PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2097371

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2097371

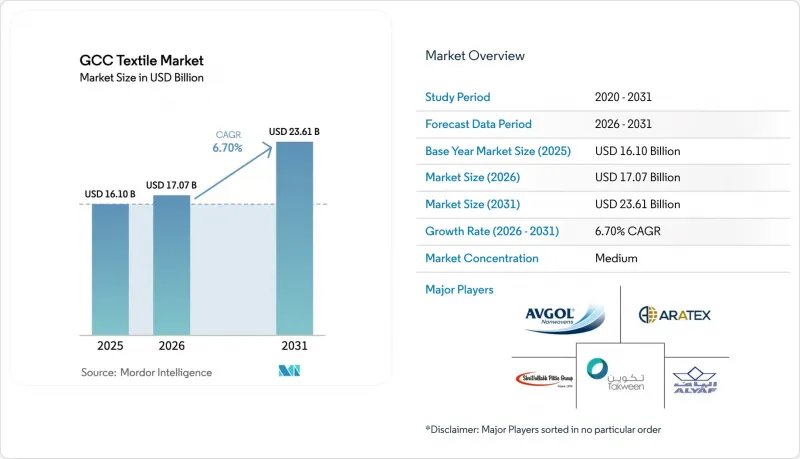

GCC Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the GCC textile market size is expected to increase from USD 16.10 billion in 2025 to USD 17.07 billion in 2026 and reach USD 23.61 billion by 2031, growing at a CAGR of 6.7% over 2026-2031.

This report is Segmented by Application (Fashion & Apparel, Industrial/Technical Textiles, and More), by Raw Material (Natural Fibers, Synthetic Fibers, and More), by Process/Technology (Woven, Knitted, Non-Woven, and More), and by Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman and Bahrain). Market Forecasts are Provided in Terms of Value (USD).

GCC Textile Market Trends and Insights

Vision 2030/2040 Industrial-Diversification Incentives & Subsidies

Robust policy support is drawing capital into spinning, nonwoven, and technical-textile projects, helping the GCC textile market localize inputs and upgrade technology. Saudi Arabia's August 2025 regulatory framework synchronizes industrial licensing, environmental compliance, and fire-safety approvals, thereby professionalizing factory operations. Concurrently, targeted financing such as the USD 55 million credit line that funded Al Shair Group's new staple-fiber plant in Yanbu underlines lender confidence. Oman's Ladayn Polymer Programme, backed by USD 104 million, replicates this model by bundling feedstock supply with offtake agreements. These initiatives are extending the regional value chain, but long gestation periods mean the full output uplift will arrive after 2028.

E-Commerce-Enabled Fast-Fashion Adoption Surge

Mobile penetration above 95% in the UAE and Saudi Arabia is accelerating direct-to-consumer sales and putting a premium on speed-to-market. Omnichannel revenue expanded 21% between 2019 and 2023, with click-and-collect now accounting for a quarter of sales for leading retailers. The result is compressed production cycles that favor local mills capable of replenishing inventories within days rather than weeks. Rising female labor-force participation widens the addressable consumer pool, and seasonal peaks tied to Ramadan and national holidays further stress supply chains. Manufacturers adopting agile production, real-time inventory tools, and augmented-reality selling are pulling ahead of peers confined to long import lead times.

Volatile Cotton and Synthetic Feedstock Prices

The USDA's December 2025 WASDE report projected global ending stocks at 76.0 million bales as production of 119.8 million bales narrowly tops mill use of 118.6 million bales, signaling continued price volatility. Cotton futures climbed past 64.5 cents /lb in December 2025 as weaker global demand intersected with dollar softness, boosting spot costs for regional spinners. Polyester tracks oil, so Brent fluctuations feed directly into PET fiber quotes. Counter-measures are emerging: Borouge 4's 1.4 million-tpa polyolefin line promises to temper synthetic-fiber prices once fully operational, while OQ's polymer project in Oman adds localized PP supply. Even so, dual exposure to agricultural commodities and crude keeps near-term margin visibility low, forcing mills to hedge or alter blend ratios quickly.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring Pivot by EU & MENA Brands

- Circular-Economy and Textile-Recycling Mandates

- Margin Pressure from Low-Cost Asian Import Influx

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles and Others (Protective, Sports Textiles, etc.) are accounted for 42.03% of the GCC textile market size for non-fashion uses in 2025, trailing only fashion & apparel but expanding more quickly at a 7.94% CAGR through 2031. Major construction programs such as NEOM and Diriyah are specifying geotextiles, geocomposites, and reinforcement fabrics to meet stringent engineering codes, lifting large orders for domestic producers. Alyaf Industrial added capacity above 20,000 tpa to service landfill, drainage, and green-roof projects, while KAST W.L.L. is targeting USD 6 million in revenue within three years by localizing fiberglass reinforcements for concrete structures.

Fashion & apparel still led consumption with 57.97% GCC textile market share in 2025, reflecting high discretionary income and luxury retail clusters in Dubai and Riyadh. Yet, rising import substitution in uniforms, automotive fabrics, and medical disposables is tilting capital spending toward technical lines. Nonwoven suppliers such as Saudi German Nonwovens, now operating five Reicofil lines, are capturing hygiene and drape contracts from global majors like Molnlycke. Over 2026-2031, product development that blends performance with Islamic modest-fashion cues is set to widen margins and smooth demand seasonality.

Complete Report Scope:

- By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others (Protective, Sports Textiles, etc.)

- By Raw Material

- Natural Fibers

- Cotton

- Wool

- Silk

- Synthetic Fibers

- Polyester

- Nylon

- Rayon / Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- Natural Fibers

- By Process / Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond / Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

List of Companies Covered in this Report:

- Alyaf Industrial Co. Ltd.

- SV Pittie Sohar Textiles

- Takween Advanced Industries

- Aratex Group

- Avgol Middle East

- Saudi German Nonwovens

- FPC Coated Technical Textiles

- Millennium Fashions Industries

- Lomar Collection

- Threads Group LLC

- Atraco Group

- Creative Clothing Co.

- Amin Textile Factory

- Baroque Garments

- Al Borj Machinery LLC

- Unirab & Polvara Spinning Weaving & Silk

- Misr Amreya

- AMCO Apparel Mfg. Co.

- Kabale Textiles

- New Global Cotton Textile LLC

- Fabricon International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fashion-conscious youth cohort expansion

- 4.2.2 E-commerce-enabled fast-fashion adoption surge

- 4.2.3 Vision 2030/2040 industrial-diversification incentives & subsidies

- 4.2.4 Circular-economy and textile-recycling mandates

- 4.2.5 Near-shoring pivot by EU & MENA brands to mitigate supply-chain shocks

- 4.2.6 AI-driven on-demand micro-factory models reducing lead-times & waste

- 4.3 Market Restraints

- 4.3.1 Volatile cotton & synthetic feedstock prices

- 4.3.2 Margin pressure from low-cost Asian import influx

- 4.3.3 Rising water-tariffs & carbon-pricing costs in dyeing/finishing

- 4.3.4 Absence of unified GCC textile-safety standards inflating compliance costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter?s Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts(Values, In USD Billion)

- 5.1 By Application

- 5.1.1 Fashion & Apparel

- 5.1.2 Industrial/Technical Textiles

- 5.1.3 Household & Home Textiles

- 5.1.4 Medical & Healthcare Textiles

- 5.1.5 Automotive & Transport Textiles

- 5.1.6 Others (Protective, Sports Textiles, etc.)

- 5.2 By Raw Material

- 5.2.1 Natural Fibers

- 5.2.1.1 Cotton

- 5.2.1.2 Wool

- 5.2.1.3 Silk

- 5.2.2 Synthetic Fibers

- 5.2.2.1 Polyester

- 5.2.2.2 Nylon

- 5.2.2.3 Rayon / Viscose

- 5.2.2.4 Acrylic

- 5.2.2.5 Polypropylene

- 5.2.3 Recycled Fibers

- 5.2.4 Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE))

- 5.2.1 Natural Fibers

- 5.3 By Process / Technology

- 5.3.1 Woven

- 5.3.2 Knitted

- 5.3.3 Non-woven

- 5.3.3.1 Spunlaid (Spunbond / Melt-blown)

- 5.3.3.2 Dry-laid Hydro-entangled

- 5.3.3.3 Wet-Laid

- 5.3.3.4 Needle-punched

- 5.3.4 3-D Weaving & Spacer Fabrics

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Oman

- 5.4.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Alyaf Industrial Co. Ltd.

- 6.4.2 SV Pittie Sohar Textiles

- 6.4.3 Takween Advanced Industries

- 6.4.4 Aratex Group

- 6.4.5 Avgol Middle East

- 6.4.6 Saudi German Nonwovens

- 6.4.7 FPC Coated Technical Textiles

- 6.4.8 Millennium Fashions Industries

- 6.4.9 Lomar Collection

- 6.4.10 Threads Group LLC

- 6.4.11 Atraco Group

- 6.4.12 Creative Clothing Co.

- 6.4.13 Amin Textile Factory

- 6.4.14 Baroque Garments

- 6.4.15 Al Borj Machinery LLC

- 6.4.16 Unirab & Polvara Spinning Weaving & Silk

- 6.4.17 Misr Amreya

- 6.4.18 AMCO Apparel Mfg. Co.

- 6.4.19 Kabale Textiles

- 6.4.20 New Global Cotton Textile LLC

- 6.4.21 Fabricon International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment