden West Specialty Foods

- Scharbackerei GmbH (Austria)

- Grupo Airos (Spain)

- Freee Foods Ltd (Doves Farm)

- Beneo GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of celiac and non-celiac gluten-sensitivity

- 4.2.2 Growing mainstream awareness and healthy-eating positioning

- 4.2.3 Expansion in product innovation

- 4.2.4 Enhanced labelling regulations and certification schemes

- 4.2.5 Growth of "clean label" and functional foods

- 4.2.6 Rapid growth in plant-based, vegan, and "free-from" foods

- 4.3 Market Restraints

- 4.3.1 Premium price positioning limits mass adoption

- 4.3.2 Micronutrient gaps in many gluten-free formulations

- 4.3.3 Raw-material supply volatility (teff, sorghum, quinoa)

- 4.3.4 Taste, texture, and sensory limitations

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bakery Products

- 5.1.2 Meats/Meat Substitutes

- 5.1.3 Dairy/Dairy Substitutes

- 5.1.4 Sauces, Dressings, and Seasonings

- 5.1.5 Snacks and RTE Products

- 5.1.6 Beverages

- 5.1.7 Other Product Types

- 5.2 By Nature

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Specialty Stores

- 5.3.3 Online Retail

- 5.3.4 Other Distribution Channels

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Netherlands

- 5.4.8 Switzerland

- 5.4.9 Belgium

- 5.4.10 Austria

- 5.4.11 Portugal

- 5.4.12 Denmark

- 5.4.13 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.4.1 Dr. Schar AG/SPA

- 6.4.2 General Mills Inc.

- 6.4.3 Warburtons Ltd (Gluten-Free)

- 6.4.4 Genius Foods Ltd

- 6.4.5 Hain Celestial Group

- 6.4.6 Conagra Brands Inc.

- 6.4.7 Nestle SA (Cereal Partners, Maggi GF)

- 6.4.8 Amy's Kitchen Inc.

- 6.4.9 Bob's Red Mill Natural Foods

- 6.4.10 Barilla Group (Mulino Bianco GF)

- 6.4.11 Kraft Heinz Company

- 6.4.12 Kellogg Company

- 6.4.13 Hero Group (Juvela)

- 6.4.14 Dawn Foods

- 6.4.15 London Food Corporation

- 6.4.16 Golden West Specialty Foods

- 6.4.17 Scharbackerei GmbH (Austria)

- 6.4.18 Grupo Airos (Spain)

- 6.4.19 Freee Foods Ltd (Doves Farm)

- 6.4.20 Beneo GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK