PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910515

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910515

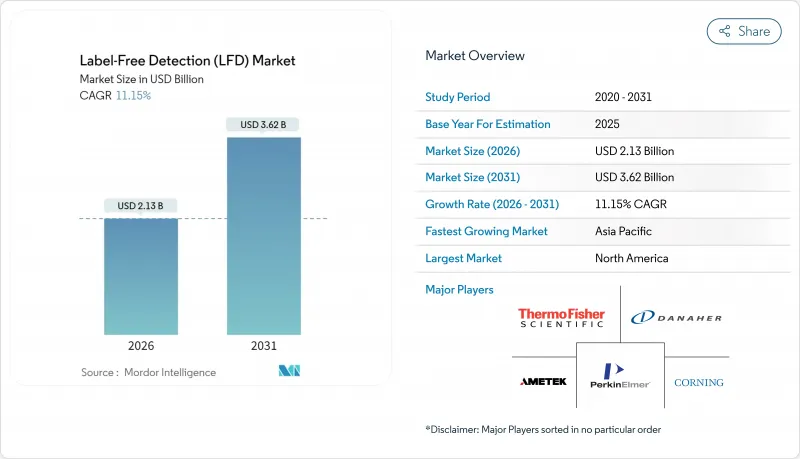

Label-Free Detection (LFD) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The label free detection market was valued at USD 1.92 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 3.62 billion by 2031, at a CAGR of 11.15% during the forecast period (2026-2031).

This expansion stems from the pharmaceutical sector's pivot to real-time kinetic assays, widespread integration of AI-driven data interpretation, and heightened demand for artifact-free screening workflows. Surface plasmon resonance (SPR) and bio-layer interferometry (BLI) systems dominate present installations, yet miniaturized fiber-optic sensors and cloud-native software are reshaping purchasing criteria for new projects. Vendors bundle instruments, consumables, and machine-learning software in subscription models that compress drug-discovery timelines, while regional investment incentives in Asia-Pacific nurture local manufacturing that lowers per-assay costs. Supply chain concentration in nanostructured chips and shortages of skilled operators temper momentum but have not slowed double-digit revenue growth for leading suppliers.

Global Label-Free Detection (LFD) Market Trends and Insights

SPR & BLI Adoption in Pharma Drug-Discovery Pipelines

Pharmaceutical laboratories are replacing ELISA with SPR and BLI instruments that generate kinetic, thermodynamic, and stoichiometric parameters in real time, shrinking assay development cycles from weeks to days. Sartorius introduced the Octet R8e in 2024, improving evaporation control that supports extended run times for low-molecular-weight leads. The U.S. Food and Drug Administration now accepts label-free kinetics in investigational new drug dossiers, which reduces validation overhead. These instruments analyze crude lysates without purification, a critical advantage for antibody-drug conjugates. Consequently, contract research organizations (CROs) report rising orders for outsourced kinetic characterization, amplifying installed-base growth of SPR and BLI systems in North America and Europe.

Investments in Biologics Driving Demand for Kinetic Assays

The USD 150 billion bispecific-antibody pipeline requires precise kinetic profiling to confirm correct chain pairing and mitigate off-target effects. Label-free assays quantify binding stoichiometry and cooperative interactions that fluorescent tags can distort. The Sensor-integrated Proteome On Chip platform enables thousands of antibody variants to be produced directly on SPR chips, expediting lead selection for oncology and autoimmune therapies. CROs record a 40% rise in biologics-related kinetic requests, indicating that the label free detection market will continue to see sustained instrument and consumable demand linked to monoclonal, bispecific, and antibody-drug conjugate development.

High Capital Cost of SPR/BLI Instruments

Advanced multi-channel SPR systems sell for USD 300,000-800,000 and require annual service contracts equal to 15-20% of purchase price. Smaller biotechs therefore share instrumentation or outsource to CROs, slowing in-house capability build-out. Leasing schemes reduce initial cash outlay but often cap annual sample volumes, limiting flexibility. High fixed costs remain the primary hurdle to wider diffusion of label-free technology, keeping the purchasing cycle concentrated among top-tier pharmaceutical firms and well-funded research labs.

Other drivers and restraints analyzed in the detailed report include:

- High-Throughput Screening Need to Cut Label-Based Assay Artifacts

- AI-Assisted Kinetic Modelling Accelerating Hit-to-Lead Timelines

- Requirement for Skilled Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The instrument class dominated with 51.72 % revenue share in 2025, underpinning core assay capacity across pharmaceutical R&D pipelines. Software and services, however, are advancing at an 11.55 % CAGR because cloud-native analytics convert raw sensorgrams into actionable SAR insights. Spending on subscription licences and managed-analysis services helps laboratories sidestep internal skill shortages. Consumables remain a moderate growth contributor as novel chemistries extend sensor life and broaden detectable analyte classes.

AI-augmented workflows embed algorithms that suggest regeneration protocols, flag mass-transport artifacts, and recommend follow-up titrations. Cloud repositories enable multi-site teams to view curves in real time, ensuring consistent decision gates. Instrument-as-a-service bundles further align operating expenses with project milestones, drawing startups into the label free detection market while tempering capital-expenditure barriers.

SPR accounted for 46.02 % of 2025 revenues, retaining leadership based on sensitivity and regulatory familiarity. BLI, though, is projected to expand at a 11.76 % CAGR as disposable probe designs tolerate crude samples and shorten cleaning cycles. Differential scanning calorimetry and isothermal titration calorimetry continue to supply niche thermodynamic insights, especially for viral protease inhibitor programs.

Competition between SPR and BLI centers on throughput versus sensitivity. Vendors enhance SPR with higher refractive-index stability and introduce BLI systems featuring automated microplate handlers. Emerging electrochemical and impedance methods target point-of-care formats, widening technology options for environmental labs that historically lacked capital for optical platforms. These alternatives create incremental opportunities without displacing core SPR/BLI spend.

The Global Label-Free Detection Market Report is Segmented by Product Type (Instruments, Consumables, Software & Services), Technology (Surface Plasmon Resonance, Bio-Layer Interferometry, and More), Application (Binding Kinetics & Affinity, and More), End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 38.85 % of 2025 revenue, underpinned by robust NIH and BARDA grants that favor biosensor-based biodefense projects. Capital budgets at major U.S. pharmaceutical firms funded fleet upgrades from single-channel SPR instruments to 16-channel platforms capable of 10,000 interactions per day. Government fast-track review pathways recognize label-free kinetics in biologics filings, shortening time-to-approval and reinforcing regional leadership.

Asia-Pacific is projected to log a 12.12 % CAGR to 2031, the fastest worldwide. China's five-year biotech plan subsidizes domestic SPR chip production, lowering consumable costs while India's contract-development organizations add label-free suites to capture biologics outsourcing contracts. Japan deepens its installed base for biosimilar comparability studies, and South Korea channels venture capital into AI-analytics startups focused on kinetic data. Cross-border joint ventures between Western instrument makers and regional manufacturers target mid-tier pricing that broadens installed base across local pharma clusters.

Europe retains its status as a steady growth region, driven by Horizon-Europe grants and a maturing biosimilar market that demands rigorous kinetic comparability. Germany and the United Kingdom maintain dense footprints of CROs offering full-spectrum label-free services, while France and Italy anchor food-safety applications connected to strict EU contamination thresholds. Regulatory divergence post-Brexit necessitates dual compliance workflows, elevating demand for harmonized analytics platforms in cross-channel biotech collaborations.

- Affinite Instruments Inc.

- Agilent Technologies

- AMETEK Inc. (Reichert)

- Bio-Rad Laboratories

- Bruker

- Carterra Inc.

- Danaher

- Hitachi

- HORIBA Ltd.

- Lumicks B.V.

- Malvern Panalytical Ltd.

- Nicoya Lifesciences Inc.

- Plexera Bioscience LLC

- Revvity Inc. (former PerkinElmer)

- Sartorius

- Siemens Healthineers

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of SPR & BLI in pharma drug-discovery pipelines

- 4.2.2 Investments in biologics driving demand for kinetic assays

- 4.2.3 High-throughput screening need to cut label-based assay artifacts

- 4.2.4 Miniaturized fiber-optic SPR sensors for decentralized PoC testing

- 4.2.5 AI-assisted kinetic modelling accelerating hit-to-lead timelines

- 4.2.6 Pandemic-preparedness programs funding airport biosensor roll-outs

- 4.3 Market Restraints

- 4.3.1 High capital cost of SPR/BLI instruments

- 4.3.2 Requirement for skilled operators

- 4.3.3 Fragile supply chain for nanostructured sensor chips

- 4.3.4 Lack of cross-platform data standards

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Consumables

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 Surface Plasmon Resonance (SPR)

- 5.2.2 Bio-Layer Interferometry (BLI)

- 5.2.3 Isothermal Titration Calorimetry (ITC)

- 5.2.4 Differential Scanning Calorimetry (DSC)

- 5.2.5 Other Optical / Impedance Methods

- 5.3 By Application

- 5.3.1 Binding Kinetics & Affinity

- 5.3.2 Thermodynamics & Stoichiometry

- 5.3.3 Lead Generation / Hit Validation

- 5.3.4 Diagnostics & Quality Control

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organizations (CROs)

- 5.4.3 Academic & Research Institutes

- 5.4.4 Food & Beverage / Environmental Labs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Affinite Instruments Inc.

- 6.3.2 Agilent Technologies Inc.

- 6.3.3 AMETEK Inc. (Reichert)

- 6.3.4 Bio-Rad Laboratories Inc.

- 6.3.5 Bruker Corporation

- 6.3.6 Carterra Inc.

- 6.3.7 Danaher Corporation

- 6.3.8 Hitachi High-Tech Corporation

- 6.3.9 HORIBA Ltd.

- 6.3.10 Lumicks B.V.

- 6.3.11 Malvern Panalytical Ltd.

- 6.3.12 Nicoya Lifesciences Inc.

- 6.3.13 Plexera Bioscience LLC

- 6.3.14 Revvity Inc. (former PerkinElmer)

- 6.3.15 Sartorius AG

- 6.3.16 Siemens Healthineers AG

- 6.3.17 Thermo Fisher Scientific Inc.

- 6.3.18 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment