PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910604

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910604

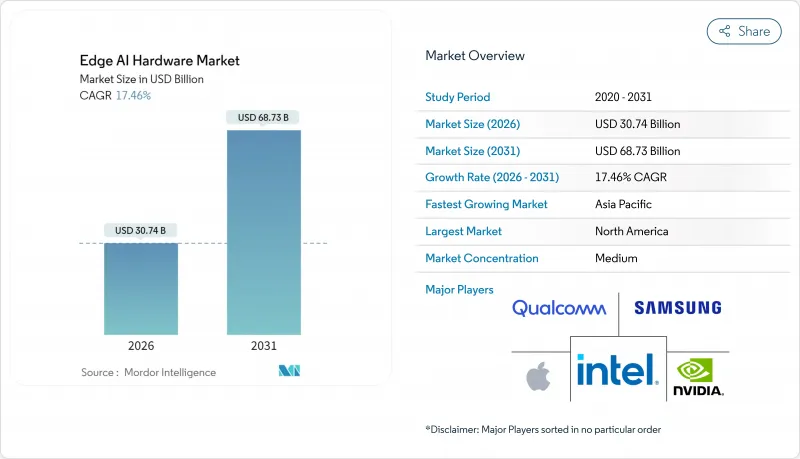

Edge AI Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Edge AI hardware market was valued at USD 26.17 billion in 2025 and estimated to grow from USD 30.74 billion in 2026 to reach USD 68.73 billion by 2031, at a CAGR of 17.46% during the forecast period (2026-2031).

Momentum stems from rising demand for on-device inference that cuts latency, safeguards data sovereignty, and lowers energy consumption. Premium-tier smartphones, AI-enabled personal computers, and mandatory automotive safety systems anchor near-term growth. Government incentives such as the CHIPS and Science Act encourage domestic production capacity, while 5G-powered multi-access edge computing (MEC) broadens the addressable workload. Competitive intensity is moderate as diversified semiconductor leaders defend share against application-specific chip suppliers that optimize performance per watt. Supply-chain concentration at advanced foundries and widening export controls add regional complexity but also stimulate indigenous alternatives.

Global Edge AI Hardware Market Trends and Insights

Rise of AI-Enabled Personal Computing Transforms Processor Architecture

Dedicated neural processing units (NPUs) in the latest laptop chips achieve 40-50 TOPS of local AI throughput, allowing large language models and genera-tive workloads to run offline with instant response times. New design baselines from Microsoft Copilot+ PCs compel every OEM to integrate similar acceleration, steering roadmaps toward heterogeneous compute rather than general-purpose cores. Semiconductor roadmaps through 2030 now prioritize inference-optimized tiles, driving sustained demand for edge-centric nodes.

Smartphone AI Capabilities Drive Premium Segment Refresh Cycles

Flagship mobile processors deliver 45-50 TOPS inference and extend battery life by scheduling AI tasks to dedicated engines. On-device translation, generative imaging, and personal-assistant features create clear upgrade motives across premium tiers, shortening replacement intervals. Mid-range designs will inherit last year's flagship capabilities, expanding volume shipments of specialized AI silicon.

Advanced Node Manufacturing Costs Limit Market Entry

Developing a 3 nm device demands over USD 100 million in masks and USD 20,000 per wafer, constraining access for new entrants. Consolidation accelerates as smaller firms seek scale or niche differentiation. Design-for-node co-optimization and chiplet partitioning partially offset cost but reinforce the advantage for incumbents with existing supply contracts.

Other drivers and restraints analyzed in the detailed report include:

- 5G Infrastructure Enables Distributed Edge Computing Architectures

- Automotive Safety Regulations Mandate Advanced Driver Assistance Systems

- Export Control Restrictions Fragment Global Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GPU devices captured 50.12% Edge AI hardware market share in 2025 owing to mature software stacks and high parallel throughput. Over the forecast horizon, ASICs and NPUs are projected to post a 18.74% CAGR as designers emphasize performance per watt. The Edge AI hardware market size for ASICs is expected to rise sharply as automotive and industrial buyers prioritize deterministic latency and functional safety. CPUs retain value where mixed workloads require general-purpose resources, and FPGAs grow in reconfigurable roles across telecom and defense.

Chiplet packaging combines CPU, GPU, and NPU tiles on common substrates, optimizing each die for distinct tasks while sharing memory interfaces. Vendors integrate security enclaves and functional-safety monitors at the silicon layer, satisfying regulatory mandates in healthcare and automotive deployments. Multi-foundry strategies mitigate geopolitical risk, yet advanced-node dependence keeps negotiating leverage with leading fabs.

Smartphones accounted for 39.25% of the Edge AI hardware market size in 2025, leveraging annual refresh cycles and large unit volumes. Robots and drones, however, represent the fastest trajectory, climbing at 19.32% CAGR as autonomous navigation and vision analytics demand low-latency inference. Specialized edge boards pair vision processors with depth sensors, enabling millisecond obstacle avoidance.

Cameras integrate edge AI to execute real-time detection within enclosures, reducing video backhaul costs for retail analytics and smart cities. Wearables adopt ultra-low-power neural engines that extract health insights continuously under limited battery budgets. Smart speakers consolidate voice capture, beamforming, and NLP inference on single chips, shrinking the bill of materials and enhancing privacy by keeping audio local.

The Edge AI Hardware Market Report is Segmented by Processor (CPU, GPU, and More), Device (Smartphones, Cameras and Smart Vision Sensors, and More), End-User Industry (Consumer Electronics, Automotive and Transportation, and More), Deployment Location (Device Edge, Near Edge Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 38.92% revenue in 2025 on the back of USD 52 billion CHIPS incentives and early enterprise pilots in automotive, retail, and healthcare. Start-ups leverage venture capital density to commercialize domain-specific accelerators. Export-control policy constrains outbound sales, yet secures domestic defense and aerospace demand.

Asia-Pacific is advancing at a 19.27% CAGR, outpacing all other regions. China funds native GPU and NPU ventures to circumvent import restrictions, while South Korea allocates USD 7 billion for national AI chip lines. Japan's Society 5.0 agenda stimulates smart-factory retrofits that require deterministic edge compute.

Europe balances sovereignty aims with budget realities under its EUR 43 billion Chips Act. Automotive hubs in Germany and France prioritize functional-safe edge inference, while GDPR compliance encourages on-premise analytics. Israel's vibrant start-up ecosystem targets defense and medical imaging use cases, exporting boards across EMEA.

Latin America sees early adoption in agriculture drones and smart-city surveillance. The Middle East accelerates investment in sovereign data centers coupled with edge gateways to host AI for logistics and energy infrastructure. Africa remains nascent but leapfrogs legacy stacks through mobile-first deployments allied with satellite backhaul.

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Incorporated

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Advanced Micro Devices, Inc.

- Huawei Technologies Co., Ltd.

- Alphabet Inc. (Google LLC)

- Amazon.com, Inc.

- Alibaba Group Holding Limited

- Baidu, Inc.

- Continental AG

- DENSO Corporation

- Robert Bosch GmbH

- Kalray S.A.

- MediaTek Inc.

- Imagination Technologies Limited

- Hailo Technologies Ltd.

- SiMa.ai, Inc.

- BrainChip Holdings Ltd.

- Syntiant Corp.

- Mythic, Inc.

- Gyrfalcon Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise of AI-enabled Personal Computing (AI PCs)

- 4.2.2 Smartphone upgrade cycle toward on-device AI

- 4.2.3 5G and 6G-driven MEC deployments lower latency

- 4.2.4 Automotive L2-L4 ADAS edge inference demand

- 4.2.5 Energy-efficient Analog and PIM accelerators

- 4.2.6 Government CHIPS ACT-style incentives

- 4.3 Market Restraints

- 4.3.1 High upfront NRE costs for advanced nodes

- 4.3.2 Fragmented toolchains and software lock-in

- 4.3.3 Talent shortage in edge-oriented ML and silicon

- 4.3.4 Supply-chain geopolitical export controls

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Processor

- 5.1.1 CPU

- 5.1.2 GPU

- 5.1.3 FPGA

- 5.1.4 ASIC and NPU

- 5.2 By Device

- 5.2.1 Smartphones

- 5.2.2 Cameras and Smart Vision Sensors

- 5.2.3 Robots and Drones

- 5.2.4 Wearables

- 5.2.5 Smart Speakers and Home Hubs

- 5.2.6 Other Edge Devices

- 5.3 By End-User Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and Transportation

- 5.3.3 Manufacturing and Industrial IoT

- 5.3.4 Healthcare

- 5.3.5 Government and Public Safety

- 5.3.6 Other End-User Industries

- 5.4 By Deployment Location

- 5.4.1 Device Edge

- 5.4.2 Near Edge Servers

- 5.4.3 Far Edge / MEC

- 5.4.4 Cloud-Assisted Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Singapore

- 5.5.4.6 Australia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Intel Corporation

- 6.4.3 Qualcomm Incorporated

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Apple Inc.

- 6.4.6 Advanced Micro Devices, Inc.

- 6.4.7 Huawei Technologies Co., Ltd.

- 6.4.8 Alphabet Inc. (Google LLC)

- 6.4.9 Amazon.com, Inc.

- 6.4.10 Alibaba Group Holding Limited

- 6.4.11 Baidu, Inc.

- 6.4.12 Continental AG

- 6.4.13 DENSO Corporation

- 6.4.14 Robert Bosch GmbH

- 6.4.15 Kalray S.A.

- 6.4.16 MediaTek Inc.

- 6.4.17 Imagination Technologies Limited

- 6.4.18 Hailo Technologies Ltd.

- 6.4.19 SiMa.ai, Inc.

- 6.4.20 BrainChip Holdings Ltd.

- 6.4.21 Syntiant Corp.

- 6.4.22 Mythic, Inc.

- 6.4.23 Gyrfalcon Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment