PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910553

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910553

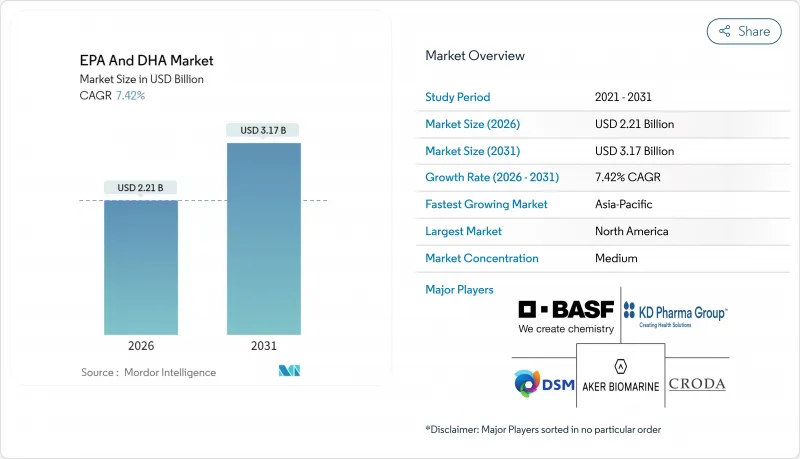

EPA And DHA - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

EPA and DHA market size in 2026 is estimated at USD 2.21 billion, growing from 2025 value of USD 2.06 billion with 2031 projections showing USD 3.17 billion, growing at 7.42% CAGR over 2026-2031.

Strong clinical evidence, favorable regulatory frameworks, and the scaling of algae-based production drive the EPA and DHA market. Rapid adoption of prescriptions following the REDUCE-IT cardiovascular outcomes trial, coupled with real-time oxidation controls that extend shelf life, supports market growth. North America continues to lead due to robust healthcare reimbursement policies, while the Asia-Pacific region benefits from swift regulatory approvals and growing health awareness. Diversifying raw material sourcing toward algae reduces reliance on Peruvian anchovy quotas, mitigating supply volatility, while quality certifications enhance consumer confidence. Ongoing investments in sustainable algae cultivation and process innovation are expected to enhance cost efficiency and support long-term market expansion.

Global EPA And DHA Market Trends and Insights

Growing Clinical Evidence Linking High-Dose EPA to Cardiovascular Risk Reduction

Findings from the landmark REDUCE-IT trial, which highlighted a 25% reduction in major adverse cardiovascular events with icosapent ethyl, have led to significant shifts in global clinical practice guidelines and regulatory approvals. Following these findings, the FDA greenlit high-dose EPA formulations aimed at reducing cardiovascular risks in patients with elevated triglycerides. This move has birthed a new prescription drug category, with projections soaring past USD 4 billion by 2030. Notably, an Asian subgroup analysis from REDUCE-IT revealed an even more pronounced benefit (HR 0.72) than the overall population. This insight has spurred regulatory submissions across APAC markets, especially given the region's escalating burden of cardiovascular diseases. The distinct mechanism of EPA, in contrast to combined EPA/DHA formulations, has led pharmaceutical firms to reformulate their products. This shift has resulted in supply chain premiums for high-purity EPA concentrates. Beyond prescriptions, nutraceutical companies are capitalizing on REDUCE-IT data for structure-function claims. However, regulatory bodies remain vigilant, drawing clear lines between therapeutic uses and dietary supplements. The ripple effect of this evidence has reached medical society guidelines. Both the American Heart Association and the European Society of Cardiology have integrated omega-3 recommendations, influencing clinical nutrition protocols.

Rapid Penetration of Concentrated Omega-3 in Prescription Drugs and Medical Nutrition

Pharmaceutical-grade omega-3 concentrates, boasting over 90% purity, have become staples in prescription formulations. This shift is largely due to their enhanced bioavailability and the resulting ease of patient compliance. A prime example of this trend is BASF's K85EE platform. It features 800-880 mg/g of total omega-3 ethyl esters, with an EPA content ranging from 430-495 mg/g, showcasing the technical prowess driving these prescription applications. Transitioning from 30-40% crude fish oil to over 90% concentrates demands cutting-edge molecular distillation and chromatographic separation technologies. Such advancements create entry barriers, favoring established players with the necessary processing capabilities. In medical nutrition, there's a growing emphasis on specific concentrate grades. This focus ensures therapeutic dosing fits within practical serving sizes, especially for conditions needing a daily intake of 2-4 grams of EPA/DHA. In a significant industry move, KD Pharma Group acquired DSM-Firmenich's marine lipids business in October 2024. This consolidation not only boosted concentrate production capacity but also crowned the combined entity as the globe's leading omega-3 manufacturer, granting them heightened pricing leverage in the pharmaceutical-grade market. The trend isn't limited to traditional sources; algae-based production is also in the spotlight. Companies like Corbion are pushing boundaries, achieving over 50% DHA concentrations in their AlgaPrime products, thanks to their unique fermentation and purification methods.

Regional Market Fragmentation

Disparate regulatory frameworks across major markets complicate compliance and create barriers to entry, constraining global omega-3 trade flows and inflating operational costs for multinational suppliers. While EFSA's novel food approvals facilitate access to the European market, China's NMPA framework mandates distinct documentation and testing protocols, potentially extending product launch timelines by 12 to 18 months. This fragmentation poses challenges, especially for smaller companies that lack the regulatory expertise and resources to simultaneously navigate multiple approval processes. As a result, market concentration is increasingly favoring established players with global compliance capabilities. Labeling requirements differ markedly across jurisdictions; some markets allow structure-function claims, while others limit therapeutic positioning. This divergence compels companies to maintain multiple product variants and diverse marketing strategies. Furthermore, the regulatory landscape varies in terms of quality standards: while IFOS certification might be adequate for certain markets, others demand local testing and documentation. Such discrepancies not only escalate compliance costs but also complicate the supply chain. Additionally, trade barriers like import tariffs and registration fees further fragment the global market. Some regions adopt protectionist policies, bolstering domestic omega-3 suppliers at the expense of international competitors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Vegan Consumer Base Driving Algae-Sourced DHA Launches

- Regulatory and Certification Advancements

- Heavy-Metal and Dioxin Contamination Concerns Prompting Stricter Testing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, DHA holds a commanding 57.78% share of the market, underscoring its strong foothold in both infant formula applications and cognitive health supplements. Meanwhile, EPA is on a rapid ascent, boasting an 7.86% CAGR through 2031, fueled by the burgeoning expansion of cardiovascular prescription drugs. The pivotal outcomes from the REDUCE-IT trial have spurred a surge in EPA-centric product development. In response, pharmaceutical firms are reengineering their combination products, placing a heightened emphasis on EPA content, especially for cardiovascular uses, as sanctioned by the FDA. Blend formulations strike a balance, providing cost efficiency and a wide array of benefits, making them a favored choice for dietary supplement manufacturers in search of adaptable ingredient platforms.

EPA's upward momentum is in sync with the precision medicine movement, which leans towards targeted therapeutic uses. Clinical studies highlight EPA's unique mechanisms of action, setting it apart from DHA, which primarily serves structural membrane roles. This heightened focus on cardiovascular health has led to a surge in supply chain premiums for high-purity EPA concentrates. Notably, BASF's K85EE platform, utilizing cutting-edge molecular distillation, boasts an impressive EPA content ranging from 430-495 mg/g. While DHA continues to reign supreme, thanks in part to regulatory nods in major markets for infant nutrition, such as FSSAI's green light for algal/fungal DHA in Indian infant formulas, set at 0.2-0.5% limits. The segmentation by type is evolving, emphasizing application-specific optimizations over a one-size-fits-all omega-3 approach, thereby fueling product differentiation and premium pricing strategies.

The EPA and DHA Market Report is Segmented by Product Type (Eicosapentaenoic Acid, Docosahexaenoic Acid, Blends), Source (Fish Oil, Algae Oil, Krill Oil, Other Marine Sources), Application (Dietary Supplements, Infant Formula, Fortified Food and Beverages, Pharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America commands a dominant 40.88% share of the omega-3 market, bolstered by the FDA's robust regulatory framework. This framework not only endorses dietary supplements but also prescription drug applications for omega-3 products. The region's well-established clinical research infrastructure substantiates therapeutic claims, and its strong healthcare reimbursement systems have spurred the adoption of prescription omega-3s, especially post the REDUCE-IT trial validation. In a nod to innovative and sustainable sourcing, Canada's Health Canada greenlit Nutriterra's plant-based omega-3 oil in December 2024. The mature supplement market in North America is increasingly prioritizing quality, with third-party certifications playing a pivotal role. Notably, IFOS-certified products are fetching premium prices, justifying investments in advanced processing. Meanwhile, Mexico's burgeoning middle class and modernizing healthcare present lucrative expansion avenues. Furthermore, the USMCA trade agreements are streamlining regulatory processes, bolstering cross-border trade in omega-3 products.

Asia Pacific is on track to be the fastest-growing region, boasting an 8.19% CAGR through 2031. This surge is fueled by demographic shifts, notably aging populations and urbanization, coupled with escalating healthcare expenditures. These factors are amplifying the demand for omega-3s across various therapeutic applications. China's NMPA framework is paving the way for international suppliers by clearly designating DHA as an approved nutrient supplement. Additionally, it recognizes fish oil as a permissible non-nutrient raw material. In India, the FSSAI has set concentration limits of 0.2-0.5% for algal and fungal DHA in infant nutrition. This move is particularly significant, given the potential market expansion for the 24 million infants born annually. Japan's regulatory landscape is equally advanced, listing omega-3 fatty acids in its Foods with Function Claims positive list. South Korea's MFDS is set to re-evaluate health functional ingredients in 2025. The region's rapid growth can be attributed to a regulatory modernization that adeptly balances consumer protection with a nod to innovation, fostering a thriving omega-3 market.

Europe's omega-3 market is witnessing steady growth, thanks in part to EFSA's stringent novel food approval process. This process has successfully granted regulatory status to several algae-derived omega-3 products, including the DHA 550 oil from Schizochytrium sp., a brainchild of Fermentalg. European consumers, increasingly leaning towards sustainability, are favoring algae-based alternatives and sustainably sourced fish oils. This trend is steering premium positioning strategies that highlight both environmental responsibility and health benefits. While Brexit introduced some regulatory hiccups, bilateral agreements have ensured that omega-3 products maintain their market access between the UK and the EU. Furthermore, regulatory harmonization among EU member states is simplifying compliance challenges, all while upholding stringent safety standards. This consistency is bolstering consumer trust in omega-3 products. The European market is also placing a premium on transparency and traceability, with stringent supply chain documentation favoring suppliers with robust quality systems. Emerging markets in South America, the Middle East, and Africa are showcasing promise, buoyed by evolving regulatory frameworks. Local production initiatives, such as Corbion's AlgaPrime facility in Brazil, underscore a strategic alignment with regional demand growth.

List of Companies Covered in this Report:

- BASF SE

- KD Pharma Group

- Croda International PLC

- Omega Protein Corporation

- Corbion NV

- Aker BioMarine ASA

- Koninklijke DSM NV

- Epax Norway (Pelagia)

- Neptune Wellness Solutions

- TASA Omega

- GC Rieber Oils

- OLVEA Fish Oils

- Lysi hf.

- Golden Omega

- Clover Corporation

- Nordic Naturals Inc

- Novotech Nutraceuticals

- Archer Daniels Midland

- Cargill

- Solutex GC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing clinical evidence linking high-dose EPA to cardiovascular risk reduction

- 4.2.2 Rapid penetration of concentrated omega-3 (>90% purity) in prescription drugs and medical nutrition

- 4.2.3 Expansion of vegan/plant-based consumer base driving algae-sourced DHA launches

- 4.2.4 Regulatory and certification advancements

- 4.2.5 National prenatal-DHA supplementation guidelines boosting infant-nutrition demand

- 4.2.6 Real-time oxidation monitoring tech reducing waste and enhancing shelf life in FandB fortification

- 4.3 Market Restraints

- 4.3.1 Volatile anchovy quotas tightening fish-oil supply

- 4.3.2 High cost of purification and advanced extraction

- 4.3.3 Regional market fragmentation

- 4.3.4 Heavy-metal and dioxin contamination concerns prompting stricter testing costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Eicosapentaenoic Acid (EPA)

- 5.1.2 Docosahexaenoic Acid (DHA)

- 5.1.3 Blends

- 5.2 By Source

- 5.2.1 Fish Oil

- 5.2.2 Algae Oil

- 5.2.3 Krill Oil

- 5.2.4 Other Marine Sources (Squid, Mussel, Calanus)

- 5.3 By Application

- 5.3.1 Dietary Supplements

- 5.3.2 Infant Formula

- 5.3.3 Fortified Food and Beverages

- 5.3.4 Pharmaceuticals

- 5.3.5 Clinical Nutrition and Medical Foods

- 5.3.6 Pet Nutrition

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 KD Pharma Group

- 6.4.3 Croda International PLC

- 6.4.4 Omega Protein Corporation

- 6.4.5 Corbion NV

- 6.4.6 Aker BioMarine ASA

- 6.4.7 Koninklijke DSM NV

- 6.4.8 Epax Norway (Pelagia)

- 6.4.9 Neptune Wellness Solutions

- 6.4.10 TASA Omega

- 6.4.11 GC Rieber Oils

- 6.4.12 OLVEA Fish Oils

- 6.4.13 Lysi hf.

- 6.4.14 Golden Omega

- 6.4.15 Clover Corporation

- 6.4.16 Nordic Naturals Inc

- 6.4.17 Novotech Nutraceuticals

- 6.4.18 Archer Daniels Midland

- 6.4.19 Cargill

- 6.4.20 Solutex GC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS