PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910717

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910717

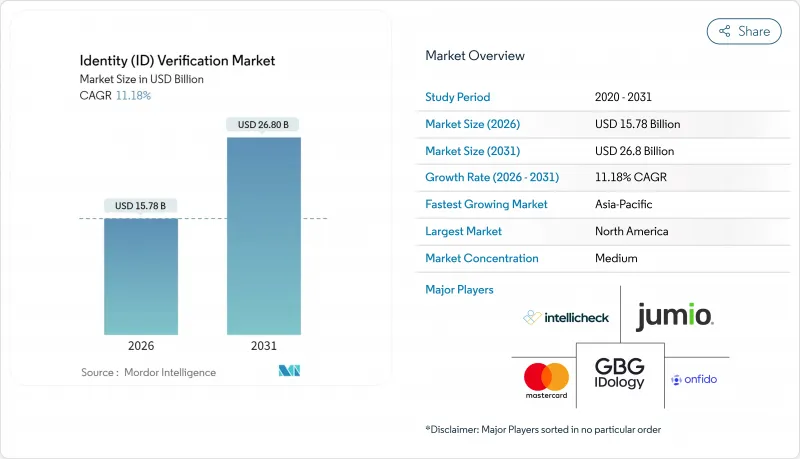

Identity (ID) Verification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The identity verification market is expected to grow from USD 14.19 billion in 2025 to USD 15.78 billion in 2026 and is forecast to reach USD 26.8 billion by 2031 at 11.18% CAGR over 2026-2031.

The expansion reflects a decisive shift from checkbox compliance toward strategic security investment as enterprises confront AI-generated fraud, deepfake attacks, and rising regulatory fines. Deepfakes alone jumped 3,000%, compelling vendors to embed passive liveness and behavioral analytics directly into onboarding workflows. Cloud-native deployment, now the default choice for most new rollouts, accelerates innovation because model updates can be pushed instantly across global tenants. Meanwhile, demand for portable, privacy-preserving credentials is spurring pilots that link government-issued mobile driver's licenses, verifiable credentials, and Web3 wallets into a single user journey. Consolidation is intensifying as full-stack security firms buy niche specialists to acquire AI document-forensics talent, yet no provider controls more than 15% revenue, leaving ample headroom for focused entrants that solve edge-case risks or industry-specific regulations.

Global Identity (ID) Verification Market Trends and Insights

Increasing Cyber-Fraud and Regulatory Fines

Fraudulent account openings spiked to 2.1% of financial transactions in 2024, a sharp rise from 1.27% two years earlier.An estimated 42.5% of detected fraud events now leverage generative AI, which forces banks to deploy multi-layer defences that spot synthetic IDs and deepfake voices in real time. Regulators are equally assertive: global institutions paid USD 6.6 billion in KYC-related penalties during 2023. The combined pressure of higher risk and higher fines is pushing buyers toward enterprise-grade orchestration platforms that integrate document forensics, biometric liveness, and continuous behavioural monitoring in a single API.

Surge in Remote Onboarding and e-KYC Mandates

Seventy-eight percent of APAC consumers deem digital identity checks essential before using new financial apps. Regulators are codifying that preference: the EU requires every member state to issue a Digital Identity Wallet within 24 months, effectively institutionalising electronic KYC. Organisations that automate verification cut service-desk handle times by up to 45 seconds, as a top-10 US bank confirmed after rolling out voice authentication. Network effects then arise when verified credentials become transferable across providers, halving repeat onboarding friction and reinforcing platform scale advantages.

Fragmented Global Regulatory Standards

KYC rules vary not only by country but sometimes by banking supervisor inside the same region, forcing platforms to run parallel verification flows and data-residency architectures. The United States stresses portability, whereas EU GDPR pushes localisation, complicating unified cloud deployments. In Asia, Japan insists on FSA licences while South Korea demands bank partnerships for cryptocurrency exchanges. As compliance teams juggle this patchwork, expansion timetables lengthen and operating costs rise.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Accuracy Improvements in Document Forensics

- Cross-Border Digital ID Interoperability Pilots

- Deepfake and Generative-AI Spoofing Threats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment captured 65.12% identity verification market share in 2025 and is expanding at a 12.72% CAGR as firms prefer elastic consumption to capital-heavy servers. The identity verification market size associated with cloud deployments is projected to reach USD 18.7 billion by 2031, reflecting rapid API adoption among digital banks and gig-economy platforms. Continuous model updates, centralised threat-intel sharing, and zero-downtime patching position cloud as the reference architecture. On-premise remains mandatory only where statutes mandate local data processing, yet even those jurisdictions accept cloud when providers open certified regional centres.

Resilience is another driver. Mastercard analyses 143 billion annual transactions to update anomaly-scoring routines that instantly benefit every tenant. Cloud hubs also simplify integration with verifiable credentials and mobile driver's licenses, cutting project timelines from months to weeks. As edge data centres proliferate, latency concerns fade, allowing cloud adoption even for biometric video streams that demand sub-second round-trip times.

Biometric engines held 35.84% of identity verification market share in 2025 and post a 12.86% CAGR through 2031, outpacing document-only approaches. The identity verification market size tied to biometric modalities is forecast to surpass USD 10.1 billion by 2031, driven by passive liveness that operates invisibly in background video frames. Vendors blend facial, voice, and behavioural signals to deliver continuous authentication, narrowing the attack surface for account takeover.

Document checks will persist yet increasingly act as a secondary step. Providers like Aware release real-time synthetic-media detection that flags GPU-rendered artefacts invisible to the naked eye Aware. Financial institutions deploying multi-modal biometrics report 250% accuracy gains, which lowers manual review cost and boosts customer conversion. Knowledge-based questions and static database lookups now serve niche use cases such as low-risk age gating.

Identity Verification Market is Segmented by Deployment (On-Premises, Cloud), Solution Type (Document / ID Verification, Biometric Verification, and More), End User Industry (Financial Services (BFSI), Retail and E-Commerce, and More), Organization Size (Large Enterprises, Small and Medium Enterprises (SMEs)), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 32.43% identity verification market share in 2025, buoyed by aggressive fraud enforcement and early biometric rollouts. The United States plans nationwide mobile driver's license acceptance at TSA checkpoints from May 2025, signalling federal confidence in digital credentials. Canada's open-banking roadmap further accelerates cross-platform identity portability.

Asia-Pacific stands out with 11.52% CAGR, propelled by Singapore's fintech sandbox, India's Aadhaar-linked payment rails, and Japan's FSA crypto rules. Trulioo reached a 90% business-verification rate after opening its Singapore hub, illustrating demand for regional KYC APIs. Rising smartphone penetration and real-time payment schemes make APAC the largest incremental revenue pool over the forecast horizon.

- Mastercard

- Onfido

- GBG (Idology)

- Intellicheck

- Jumio

- Trulioo

- Mitek Systems

- Veriff

- IBM

- AuthenticID

- Experian

- TransUnion

- LexisNexis Risk Solutions

- Pindrop

- ComplyCube

- Nuance Communications

- Thales Group

- IDEMIA

- Okta

- Ping Identity

- Equifax

- NEC Corporation

- Acuant

- Persona

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing cyber-fraud and regulatory fines

- 4.2.2 Surge in remote onboarding and e-KYC mandates

- 4.2.3 AI-driven accuracy improvements in document forensics

- 4.2.4 Cross-border digital ID interoperability pilots

- 4.2.5 Fintech inclusion programmes in emerging markets

- 4.2.6 Rise of verifiable credentials and Web3 identity wallets

- 4.3 Market Restraints

- 4.3.1 Fragmented global regulatory standards

- 4.3.2 Deepfake and generative-AI spoofing threats

- 4.3.3 High integration cost for legacy core systems

- 4.3.4 Data-sovereignty barriers limiting cloud roll-outs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Solution Type

- 5.2.1 Document / ID Verification

- 5.2.2 Biometric Verification

- 5.2.3 Authentication and Liveness

- 5.2.4 Others

- 5.3 By End-user Industry

- 5.3.1 Financial Services (BFSI)

- 5.3.2 Retail and E-commerce

- 5.3.3 Government and Public Sector

- 5.3.4 Healthcare

- 5.3.5 Telecom and IT

- 5.3.6 Others

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mastercard

- 6.4.2 Onfido

- 6.4.3 GBG (Idology)

- 6.4.4 Intellicheck

- 6.4.5 Jumio

- 6.4.6 Trulioo

- 6.4.7 Mitek Systems

- 6.4.8 Veriff

- 6.4.9 IBM

- 6.4.10 AuthenticID

- 6.4.11 Experian

- 6.4.12 TransUnion

- 6.4.13 LexisNexis Risk Solutions

- 6.4.14 Pindrop

- 6.4.15 ComplyCube

- 6.4.16 Nuance Communications

- 6.4.17 Thales Group

- 6.4.18 IDEMIA

- 6.4.19 Okta

- 6.4.20 Ping Identity

- 6.4.21 Equifax

- 6.4.22 NEC Corporation

- 6.4.23 Acuant

- 6.4.24 Persona

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment