PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907352

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907352

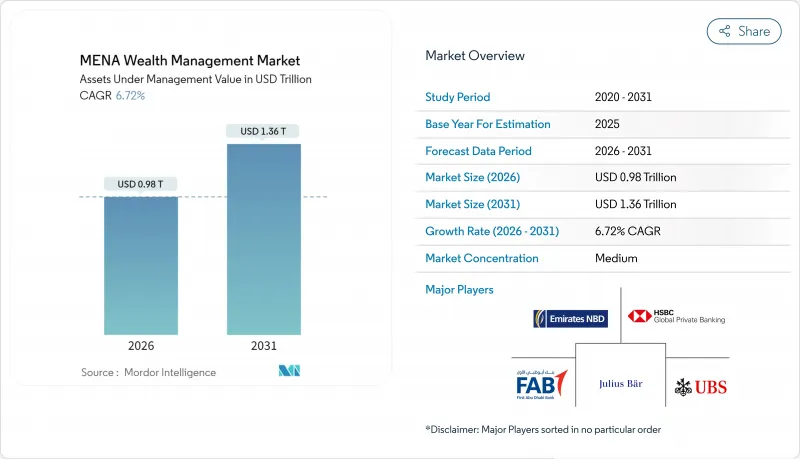

MENA Wealth Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The MENA wealth management market is expected to grow from USD 0.92 trillion in 2025 to USD 0.98 trillion in 2026 and is forecast to reach USD 1.36 trillion by 2031 at 6.72% CAGR over 2026-2031.

The outlook benefits from sovereign-wealth diversification mandates that funnel hydrocarbon earnings into structured advisory products, policy frameworks that levy zero personal tax in UAE and Saudi Arabia, and regulatory sandboxes that fast-track tokenized investment funds. Intensifying millionaire migration to economic zones in Dubai, Abu Dhabi, and Riyadh fortifies the regional asset base while Shariah-compliant robo-advisory tools expand coverage among mass-affluent savers. Competitive behavior centers on hybrid advisory models that merge human expertise with automated screening and portfolio construction. The rise of environmental, social, and governance mandates plus gender-inclusive entrepreneurship programs broadens the potential client pool and supports strong revenue momentum over the forecast horizon.

MENA Wealth Management Market Trends and Insights

Gulf HNWI In-Migration Accelerates Onshore AUM Growth

Zero-tax residency programs in the UAE and Saudi Arabia drive unprecedented millionaire migration, with the UAE expected to attract 9,800 high-net-worth individuals in 2025 alone. This influx creates immediate demand for sophisticated wealth structuring services, family office establishment, and cross-border tax optimization strategies that local private banks are rapidly scaling to capture. The Dubai International Financial Centre processed over 200 new family office applications in 2024, representing a 40% increase from the previous year. Saudi Arabia's Riyadh International Financial District similarly targets 500 licensed financial services firms by 2030, creating competitive pressure on established UAE hubs. This geographic arbitrage fundamentally reshapes regional AUM distribution patterns as wealth managers establish dual-hub strategies to serve mobile HNWI clients.

Sovereign Wealth Diversification Mandates Reshape Private Banking

Gulf sovereign wealth funds increasingly mandate private banking relationships for their diversification strategies, moving beyond traditional asset management toward structured products and alternative investments. The Saudi Public Investment Fund's allocation to private markets reached 30% in 2024, while ADIA expanded its private wealth co-investment programs with regional family offices. This institutional-to-private wealth crossover creates new revenue streams for private banks that can bridge sovereign capital with HNWI investment opportunities. Abu Dhabi Investment Authority's partnership with local private banks for co-investment vehicles demonstrates how sovereign capital increasingly flows through private banking channels rather than direct institutional mandates. The trend accelerates as oil-dependent economies seek to create sustainable wealth management ecosystems beyond hydrocarbon revenues.

Geopolitical Flashpoints Create Compliance Cost Escalation

Regional conflicts and sanctions regimes impose escalating compliance costs on MENA wealth managers, with some institutions reporting 40% increases in anti-money laundering and sanctions screening expenses during 2024. Enhanced due diligence requirements for clients with regional business interests create onboarding delays averaging 45 days compared to 15 days for European clients, according to HSBC Private Bank's regional compliance reports. The U.S. Treasury's Office of Foreign Assets Control expanded secondary sanctions risks for financial institutions serving certain Middle Eastern markets, forcing some global private banks to restrict services to regional clients. Swiss private banks operating in DIFC implemented additional client screening protocols that increased operational costs by 25% while reducing client acquisition rates. These compliance burdens disproportionately affect smaller regional players who lack the technology infrastructure to efficiently manage complex sanctions screening requirements.

Other drivers and restraints analyzed in the detailed report include:

- Islamic Digital Wealth Platforms Democratize Shariah-Compliant Investing

- Inter-Generational USD 2 Trillion Wealth Transfer Reshapes Advisory Demand

- Regulatory Fragmentation Impedes Cross-Border Islamic Finance Scaling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-net-worth individuals maintain commanding market leadership with a 54.10% share in 2025, yet retail investors emerge as the transformation catalyst with a 11.78% CAGR through 2031. The HNWI segment benefits from the UAE's golden visa program and Saudi Arabia's premium residency scheme, which attracted over 15,000 millionaire families to the region in 2024. Traditional relationship-driven advisory models serve this segment through private banking arms of Emirates NBD, FAB, and international players like UBS and Julius Baer. However, next-generation HNWI clients increasingly demand technology-enabled solutions, forcing private banks to invest heavily in digital advisory platforms and ESG-compliant investment products.

Retail investors represent the market's digital frontier, with platforms like Sarwa and StashAway democratizing wealth management access through Shariah-compliant robo-advisory services that require minimum investments as low as USD 500. The Dubai Financial Services Authority's regulatory sandbox enabled 12 new retail-focused Islamic fintech platforms in 2024, while Saudi Arabia's Capital Market Authority streamlined licensing for mass-market advisory services. Other institutional clients, including pension funds and insurance companies, maintain steady growth patterns but face regulatory constraints that limit cross-border investment mandates. The segmentation shift reflects broader financial inclusion initiatives across GCC economies seeking to reduce oil dependency through diversified savings and investment behaviors.

The MENA Wealth Management Market Report is Segmented by Client Type (HNWI, Retail/Individuals, Other Client Types), Provider (Private Banks, Independent/External Asset Managers, Family Offices, Other Providers), and Geography (GCC, North Africa, Levant, Turkey, Iran & Iraq). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Emirates NBD Private Banking

- First Abu Dhabi Bank (FAB) Private Banking

- HSBC Global Private Banking - MENA

- UBS Global Wealth Management - Middle East

- Julius Baer Middle East

- BNP Paribas Wealth Management Gulf

- Credit Suisse (UBS) MENA

- Citi Private Bank - MENA

- Lombard Odier Middle East

- Goldman Sachs PWM - GCC

- Standard Chartered Private Bank MENA

- Bank of Saudi Fransi Elite

- Samba Private Banking

- Al Rajhi Capital Wealth

- QNB Private

- Mashreq Private Banking

- Sarwa

- StashAway Reserve

- ADCB Private & Wealth

- DIFC-based Single-Family Offices (aggregate)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gulf HNWI in-migration to UAE & Saudi economic zones

- 4.2.2 Sovereign-wealth diversification boosting on-shore AUM

- 4.2.3 Rapid rise of Islamic digital-wealth platforms

- 4.2.4 Inter-generational USD 2 tn GCC wealth transfer wave

- 4.2.5 Female entrepreneurship and rising women-controlled assets

- 4.2.6 DIFC/ADGM sandbox pipelines for tokenised funds

- 4.3 Market Restraints

- 4.3.1 Geopolitical flashpoints & sanctions spill-over risk

- 4.3.2 Oil-price volatility affecting liquidity creation

- 4.3.3 Fragmented Shariah & cross-border regulatory regimes

- 4.3.4 Shortage of Arabic-speaking certified wealth advisers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Client Type

- 5.1.1 HNWI

- 5.1.2 Retail / Individuals

- 5.1.3 Other Client Types (Pension Funds, Insurers, etc.)

- 5.2 By Provider

- 5.2.1 Private Banks

- 5.2.2 Family Offices

- 5.2.3 Others (Independent/External Asset Managers)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Emirates NBD Private Banking

- 6.4.2 First Abu Dhabi Bank (FAB) Private Banking

- 6.4.3 HSBC Global Private Banking - MENA

- 6.4.4 UBS Global Wealth Management - Middle East

- 6.4.5 Julius Baer Middle East

- 6.4.6 BNP Paribas Wealth Management Gulf

- 6.4.7 Credit Suisse (UBS) MENA

- 6.4.8 Citi Private Bank - MENA

- 6.4.9 Lombard Odier Middle East

- 6.4.10 Goldman Sachs PWM - GCC

- 6.4.11 Standard Chartered Private Bank MENA

- 6.4.12 Bank of Saudi Fransi Elite

- 6.4.13 Samba Private Banking

- 6.4.14 Al Rajhi Capital Wealth

- 6.4.15 QNB Private

- 6.4.16 Mashreq Private Banking

- 6.4.17 Sarwa

- 6.4.18 StashAway Reserve

- 6.4.19 ADCB Private & Wealth

- 6.4.20 DIFC-based Single-Family Offices (aggregate)

7 Market Opportunities & Future Outlook

- 7.1 Tokenised sukuk & private-credit funds for mass-affluent investors

- 7.2 Riyadh's new International Wealth Hub attracting global managers