PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910435

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910435

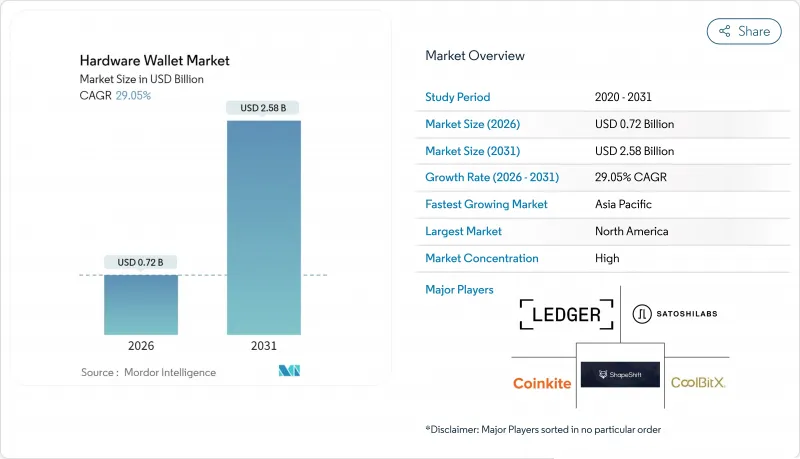

Hardware Wallet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The hardware wallet market was valued at USD 0.56 billion in 2025 and estimated to grow from USD 0.72 billion in 2026 to reach USD 2.58 billion by 2031, at a CAGR of 29.05% during the forecast period (2026-2031).

A sharp pivot by asset managers toward self-custody, an upsurge in high-profile exchange breaches, and clarity from frameworks such as MiCA and the OCC have together created a durable demand runway for the hardware wallet market. Enterprise clients now drive larger order values as they replace custodial accounts with on-premises key-management appliances, forcing formerly consumer-centric vendors to upgrade certification levels and professional-service offerings. The hardware wallet market also benefits from manufacturers localizing secure-element production after tariff shocks, and from multi-chain DeFi activity that rewards devices able to sign transactions across numerous layer-1 and layer-2 networks. Competitive conditions remain fluid because multi-year venture funding lets new entrants experiment with form factors, yet certification costs and supply-chain control continue to favor incumbents with deeper capital pools.

Global Hardware Wallet Market Trends and Insights

Intensifying Institutional Adoption of Self-Custody Solutions

Organizations now treat digital assets as treasury items rather than speculative holdings, so decision-makers reject omnibus custody in favor of deterministic control that satisfies board-level risk appetites. This change explains why the hardware wallet market increasingly revolves around FIPS-certified secure elements, REST-based signing stacks, and SOC-2 reporting layers. Dfns illustrates the shift by raising USD 16 million to scale wallet-as-a-service infrastructure that supports Fidelity International and Zodia Custody. Enterprise adoption raises average selling prices, lengthens replacement cycles, and nudges vendors toward subscription models bundling firmware updates, attestation services, and hardware warranties. In parallel, systems integrators extend device life by embedding wallets in HSM racks or zero-trust enclaves, widening the addressable hardware wallet market.

Surge in Cyber-Breach Publicity Pushing Demand for Offline Keys

Crypto theft reached signficantly, reigniting awareness of hot-wallet attack surfaces. Incidents at Bybit and Phemex triggered emergency asset migrations that overloaded consumer-grade devices, exposing feature gaps in backup verification and key-sharding workflows. Vendors responded by showcasing Common Criteria EAL5+ chips, epoxy-filled enclosures, and tamper-evident holograms that underline offline resilience. Marketing campaigns play on the cognitive impact of breach headlines, repeatedly framing air-gapped storage as the last line of defense between treasury assets and state-linked exploit groups. The resulting brand equity further entrenches device use among family offices and exchange-traded-product sponsors, expanding the hardware wallet market beyond technology enthusiasts.

Evolving AML/KYC Mandates Raising Compliance Costs

Regulators now ask hardware suppliers to embed mechanisms that flag sanctioned addresses, impose address-screening APIs, and log suspicious activity across device fleets. Implementing these functions adds firmware overhead, demands regular list updates, and exposes vendors to data-protection liability. Start-ups lacking legal teams often outsource compliance to cloud scorers, inflating unit economics and stretching working capital. Stringent cross-border export classifications for cryptographic modules further complicate logistics, delaying shipment into high-growth corridors and slowing the hardware wallet market momentum. Meanwhile, established manufacturers lean on pre-existing FATF audit files to maintain global reach at a lower marginal compliance outlay.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Segregated Crypto Custody (MiCA, OCC)

- Expanding DeFi and NFT Ecosystems Requiring Multi-Chain Support

- Persistent Consumer UX Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

USB connectivity retained a 46.98% slice of the hardware wallet market in 2025, underpinned by its air-gapped lineage and minimal attack surface. NFC devices, however, are racing ahead at a 29.62% CAGR as consumers align crypto spending with contactless habits honed on Apple Pay and PayNow. Vendors like Arculus and Sugi shape the discussion by enclosing secure elements in sleek cards that slip into normal wallets, and by enabling tap-to-sign workflows that appeal to shoppers scanning QR codes at point-of-sale. The hardware wallet market size attributable to NFC is therefore expected to surge as super-apps in Southeast Asia enroll merchants that now accept stablecoin micropayments.

Institutional desks still prefer physical cables to reduce radio-frequency leakage and to preserve deterministic paths during SOC-2 audits. Even so, next-generation air-gap solutions adapt NFC in a stateless manner that permits external secure-element attestation without exposing private keys. Regulatory oversight may tilt further once standards bodies like ISO/TC 68 publish final guidelines on NFC-enabled custody. For now, vendors hedge bets by offering tri-modal SKUs, USB, NFC, and Bluetooth, to cover every operational context, thereby preventing channel cannibalization and growing their total addressable share of the hardware wallet market.

Hot wallets dominated early user behavior, grabbing 62.78% hardware wallet market share in 2025 thanks to plug-and-play swaps and decentralized-exchange farming incentives. Yet the asset-wipe headlines of 2024 have pushed fiduciaries toward cold environments that record a 29.85% CAGR through 2031 as boards assign quantitative risk scores to each custody model. That trend lifts the hardware wallet market size devoted to air-gapped vaults, including bunker-installed HSM racks equipped with secure-element blades designed to withstand physical intrusion.

Hybrid designs blur boundaries by allowing "warm" states that temporarily expose signing rights under M-of-N quorum approval, then revert to cold once sweeps finish. This controlled activation fits treasury playbooks that disburse payroll in USDC yet store reserves offline. In emerging capital-market mandates, MiCA interprets cold storage as the reference architecture for reserve verification, further amplifying unit demand. Vendors monetizing the shift receive elevated gross margins because every cold-wallet SKU ships with additional Faraday-cage sleeves, epoxy-sealed PCBs, and high-pixel-density screens required to display full-length smart-contract call data, sustaining profitability inside the hardware wallet market.

The Hardware Wallet Market Report is Segmented by Connectivity (USB, NFC, Bluetooth, and More), Wallet Type (Hot Wallet and Cold Wallet), End User (Individual/Retail and Institutional/Enterprise), Distribution Channel (Online and Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 39.15% of 2025 value as OCC clarification prompted U.S. banks to integrate hardware-secured settlement services. High property-rights enforcement, deep insurance capacity, and significant venture capital pools create an ecosystem where start-ups iterate quickly on secure-element designs while institutional buyers validate those products through rigorous penetration tests. The hardware wallet market benefits when asset-managers replace omnibus custody accounts with on-premises cold-wallet cages that anchor SOC-2 controls.

Asia Pacific is on track for a 29.66% CAGR through 2031, accelerated by Singapore's MAS guidelines that label seed-phrase mis-management a critical operational risk and by Japan's FSA mandate for segregated custody. Domestic component manufacturers shorten lead times and lower costs, letting brands such as OneKey ship open-source units competitive with Western peers at lower ASPs. Consumers' dependence on super-apps cultivates NFC and Bluetooth deployment, so the region often previews mobile-first features that later migrate to Europe and North America, magnifying APAC's influence on the hardware wallet market roadmap.

Europe's MiCA framework translates privacy-first culture into systematic hardware adoption, driving consistent though comparatively moderate growth through 2031. France hosts Ledger's secure-element assembly lines, illustrating supply-chain reshoring designed to hedge tariff and geopolitical exposure. Simultaneously, Nordic pension funds lobby regulators to allow limited crypto allocations-conditional upon cold-wallet proof of reserves, which further embeds secure hardware in traditional finance workflows. Accordingly, regional dynamics enhance innovation density and push collective security standards higher across the hardware wallet market.

- Ledger SAS

- SatoshiLabs s.r.o.

- ShapeShift AG

- Coinkite Inc.

- CoolBitX Technology Ltd.

- Shift Crypto AG

- Penta Security Systems Inc.

- SecuX Technology Inc.

- ARCHOS S.A.

- ELLIPAL Ltd.

- BitLox Limited

- SafePal Technology Ltd.

- Keystone (Cobo Technology Ltd.)

- OPOLO SARL

- zSofitto NV (Sugi)

- KeepKey LLC

- IoTrust Co., Ltd. (D'CENT)

- Prokey Technologies Co., Ltd.

- CryoBit LLC

- BC VAULT d.o.o.

- Tangem AG

- OneKey Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying institutional adoption of self-custody solutions

- 4.2.2 Surge in cyber-breach publicity pushing demand for offline keys

- 4.2.3 Regulatory push for segregated crypto custody (MiCA, OCC)

- 4.2.4 Expanding DeFi and NFT ecosystems requiring multi-chain support

- 4.2.5 Emergence of Bluetooth/NFC form-factors enabling mobile payments

- 4.2.6 New import tariffs on Chinese crypto hardware boosting on-shore production

- 4.3 Market Restraints

- 4.3.1 Evolving AML/KYC mandates raising compliance costs

- 4.3.2 Persistent consumer UX complexity

- 4.3.3 Hardware supply-chain shortages for secure elements

- 4.3.4 Fragmented standards hindering interoperability

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Hardware Wallet Product Comparison

- 4.8 Assessment of Macroeconomic Factors

- 4.9 Case Study Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity

- 5.1.1 USB

- 5.1.2 NFC

- 5.1.3 Bluetooth

- 5.1.4 Others

- 5.2 By Wallet Type

- 5.2.1 Hot Wallet

- 5.2.2 Cold Wallet

- 5.3 By End User

- 5.3.1 Individual / Retail

- 5.3.2 Institutional / Enterprise

- 5.4 By Distribution Channel

- 5.4.1 Online

- 5.4.2 Offline

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Rest of Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Ledger SAS

- 6.4.2 SatoshiLabs s.r.o.

- 6.4.3 ShapeShift AG

- 6.4.4 Coinkite Inc.

- 6.4.5 CoolBitX Technology Ltd.

- 6.4.6 Shift Crypto AG

- 6.4.7 Penta Security Systems Inc.

- 6.4.8 SecuX Technology Inc.

- 6.4.9 ARCHOS S.A.

- 6.4.10 ELLIPAL Ltd.

- 6.4.11 BitLox Limited

- 6.4.12 SafePal Technology Ltd.

- 6.4.13 Keystone (Cobo Technology Ltd.)

- 6.4.14 OPOLO SARL

- 6.4.15 zSofitto NV (Sugi)

- 6.4.16 KeepKey LLC

- 6.4.17 IoTrust Co., Ltd. (D'CENT)

- 6.4.18 Prokey Technologies Co., Ltd.

- 6.4.19 CryoBit LLC

- 6.4.20 BC VAULT d.o.o.

- 6.4.21 Tangem AG

- 6.4.22 OneKey Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment