PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910636

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910636

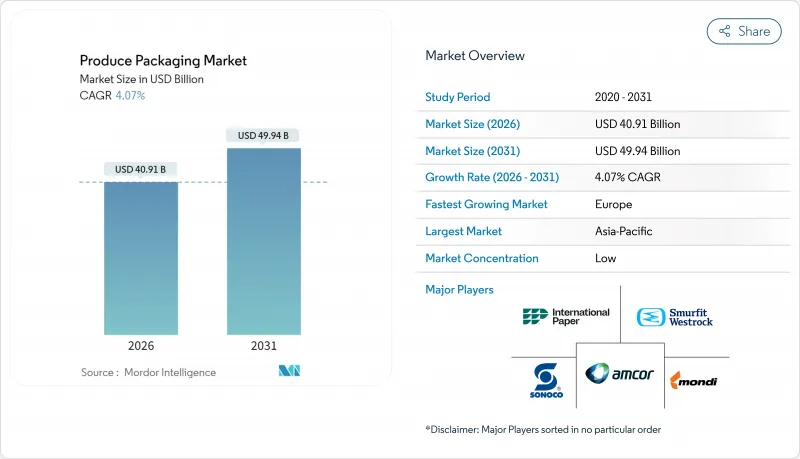

Produce Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The produce packaging market was valued at USD 39.31 billion in 2025 and estimated to grow from USD 40.91 billion in 2026 to reach USD 49.94 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031).Rising consumer demand for fresh, traceable produce, combined with strict sustainability mandates, is steering material choices toward paper, paperboard, and next-generation bioplastics.

Retailers are prioritizing active and intelligent solutions that extend shelf life, cut food waste, and support global food-security commitments. Flexible pack formats continue to gain traction because they deliver strong barrier performance with lower material intensity, while automation and robotics help growers control unit costs despite volatile resin and fiber prices. Competitive rivalry is intensifying as sustainability-focused start-ups introduce circular materials that challenge incumbent leaders in the produce packaging market.

Global Produce Packaging Market Trends and Insights

Surge in Convenience-Oriented Fresh Produce Demand

Packaged fresh-cut salads, sliced fruit cups, and snack-ready vegetable packs have moved rapidly from niche to mainstream retail shelves since 2024. Shelf-life gains of 7-10 days from modified-atmosphere pouches allow supermarkets to broaden geographic distribution without sacrificing freshness. Resealable antimicrobial films reduce spoilage after opening, appealing to smaller households concerned about waste. Gross margins on convenience SKUs sit 15-25% above bulk formats, encouraging converters to invest in precision barrier technology. On e-commerce channels, orders protected by damage-resistant packs show 40% higher repeat rates, proving that packaging performance directly reinforces brand loyalty. These factors collectively propel the produce packaging market as retailers and growers chase profitable growth.

Rapid Uptake of Modified-Atmosphere and Antimicrobial Films

Gas-permeable films tuned to produce type lower respiration rates in leafy greens by 60% and maintain vitamin content during extended display periods. The FDA cleared 12 new natural antimicrobial formulations in 2024, giving packers safer tools to curb microbial growth without chemical preservatives. Asian manufacturers lead the charge with temperature-responsive films that alter permeability as ambient conditions change, minimizing condensation. Premium organic and exotic items adopt these solutions first because shelf-life improvement offsets higher material cost. Accelerated adoption strengthens the produce packaging market as growers target export windows previously considered risky due to spoilage.

Volatile Polymer and Paper Input Prices

Crude-oil swings drove resin prices up to 35% in 2024, while paperboard rose 22% on fiber shortages. Small converters lacking hedging tools or volume contracts experienced margin compression that triggered consolidation waves. Frequent re-pricing disrupted grower-packer contracts, delaying roll-outs of new packaging that carries higher material cost. Currency shifts worsened instability for exporters purchasing inputs in EUR or USD while selling in local currencies. While large multinationals weather volatility through scale, sustained price turbulence restrains investment in sustainable innovation within the produce packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Global Fresh Produce E-Commerce and Cold-Chain Logistics

- Sustainability Mandates Boosting Paper-Based and Compostable Formats

- Regulatory Bans and Taxes on Single-Use Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and paperboard retained 25.15% of the produce packaging market share in 2025, reflecting improved water-resistant coatings that broadened use beyond dry produce. The segment benefits from recyclability mandates that compress the cost gap versus plastics. Bioplastics recorded the sector's fastest CAGR at 12.72%, fueled by R&D progress in PLA and PHA that now match tensile and clarity benchmarks once exclusive to PET. Enhanced compostability supports brand messaging around zero-waste goals, propelling adoption in premium organic lines.

Plastic containers still dominate applications demanding high impact resistance, especially for grape and tomato clamshells that travel long distances. Corrugated boxes capture gains from booming e-commerce produce deliveries, often integrating phase-change inserts to stabilize temperature. Film lidding and laminates continue to differentiate high-value berries through superior gas control, while molded-fiber trays advance as plastic replacements when retailers seek curbside-recyclable formats. The interplay of performance, compliance, and branding keeps material choice dynamic within the produce packaging market.

Flexible pouches, flow wraps, and form-fill-seal packs delivered 31.76% of the produce packaging market size in 2025, aided by 60-70% lower material usage than rigid counterparts. Lightweight structures reduce freight emissions, aligning with corporate carbon targets. Adoption deepened when laser-scored openings and zip-track closures delivered convenience without compromising barrier integrity.

Semi-rigid thermoforms protect delicate stone fruit and blueberries, where cushioning properties mitigate bruising through cold-chain vibrations. Rigid containers maintain relevance for club-store packs requiring stackability and tamper evidence, but digital printing and perforation innovations help flexibles encroach on that territory. As circular-ready mono-material films reach commercial scale, brand owners see flexibles as pivotal to meeting recyclability thresholds, reinforcing their growth path inside the produce packaging market.

The Produce Packaging Market Report is Segmented by Packaging Material Type (Plastic Containers, Paper and Paperboard, Corrugated Boxes, Bags and Pouches, and More), Pack Type (Rigid, Semi-Rigid, and Flexible), Application (Fruits, Vegetables, Fresh-Cut Produce, and More), Technology (Modified Atmosphere Packaging, Active and Intelligent Packaging, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 33.85% of global value in 2025 as governments poured more than USD 15 billion annually into cold-chain upgrades. China's stricter food-safety code now mandates QR-based traceability, elevating demand for smart labels that pair with consumer apps. India's e-grocery boom spurred construction of temperature-controlled hubs that rely on humidity-regulating pallets and pouches tailored to tropical climates. Southeast Asian exporters, led by Thailand, adopted shock-absorbing fiber trays for long-haul shipments that protected delicate durians and mangosteens, lifting packaged-fruit export value by 18%.

Europe is projected to record the fastest regional CAGR at 8.78% as the EU PPWR drives a wholesale pivot to recyclable and compostable formats. German and Dutch converters pioneer water-based dispersion coatings that keep fiber packs sturdy in wet conditions yet remain repulpable. Nordic multistakeholder loops allow used produce packs to return to fiber mills, closing the material loop. Retailers accept 20-30% pack cost premiums when they translate directly into documented waste reduction, sustaining momentum in the produce packaging market.

North America shows steady advancement underpinned by mature automation and dense distribution networks. U.S. and Canadian consumers willingly pay premiums for resealable pouches that lessen spoilage at home. Mexico's export-oriented farms deploy MAP liners that preserve berries during cross-border runs, while Canadian grocers champion compostable options as part of nationwide food-waste targets. Solid recycling capacity supports fiber and mono-material film growth, indicating a stable yet progressive trajectory for the produce packaging market in the region.

- Amcor plc

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Sonoco Products Company

- Sealed Air Corporation

- Coveris Holding SA

- Reynolds Consumer Products Inc.

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Printpack Inc.

- Anchor Packaging Inc.

- Pactiv Evergreen Inc.

- Packaging Corporation of America

- Constantia Flexibles Group

- Silgan Holdings Inc.

- Linpac Senior Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Convenience Oriented Fresh Produce Demand

- 4.2.2 Rapid Uptake of Modified-Atmosphere and Antimicrobial Films

- 4.2.3 Expansion of Global Fresh Produce E-Commerce and Cold-Chain Logistics

- 4.2.4 Sustainability Mandates Boosting Paper-Based and Compostable Formats

- 4.2.5 Stricter Food Safety and Traceability Regulations

- 4.2.6 Automation and Robotics Lowering Unit Packing Costs for Growers

- 4.3 Market Restraints

- 4.3.1 Volatile Polymer And Paper Input Prices

- 4.3.2 Regulatory Bans And Taxes On Single-Use Plastics

- 4.3.3 High Capital Cost Of Next-Gen Sustainable Materials And Machinery

- 4.3.4 Post-Harvest Loss Risk From Packaging Specification Errors

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Material Type

- 5.1.1 Plastic Containers

- 5.1.2 Paper and Paperboard

- 5.1.3 Corrugated Boxes

- 5.1.4 Bags and Pouches

- 5.1.5 Film Lidding and Laminates

- 5.1.6 Trays

- 5.1.7 Bioplastics

- 5.2 By Pack Type

- 5.2.1 Rigid

- 5.2.2 Semi-Rigid

- 5.2.3 Flexible

- 5.3 By Application

- 5.3.1 Fruits

- 5.3.2 Vegetables

- 5.3.3 Fresh-Cut Produce

- 5.3.4 Organic Produce

- 5.3.5 Exotic and Specialty Produce

- 5.4 By Technology

- 5.4.1 Modified Atmosphere Packaging

- 5.4.2 Active and Intelligent Packaging

- 5.4.3 Antimicrobial Packaging

- 5.4.4 Edible and Biodegradable Coatings

- 5.4.5 Vacuum Skin Packaging

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 International Paper Company

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Mondi plc

- 6.4.5 Sonoco Products Company

- 6.4.6 Sealed Air Corporation

- 6.4.7 Coveris Holding SA

- 6.4.8 Reynolds Consumer Products Inc.

- 6.4.9 Huhtamaki Oyj

- 6.4.10 Graphic Packaging Holding Company

- 6.4.11 Printpack Inc.

- 6.4.12 Anchor Packaging Inc.

- 6.4.13 Pactiv Evergreen Inc.

- 6.4.14 Packaging Corporation of America

- 6.4.15 Constantia Flexibles Group

- 6.4.16 Silgan Holdings Inc.

- 6.4.17 Linpac Senior Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment