PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910541

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910541

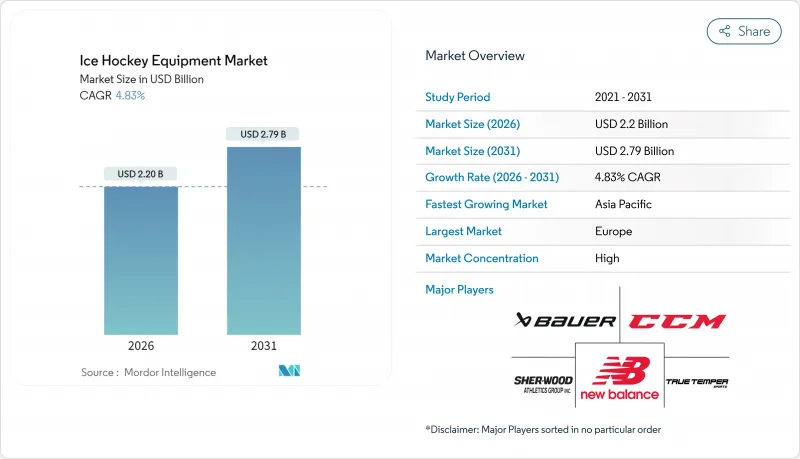

Ice Hockey Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The ice hockey equipment market was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.2 billion in 2026 to reach USD 2.79 billion by 2031, at a CAGR of 4.83% during the forecast period (2026-2031).

This growth is driven by increased global participation, expansion of professional leagues into new markets, and continuous product innovations focusing on lightweight materials and enhanced impact protection. The market received significant investment support in 2024, with private-equity funds acquiring two of the three largest manufacturers, providing capital for research, manufacturing improvements, and digital retail initiatives. Europe maintains its market dominance due to established youth development programs and IIHF safety regulations that require regular equipment replacement. The Asia-Pacific region shows the highest growth rate, supported by ice rink development in China, Japan, and Southeast Asian markets, where winter sports expenditure continues to increase. The integration of advanced materials such as carbon-fiber composites, cut-resistant fabrics, and specialized foams enables manufacturers to maintain profit margins while offering lighter equipment at premium price points.

Global Ice Hockey Equipment Market Trends and Insights

Rising Popularity of Ice Hockey Worldwide Fueling Demand for Equipment

The worldwide expansion of hockey participation has generated substantial equipment demand across non-traditional markets, with the Asia-Pacific region experiencing notable growth due to improved infrastructure development. The NHL's successful international expansion strategy demonstrates this market evolution, as evidenced by capacity crowds at games in Prague and Tampere. The increasing representation of European players in the NHL, now accounting for approximately 30% of team rosters, reflects the sport's global reach. Equipment manufacturers have responded to this diversification by developing specialized product lines that address regional climate variations and distinct playing styles. The upcoming 4 Nations Face-Off tournament and the anticipated 2026 Olympic participation are expected to enhance global visibility and stimulate equipment sales across emerging markets. This growth trajectory is exemplified in markets like the Philippines, where women's hockey teams have achieved international recognition despite facing equipment accessibility challenges, highlighting the considerable untapped market opportunities in these regions.

Expansion of Professional Leagues and Tournaments Increasing Visibility and Sport Appeal

The growth of professional leagues has a significant impact on equipment demand, driven by increased media exposure and changing purchasing behaviors among amateur players. The inaugural season of the Professional Women's Hockey League (PWHL) achieved notable success, with an average attendance of 5,689 fans per game and securing over 40 sponsorship partners, including major equipment manufacturers such as Bauer. Similarly, the Utah Hockey Club's entry into the Salt Lake City market demonstrated strong results, with consistent sellout crowds and robust merchandise sales, highlighting market potential in previously untapped regions. The PWHL's planned expansion into Vancouver for the 2025-26 season at Pacific Coliseum, supported by neutral-site game attendance figures of 19,038, underscores the strategic value of geographic diversification. The increased visibility of professional hockey directly influences equipment sales, as amateur players increasingly purchase professional-grade equipment to emulate professional standards and appearances.

High Cost of Advanced Equipment Limiting Affordability for Many Players

The substantial financial investment required for hockey equipment presents significant participation barriers, particularly affecting youth development and market expansion in emerging economies. The considerable annual costs associated with youth hockey participation in North America, including equipment expenses, create financial strain for many families. Essential equipment like hockey sticks and comprehensive goaltender gear requires substantial financial commitment, making the sport less accessible to lower-income households. Research from the Aspen Institute highlights that a significant portion of families face challenges with youth sports participation costs, leading to a notable decline in youth sports engagement over recent years. These affordability challenges create a ripple effect throughout the industry by limiting the growth of the player base, which directly impacts equipment demand across the value chain. While premium equipment pricing enables manufacturers to invest in product innovation, it simultaneously creates market segmentation that restricts accessibility and hampers participation growth across various demographic segments.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements Producing Lighter, More Durable, and Safer Equipment

- Advances in Materials Like Carbon Fiber Composites Improving Performance

- Counterfeit and Low-Quality Equipment Flooding the Market Undermining Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ice hockey gear and accessories hold a 47.62% market share in 2025, demonstrating the substantial investment required in protective equipment, helmets, and specialized accessories beyond basic playing equipment. The segment's dominant position reflects the industry's commitment to player safety, as regulations and standards require regular equipment replacement and upgrades to maintain optimal protection levels. Ice hockey skates are showing promising growth prospects, with projections indicating a 5.61% CAGR through 2031, driven by continuous improvements in blade technology and boot design that enhance player performance on the ice.

Professional athlete endorsements continue to shape consumer purchasing decisions in the market, while manufacturers invest significant resources in research and development to achieve breakthroughs in weight reduction and energy transfer capabilities. The ice hockey stick segment maintains consistent market performance, offering a range of options from premium carbon fiber composites to more affordable wood and aluminum variants, addressing diverse consumer preferences and budget considerations. The gear and accessories segment receives additional support from evolving safety regulations, particularly with the implementation of mandatory neck protection requirements across USA Hockey, NFHS, and AHL organizations in 2024-25, reinforcing the industry's focus on player safety and equipment standards.

Male players hold a dominant 73.05% share of the hockey equipment market in 2025, reflecting the sport's historically male-focused infrastructure and participation patterns. The market landscape has been shaped by decades of investment in male-oriented facilities, training programs, and equipment development. This established ecosystem has created a self-reinforcing cycle where male participation continues to drive substantial market growth and investment decisions.

The market is experiencing a significant transformation, driven by a 5.76% CAGR in female participation through 2031. The Professional Women's Hockey League (PWHL) has played a pivotal role in this shift, with its inaugural season drawing an average of 5,689 fans per game and forming partnerships with over 40 brands. This heightened visibility has prompted increased investment in hockey equipment by female players, introducing a new dynamic to the market. In response, manufacturers are developing product lines tailored to female players, addressing their unique anatomical needs and preferences. The growing female market segment presents a notable opportunity for innovation, as traditional gear designed for male players often lacks the fit and performance required by female athletes. This focus on female-specific requirements reflects a broader evolution in the market toward more inclusive product development and distribution strategies.

The Ice Hockey Equipment Market Report is Segmented by Product Type (Ice Hockey Skates, Ice Hockey Sticks, Ice Hockey Gear and Accessories), End User (Male, and Female), Category (Mass, and Premium), Distribution Channel (Offline Retail Stores, and Online Retail Stores) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The European hockey equipment market demonstrates substantial market leadership with a 48.20% share in 2025, underpinned by deeply embedded hockey traditions across Nordic countries, Russia, and emerging Central and Eastern European nations. This dominance is reinforced by strategic government investments in sports infrastructure, which has created a robust foundation for continuous participation growth. The region's market strength is further enhanced by well-established IIHF regulatory frameworks that maintain stringent equipment safety standards and performance consistency across national boundaries. The presence of professional leagues throughout multiple European countries generates significant visibility and equipment demand, while systematic youth development programs administered by national hockey federations ensure steady equipment replacement cycles. The recent recognition of Sweden with the IIHF Sustainability Award underscores the region's commitment to environmental considerations in equipment manufacturing and procurement decisions.

The Asia-Pacific region is experiencing remarkable growth in the hockey equipment market, recording a 6.36% CAGR through 2031. This exceptional growth trajectory is primarily attributed to substantial investments in ice rink infrastructure and increasing winter sports enthusiasm across major markets including China, Japan, Australia, and emerging economies like the Philippines. The region's expansion is characterized by significant infrastructure development and evolving cultural perspectives that position hockey as an aspirational sport, particularly among urban populations experiencing rising disposable income levels. However, the market faces notable challenges in developing regions, where complex international shipping requirements and underdeveloped local distribution networks create substantial barriers to equipment accessibility and affordability.

The North American market continues to operate as a mature yet stable segment, characterized by well-established participation patterns and comprehensive infrastructure that generates consistent demand patterns across the United States and Canada. The region confronts significant challenges related to participation affordability, particularly in youth segments, with annual participation costs reaching USD 2,583 in the United States and CAD 4,478 in Canada. Despite these constraints, the market demonstrates ongoing growth potential through professional league expansion initiatives, as evidenced by new market entries such as Salt Lake City, which typically result in notable regional increases in equipment demand.

- Bauer Hockey LLC

- CCM Hockey

- New Balance Inc.

- True Temper Sports Inc.

- Sher-wood Hockey Inc.

- Graf Skates AG

- Vaughn Hockey

- Winnwell Inc.

- Roller Derby Skate Corp.

- Canadian Tire Corp. (NHL Fanatics)

- Easton Hockey

- Mylec Inc.

- Oakley Inc. (Visors)

- HTM Sport GmbH (Head)

- Pallas Textiles (STX)

- Karbona Co. (Asia OEM)

- Torspo Hockey

- Verbero Hockey

- No-Sweat Co. (Helmet Liners)

- Ferland Sports

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising popularity of ice hockey worldwide fueling demand for equipment

- 4.2.2 Expansion of professional leagues and tournaments increasing visibility and sport appeal

- 4.2.3 Technological advancements producing lighter, more durable, and safer equipment

- 4.2.4 Advances in materials like carbon fiber composites improving performance

- 4.2.5 Product customization and variety meeting diverse consumer needs

- 4.2.6 Influence of sports celebrities and endorsements driving equipment demand

- 4.3 Market Restraints

- 4.3.1 High cost of advanced equipment limiting affordability for many players

- 4.3.2 Counterfeit and low-quality equipment flooding the market undermining trust

- 4.3.3 Logistics and supply chain disruptions impacting availability and prices

- 4.3.4 Seasonal nature of ice hockey reduces steady demand across the year

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Ice Hockey Skates

- 5.1.2 Ice Hockey Sticks

- 5.1.3 Ice Hockey Gear and Accessories

- 5.2 By End User

- 5.2.1 Male

- 5.2.2 Female

- 5.3 By Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Russia

- 5.5.2.2 Finland

- 5.5.2.3 Sweden

- 5.5.2.4 Czech Republic

- 5.5.2.5 Switzerland

- 5.5.2.6 Germany

- 5.5.2.7 France

- 5.5.2.8 United Kingdom

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 Australia

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.5 Middle East and Africa

- 5.5.5.1 South America

- 5.5.5.2 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bauer Hockey LLC

- 6.4.2 CCM Hockey

- 6.4.3 New Balance Inc.

- 6.4.4 True Temper Sports Inc.

- 6.4.5 Sher-wood Hockey Inc.

- 6.4.6 Graf Skates AG

- 6.4.7 Vaughn Hockey

- 6.4.8 Winnwell Inc.

- 6.4.9 Roller Derby Skate Corp.

- 6.4.10 Canadian Tire Corp. (NHL Fanatics)

- 6.4.11 Easton Hockey

- 6.4.12 Mylec Inc.

- 6.4.13 Oakley Inc. (Visors)

- 6.4.14 HTM Sport GmbH (Head)

- 6.4.15 Pallas Textiles (STX)

- 6.4.16 Karbona Co. (Asia OEM)

- 6.4.17 Torspo Hockey

- 6.4.18 Verbero Hockey

- 6.4.19 No-Sweat Co. (Helmet Liners)

- 6.4.20 Ferland Sports

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK