PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910680

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910680

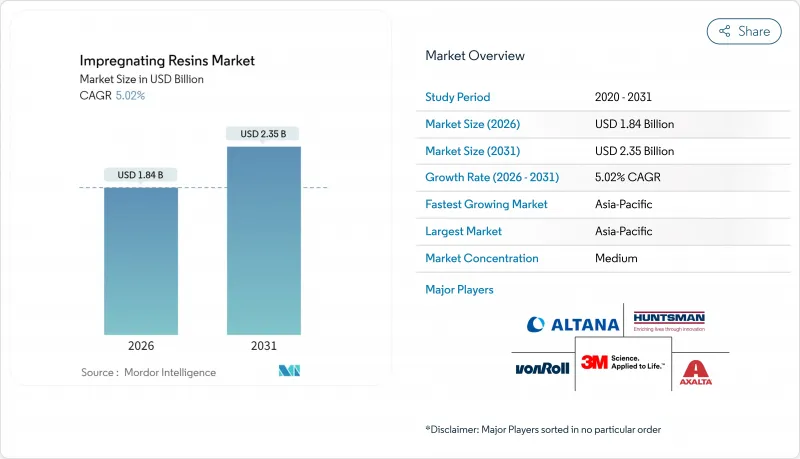

Impregnating Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Impregnating Resins Market was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.84 billion in 2026 to reach USD 2.35 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

Robust demand for high-efficiency electrical insulation in motors, generators, transformers, and power-electronics modules underpins this expansion. Original-equipment manufacturers increasingly specify vacuum pressure impregnation (VPI) systems that elevate dielectric strength and cut partial-discharge losses, supporting durable performance in renewables and e-mobility platforms. Scale-up of offshore wind turbines, higher-voltage electric vehicles, and smart-grid upgrades reinforce multi-year procurement pipelines for premium liquid insulation. Persistent capital requirements for advanced VPI equipment favor established players with vertically integrated resin and machinery offerings, gradually concentrating the impregnating resins market.

Global Impregnating Resins Market Trends and Insights

Surging Demand for High-Efficiency Electric Motors

Global regulations now mandate tighter loss limits for industrial motors; in the United States, updated Department of Energy rules require minimum nominal efficiencies across horsepower classes. These thresholds spur retrofits with VPI-treated windings that cut hot-spot temperatures, reduce vibration, and extend rewind intervals. Manufacturers consequently specify impregnating resins that tolerate 180 °C thermal classes and exhibit a low dissipation factor to meet energy audits. As plants chase operational expense reductions, the impregnating resins market sees stable aftermarket demand for rewind kits and field-service resins. Mid-size industrial hubs in Southeast Asia and Latin America replicate this replacement cycle, reinforcing the medium-term growth impulse.

OEM Shift Toward Solvent-Free Impregnation Processes

The U.S. Environmental Protection Agency's 2025 amendments on aerosol-coating reactivity, plus Europe's evolving VOC caps, accelerate the transition to 100% solids systems that release no regulated solvents. Solventless resins penetrate winding stacks efficiently under vacuum, polymerize faster under controlled heat, and remove worker-exposure liabilities, enabling ISO 14001 certification. Induction-heated trickle lines such as Gehring's IMFLEX illustrate process agility, cutting cycle times by 20% versus conventional dip-and-bake lines. Cost savings accrue from lower ventilation loads and simpler waste-treatment schemes, making solventless lines the de-facto capex choice for greenfield plants. These operational gains reinforce the impregnating resins market trajectory in developed and emerging economies alike.

VOC and HAPS Regulatory Tightening

Authorities worldwide keep lowering permissible VOC thresholds for industrial coatings; Canada's 2024 rules cap concentrations across 130 product classes, requiring reformulation or market withdrawal. Southern California's revised Rule 1151 on automotive coatings signals similar tightening for electrical-insulation applications, adding compliance documentation and lab-testing expenses. Smaller resin formulators often lack in-house environmental staff and solvent-recovery infrastructure, constraining their ability to compete for OEM contracts prioritizing green chemistry. Transition timelines of two years or less compress capital-planning windows, prompting some regional players to exit the impregnating resins market rather than absorb upgrade costs.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Scale Wind-Turbine Installation Growth

- Miniaturization of Consumer Electronics

- Price Volatility of Bisphenol-A and Styrene Feedstocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solventless formulations account for 64.12% of the impregnating resins market share in 2025, outpacing all alternatives with a 5.10% CAGR to 2031. This dominance derives from the ability of 100% solids chemistries to impregnate stator stacks under high vacuum without entrapped air pockets, yielding class H and class N thermal ratings. The resulting reduction in partial-discharge inception bolsters service lives of traction and wind-generator stators. Plant operators emphasize solvent elimination because it removes fire-code constraints and slashes exhaust-scrubber loads, shrinking operating costs within two years of retrofit.

Innovation pipelines continue to refine solventless rheology for automated trickling and roll-dip methods. Recent RSC-documented polyester networks achieve 331 °C onset degradation and 38% lower dielectric loss versus baseline, expanding suitability for high-frequency inverters. IEEE 275-1992 and 1553-2002 evaluation protocols guide OEM qualifications, ensuring that new resin grades integrate seamlessly with existing insulation systems. Solvent-based grades persist in niche rewind shops that value extended pot life, yet their share erodes annually as regulatory and insurance incentives favor solids technology. Consequently, producers that invested early in solventless assets enjoy pricing premiums and loyalty contracts, solidifying leadership positions across the global impregnating resins market.

The Impregnating Resins Report is Segmented by Technology (Solventless Resins and Solvent-Based Resins), Resin Type (Epoxy, Polyester, Polyester-Imide, and Other Resin Types), Application (Motors and Generators, Home Appliances, Transformers, Electrical and Electronic Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.20% of 2025 sales in the impregnating resins market and posts the quickest 5.11% CAGR to 2031. China's dominance in electric-motor production keeps regional demand vibrant, while targeted incentives for offshore wind clusters in Fujian and Guangdong provinces guarantee resin pull-through. India's performance incentives for high-efficiency appliances signal a sizable downstream opportunity as domestic manufacturers scale VPI lines. Southeast Asian nations leverage competitive labor costs and growing electronics exports to source localized impregnating capacity, anchoring regional supply chains that feed global OEM networks.

North America exhibits mature but resilient demand underpinned by automotive electrification, rebounding industrial capex, and grid modernization programs. Major resin suppliers now run U.S. and Mexican plants on renewable electricity, shrinking product carbon footprints and giving OEMs a Scope 3 emissions advantage. U.S. Department of Energy motor and transformer standards drive retrofits, translating regulatory action into predictable resin sales. Canada's VOC rules, effective 2024, further push solventless adoption, giving technologically advanced suppliers a market opening.

Europe navigates energy-price volatility yet sustains forward-looking policy drivers such as REACH Annex XVII formaldehyde limits effective 2026, which favor low-emission resins. Offshore-wind installation rates in the North Sea and Baltic Sea lock in high-performance silicone demand, partially offsetting weaker appliance production. Anti-dumping tariffs on foreign epoxy imports shore up domestic resin manufacturing, though they add cost pressure downstream. Overall, the impregnating resins market retains a balanced geographic footprint with Asia-Pacific's scale, North America's standards-driven upgrades, and Europe's environmental-technology leadership acting as complementary growth pillars.

- 3M

- AEV Group

- Axalta Coating Systems, LLC

- BASF

- Borger GmbH

- Chetak Manufacturing Company

- ALTANA (ELANTAS)

- Henkel AG and Co. KGaA

- Huntsman International LLC

- Momentive

- NIPPON RIKA INDUSTRIES CORPORATION

- Resonac Holdings Corporation

- Von Roll

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for High-Efficiency Electric Motors

- 4.2.2 OEM Shift toward Solvent-Free Impregnation Processes

- 4.2.3 Grid-Scale Wind-Turbine Installation Growth

- 4.2.4 EV Traction-Motor Production Acceleration

- 4.2.5 Miniaturisation of Consumer Electronics

- 4.3 Market Restraints

- 4.3.1 VOC and HAPS Regulatory Tightening

- 4.3.2 Price Volatility of Bisphenol-A and Styrene Feedstocks

- 4.3.3 Capital-Intensive Vacuum-Pressure Equipment

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Solventless Resins

- 5.1.2 Solvent-based Resins

- 5.2 By Resin Type

- 5.2.1 Epoxy

- 5.2.2 Polyester

- 5.2.3 Polyester-imide

- 5.2.4 Other Resin Types (Polyurethane, silicone, etc.)

- 5.3 By Application

- 5.3.1 Motors and Generators

- 5.3.2 Home Appliances

- 5.3.3 Transformers

- 5.3.4 Electrical and Electronic Components

- 5.3.5 Automotive Components

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 AEV Group

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 BASF

- 6.4.5 Borger GmbH

- 6.4.6 Chetak Manufacturing Company

- 6.4.7 ALTANA (ELANTAS)

- 6.4.8 Henkel AG and Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 Momentive

- 6.4.11 NIPPON RIKA INDUSTRIES CORPORATION

- 6.4.12 Resonac Holdings Corporation

- 6.4.13 Von Roll

- 6.4.14 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment