PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910681

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910681

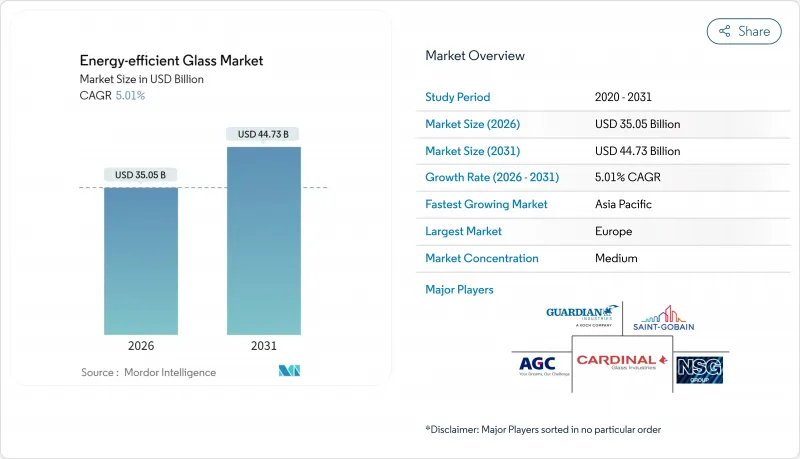

Energy-efficient Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Energy-efficient Glass market size in 2026 is estimated at USD 35.05 billion, growing from 2025 value of USD 33.38 billion with 2031 projections showing USD 44.73 billion, growing at 5.01% CAGR over 2026-2031.

Growth flows from stricter building-energy codes, green-building certifications, and the automotive shift to low-E glazing that extends electric-vehicle range. Technological gains in vacuum-insulated glass retrofits, the EU Carbon Border Adjustment Mechanism, and multi-layer silver coatings sustain product differentiation while protecting margins despite raw-material volatility. Producers with magnetron-sputter capacity enjoy pricing power as equipment lead times stretch up to three years. Simultaneously, collaborations between glassmakers and photovoltaic innovators unlock building-integrated solar facades that satisfy net-zero goals and open new revenue pools.

Global Energy-efficient Glass Market Trends and Insights

Stricter Global Building-Energy Codes

The latest International Energy Conservation Code trims allowable window U-factors by up to 17%, pushing architects toward low-E triple panes and vacuum solutions. California's 2025 Title 24 limits vertical fenestration U-factors to 0.47, a level achievable only with advanced soft-coat glazing. Canada's path to net-zero-ready buildings by 2030 sets a 0.27 target for fixed windows, accelerating triple-glazing demand. These codes eliminate loopholes that once permitted trade-offs, so performance now outweighs upfront cost during specification. Suppliers with multi-silver stacks find greater leverage as code updates proliferate across Asia-Pacific capitals. Compliance deadlines over the medium term underpin a dependable order pipeline for high-performance units.

Growth in Green-Building Certifications (LEED, BREEAM)

Certification frameworks reward envelope efficiency and embodied-carbon transparency. LEED v4.1 credits hinge on Environmental Product Declarations, nudging fabricators to quantify carbon footprints. The United States Green Building Council estimates USD 35 trillion must flow into net-zero assets by 2030, much of it earmarked for facades that cut operational loads. BREEAM Outstanding landmarks such as London's Crystal achieve U-values near 1.0 W/m2K, highlighting how advanced glazing delivers certification points that translate into rental premiums. Developers now value total cost of ownership over headline material prices, reinforcing demand for low-emissivity products.

High Upfront Cost Versus Conventional Float Glass

Premium coatings and multiple panes lift prices 40-80% above standard float, constraining adoption where first-cost sensitivity dominates. Triple units carry 15-25% mark-ups over double panes, while VIG commands 200-300% premiums, placing it mostly in high-spec commercial projects. Emerging markets often defer performance gains for capital savings, slowing near-term volume. Yet escalating utility tariffs and nascent carbon pricing are shortening payback horizons, easing resistance. Public-sector subsidies and concessional lending further erode the cost barrier, particularly in retrofits targeting energy-poverty households.

Other drivers and restraints analyzed in the detailed report include:

- OEM Demand for Low-E Glazing in EVs

- EU CBAM Favoring Low-Carbon Flat-Glass Supply Chains

- Limited Global Magnetron-Sputter Coating Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft-coat products held 61.82% share of the energy-efficient glass market in 2025 and are growing at a 5.51% CAGR through 2031, reflecting unmatched emissivity below 0.04 and compatibility with multi-pane assemblies. The energy-efficient glass market size attached to soft-coat offerings is forecast to expand steadily as building codes ratchet down window U-factors. Advanced multi-silver stacks optimize solar heat-gain coefficients without sacrificing visible transmittance, appealing to both office towers seeking daylighting and EV makers requiring cabin comfort. Hard-coat pyrolytic glass remains relevant in monolithic storefronts and regions with modest efficiency requirements where durability and scratch resistance outweigh thermal targets. Suppliers continually refine sputter uniformity across jumbo lites, using closed-field cathode arrays that cut edge haze and reduce yield loss.

A surge in automotive demand further cements soft-coat ascendance. Low-E windshields are now factory-specified by premium EV brands, and regulatory frameworks such as ISO 9050 harmonize performance metrics globally, shortening qualification cycles. However, sputter-line scarcity tempers supply, prompting mergers and long-term offtake agreements that lock in allocations. Tier-one float producers leverage vertical integration to control silver supply chains, minimizing cost spikes. Should capital commitments lag demand, spot premiums for high-selectivity coatings may persist well into the forecast horizon.

The Energy-Efficient Glass Report is Segmented by Coating Type (Hard-Coat Pyrolytic and Soft-Coat Magnetron-Sputtered), Glazing Type (Single, Double, and Triple), End-User Industry (Building and Construction, Automotive, Solar Panel, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 34.21% share of the energy-efficient glass market in 2025 on the back of the EU Energy Performance of Buildings Directive that requires near-zero-energy new builds. Germany and the UK drove specification with updated Part L rules, while France's RE2020 prioritized embodied carbon, steering orders toward low-carbon float made with electric furnaces.

Asia-Pacific posts the briskest 5.76% CAGR through 2031 as China alone accounts for roughly half of global new construction. Stringent Tier-1 city codes now reference triple-pane performance, and India's Smart Cities Mission fosters green-building certifications that spotlight envelope efficiency.

North America records steady gains aided by tax credits under the U.S. Inflation Reduction Act and Canada's net-zero-ready roadmap. Title 24 in California and city-level building-performance standards across the Northeast anchor retrofit pipelines. South America and the Middle East and Africa remain smaller but strategic: rising energy tariffs and extreme-climate cooling needs boost solar-control glazing uptake, though local fabrication capacity still lags demand.

- Abrisa Technologies

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- Corning Incorporated

- Fuyao Group

- Guardian Industries Holdings

- Morley Glass & Glazing Ltd

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- ?i?ecam

- TuffX Glass

- Vitro

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter global building-energy codes

- 4.2.2 Growth in green-building certifications (LEED, BREEAM)

- 4.2.3 OEM demand for low-E glazing in EVs

- 4.2.4 Rapid retrofit uptake of vacuum-insulated glass (VIG)

- 4.2.5 EU CBAM favouring low-carbon flat-glass supply chains

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. conventional float glass

- 4.3.2 Volatile soda-ash and energy prices impacting margins

- 4.3.3 Limited global magnetron-sputter coating capacity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Coating Type

- 5.1.1 Hard-coat (pyrolytic)

- 5.1.2 Soft-coat (magnetron-sputtered)

- 5.2 By Glazing Type

- 5.2.1 Single

- 5.2.2 Double

- 5.2.3 Triple

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Solar Panel

- 5.3.4 Other End-user Industries (Industrial, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abrisa Technologies

- 6.4.2 AGC Inc.

- 6.4.3 CARDINAL GLASS INDUSTRIES, INC

- 6.4.4 Central Glass Co., Ltd.

- 6.4.5 Corning Incorporated

- 6.4.6 Fuyao Group

- 6.4.7 Guardian Industries Holdings

- 6.4.8 Morley Glass & Glazing Ltd

- 6.4.9 Nippon Sheet Glass Co., Ltd

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 ?i?ecam

- 6.4.13 TuffX Glass

- 6.4.14 Vitro

- 6.4.15 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment