PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910669

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910669

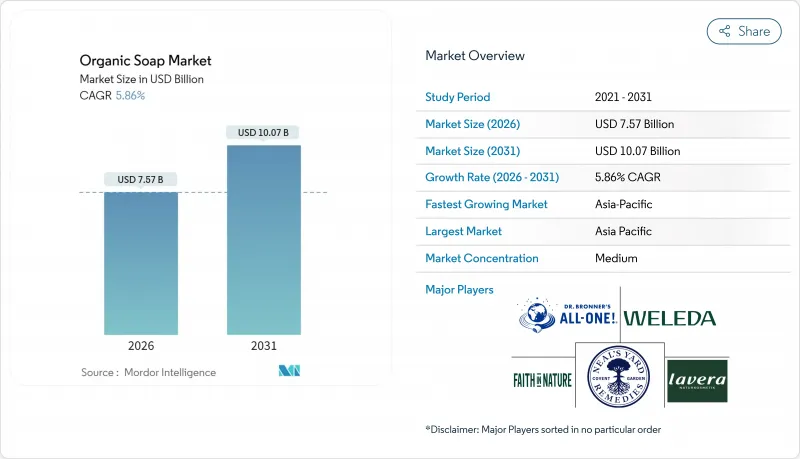

Organic Soap - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Organic soap market size in 2026 is estimated at USD 7.57 billion, growing from 2025 value of USD 7.15 billion with 2031 projections showing USD 10.07 billion, growing at 5.86% CAGR over 2026-2031.

As consumers increasingly gravitate towards clean-label, chemical-free personal care products that embody wellness and sustainability values, the organic bar soap market is witnessing steady expansion. Credible certification frameworks like USDA Organic and COSMOS bolster trust in these offerings. While North America and Europe lead in maturity due to established certifications and demand, the Asia-Pacific region is on the rise, fueled by increasing incomes and a penchant for herbal, traditional formulations. Bar soaps dominate the market: for instance, Sagitta Hand Soap 1911 highlights functional, gentle cleansing by incorporating prebiotic inulin with juniper and pine oils from organic sources. In India, Indo Naturals showcases formulation innovation by blending probiotics with turmeric and herbs in compact shaving-soap formats. Digital platforms and social commerce have emerged as pivotal distribution channels, enabling niche brands to connect directly with global consumers. Concurrently, sustainability trends are driving innovations in biodegradable and minimal-packaging designs, resonating with circular economy objectives. These structural and technological evolutions, coupled with shifting clean-beauty consumer behaviors, pave the way for continued growth in the organic bar soap sector.

Global Organic Soap Market Trends and Insights

Rising Demand for Natural and Chemical-Free Personal Care Products

As consumers increasingly prioritize ingredient transparency and safety, the demand for natural and chemical-free bar soaps is surging, propelling market expansion. A 2024 survey by the National Sanitation Foundation (NSF) reveals that 74% of Americans prefer organic ingredients in personal care, and 65% actively seek transparent ingredient lists to sidestep harmful components . In response, brands are emphasizing authenticity and eco-conscious values. For instance, in 2024, The Little Soap Company introduced its Eco Warrior Baby & Child Edit bars, tailored for sensitive skin, garnering praise from parents prioritizing allergen-free and sustainable choices. Likewise, brands like Ethique, Meow Meow Tweet, and Alaffia have cultivated dedicated followings by championing plant oils, shea butter, and zero-waste packaging, resonating with health-conscious and eco-minded consumers. This trend underscores a broader lifestyle evolution, where natural soaps symbolize holistic wellness and environmental responsibility. Such alignment of values with purchasing decisions fuels the momentum for organic bar soaps, cementing their role as pivotal players in the broader personal care market's evolution.

Increasing Emphasis on Eco-Friendly and Sustainable Products

As consumers increasingly prioritize eco-friendliness, the demand for sustainable bar soaps is surging. In 2024, Goop teamed up with evolvetogether to launch a low-to-zero waste soap bar. This soap not only adheres to Goop's clean-certified standards but is also wrapped in eco-friendly paper derived from wood pulp. The soap's formula features fine coconut shell powder for a gentle cleanse, shea and murumuru butters, and olive oil for hydration, and licorice root to bolster the skin barrier, catering to consumers who value both sustainability and skin health. ITC's Savlon has also entered the fray, unveiling glycerin bar soaps encased in recycled plastic, making sustainable choices more mainstream. Meanwhile, niche brands are pushing the envelope with biodegradable wrappers and innovative plantable seed-paper packaging, resonating with consumers who see packaging as a reflection of product integrity. These trends underscore how consumers are increasingly favoring brands that seamlessly blend sustainable packaging with natural ingredients, driving the bar soap segment from a niche market to a mainstream powerhouse. The growing emphasis on eco-consciousness is also encouraging brands to innovate further, ensuring they stay competitive in this evolving market.

Dominance of Conventional Soaps

The widespread preference for conventional soaps poses a significant challenge to the growth of the organic soap market. Conventional soap brands like Lux, Dove, and Lifebuoy leverage aggressive pricing, widespread distribution, and relentless innovation to maintain their edge. For example, Lux's new Stratos technology cuts palm oil content by 25%, boosting both skin protection and fragrance delivery. Meanwhile, Dove's Garden Tea Party Collection introduces fresh fragrances and formulations, broadening its appeal. Lifebuoy continues to focus on health and hygiene benefits, further solidifying its position in the market. Such innovations not only deepen consumer loyalty but also elevate product performance and value standards, making it tough for organic brands to match in price and functionality. Furthermore, the strong brand recall and emotional ties consumers have with these conventional soaps bolster their market stance, leaving scant room for organic alternatives. Consequently, organic soap brands struggle to carve out a significant market share, as many consumers stick with established names they view as reliable, convenient, and affordable.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Premium and Homemade Artisanal Soaps

- Increasing Preference for Organic Soaps Among Sensitive Skin Consumers

- Premium Pricing of Organic Soaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, bar soap is set to dominate the global organic soap market, capturing a substantial 95.29% share. This stronghold can be attributed to consumer familiarity, cost-effectiveness, and user-friendliness. Bar soap's supremacy is further bolstered by its manufacturing efficiency, extended shelf life, and straightforward packaging. These attributes resonate with both producers and consumers who are on the lookout for uncomplicated organic choices. Brands such as Alaffia, with their Lavender and Coconut-scented Good Soap Bar Multipack, and Green-Beauty Co., presenting Neem, Turmeric, and Charcoal bars, underscore the allure of bar soaps. Their gentle, natural formulations strike a balance between effectiveness and convenience, appealing to a diverse consumer demographic. This widespread preference across various demographics solidifies bar soap's foundational role in the organic soap market.

Paper soaps and strips are emerging as the fastest-growing segment, boasting a CAGR of 5.94% projected through 2031. Their rise is fueled by the convenience they offer to travelers, heightened hygiene concerns, and evolving lifestyles in the wake of the pandemic. Brands are pushing boundaries, introducing biodegradable paper substrates and concentrated formulations. These innovations ensure cleansing effectiveness while being mindful of the environment. A case in point is Bon Organics, which provides a 30-sheet pack of handmade paper leaflets, each coated with organic soap, catering to the on-the-go hand hygiene need. Additionally, novel formats like strip-based or dissolvable sheets are gaining momentum. These innovations not only cater to the demand for compact, eco-friendly, and TSA-compliant solutions but also address significant consumer concerns like portion control and contamination in shared spaces. This trajectory of innovation not only fuels the overall market growth but also complements the established bar soap segment.

In 2025, the mass segment dominates the global organic soap market, boasting a 62.10% share. Brands such as Dr. Bronner's, Tom's of Maine, Chagrin Valley, Crate 61 Organics, and Kirk's Original lead the charge. These brands provide affordable, non-luxury organic soaps, targeting consumers who prioritize eco-friendliness and effectiveness without the luxury price tag. Their consistent quality and broad availability have cemented their appeal across diverse demographics. Additionally, the mass segment benefits from strong distribution networks, ensuring accessibility in both urban and rural markets.

On the other hand, the premium segment is on an upward trajectory, forecasting a CAGR of 8.28% through 2031. This surge aligns with a wider trend in consumer goods, where genuine brand stories and artisanal methods justify higher price points. Brands like Flamingo Estate are at the forefront, showcasing products like their botanical bar soap, a handcrafted blend of Big Sur sea salt, French blue clay, poppy seeds, and organic peppermint. The premium segment's expansion is fueled by consumers' growing inclination to splurge on luxury personal care, prioritizing quality, sustainability, and distinct formulations. Furthermore, the segment is leveraging digital platforms and exclusive retail partnerships to enhance visibility and attract niche audiences.

The Organic Soap Market Report is Segmented by Product Form (Bar Soap, Paper Soaps, and Strips), Category (Mass, Premium), End Users (Adults, Kids), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores/Grocery Stores, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region holds a dominant 38.32% share of the global organic soap market, driven by rising disposable incomes, a cultural preference for natural ingredients, and a rapid adoption of e-commerce. This region not only leads in market share but also showcases the fastest growth rate, boasting a 6.24% CAGR projected through 2031. India and Indonesia emerge as key players, supplying organic oils and botanical extracts, while China's robust digital commerce infrastructure accelerates brand expansion. Meanwhile, Japan and South Korea are propelling the premium segment, driven by discerning consumers who prioritize and are willing to invest in innovative formulations. Brands like Taiwan's Mumu Bath, India's Nyassa, and South Korea's Binu Binu epitomize this trend, crafting soaps that harmoniously fuse traditional Asian ingredients with contemporary design.

North America and Europe, characterized as mature markets, witness steady growth bolstered by regulatory endorsements, such as the United States Department of Agriculture, organic certification, and EU organic standards. These regions not only champion innovation in sustainable packaging and ingredient transparency but also set global benchmarks, shaping product development worldwide. Noteworthy brands include the UK's Lush, celebrated for its handmade, cruelty-free ethos, and the U.S.-based Sodambi, which draws inspiration from traditional African recipes for its natural moisturizing bar soaps.

Emerging markets in South America, the Middle East, and Africa showcase diverse growth patterns. Brazil spearheads South America's ascent, rooted in its rich tradition of natural products and a burgeoning urban consumer base. The UAE and Saudi Arabia in the Middle East are witnessing a surge driven by rising disposable incomes and heightened health consciousness among the youth. In Africa, brands like Togo's Alaffia and U.S.-based Shea Terra Organics (sourcing directly from Africa) are making waves. Alaffia champions fair-trade, handcrafted African black soap, while Shea Terra Organics stays true to authenticity, crafting its African black soap with time-honored ingredients, including cocoa pod ash and shea butter.

- Dr. Bronner's Magic Soaps (Dr. Bronner's)

- Colgate-Palmolive Company (Tom's of Maine)

- The Clorox Company (Burt's Bees)

- Weleda AG

- Neal's Yard Remedies Limited

- Unilever PLC (Dr. Squatch

- SheaMoisture

- Nubian Heritage)

- L'Occitane International SA (L'Occitane en Provence)

- Pre de Provence SAS (Pre de Provence)

- Faith In Nature Limited (Faith In Nature)

- Laverana GmbH & Co. KG (lavera)

- The Hain Celestial Group Inc. (Jason)

- W.S. Badger Company Inc. (Badger)

- Sukin Naturals Pty Ltd (Sukin)

- Kneipp GmbH (Kneipp)

- S. C. Johnson & Son Inc. (Mrs. Meyer's)

- Lush Limited (Lush)

- The Body Shop International Limited (The Body Shop)

- Windmill Health Products LLC (Kiss My Face)

- L'Oreal S.A. (CeraVe)

- Herbivore Botanicals LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Natural and Chemical-Free Personal Care Products

- 4.2.2 Increasing Emphasis on Eco-Friendly and Sustainable Products

- 4.2.3 Growing Demand for Premium and Homemade Artisanal Soaps

- 4.2.4 Increasing Preference for Organic Soaps Among Sensitive Skin Consumers

- 4.2.5 Aggressive Marketing and Advertisement Campaigns

- 4.2.6 Innovation in Exotic Ingredients and Multifunctional Formulations

- 4.3 Market Restraints

- 4.3.1 Dominance of Conventional Soaps

- 4.3.2 Stringent Organic Certification Regulations

- 4.3.3 Premium Pricing of Organic Soaps

- 4.3.4 Raw Material Price Volatility and Supply Constraints

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Form

- 5.1.1 Bar Soap

- 5.1.2 Paper Soaps and Strips

- 5.2 Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 End Users

- 5.3.1 Adults

- 5.3.2 Kids

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convinence Stores/ Grocery Stores

- 5.4.3 Health and Beauty Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dr. Bronner's Magic Soaps (Dr. Bronner's)

- 6.4.2 Colgate-Palmolive Company (Tom's of Maine)

- 6.4.3 The Clorox Company (Burt's Bees)

- 6.4.4 Weleda AG

- 6.4.5 Neal's Yard Remedies Limited

- 6.4.6 Unilever PLC (Dr. Squatch; SheaMoisture; Nubian Heritage)

- 6.4.7 L'Occitane International SA (L'Occitane en Provence)

- 6.4.8 Pre de Provence SAS (Pre de Provence)

- 6.4.9 Faith In Nature Limited (Faith In Nature)

- 6.4.10 Laverana GmbH & Co. KG (lavera)

- 6.4.11 The Hain Celestial Group Inc. (Jason)

- 6.4.12 W.S. Badger Company Inc. (Badger)

- 6.4.13 Sukin Naturals Pty Ltd (Sukin)

- 6.4.14 Kneipp GmbH (Kneipp)

- 6.4.15 S. C. Johnson & Son Inc. (Mrs. Meyer's)

- 6.4.16 Lush Limited (Lush)

- 6.4.17 The Body Shop International Limited (The Body Shop)

- 6.4.18 Windmill Health Products LLC (Kiss My Face)

- 6.4.19 L'Oreal S.A. (CeraVe)

- 6.4.20 Herbivore Botanicals LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK