PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910721

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910721

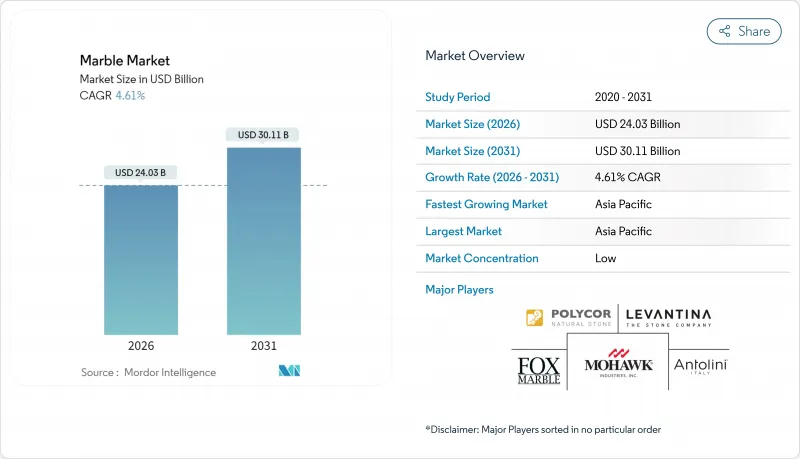

Marble - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Marble Market was valued at USD 22.97 billion in 2025 and estimated to grow from USD 24.03 billion in 2026 to reach USD 30.11 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

Growth in Asia-Pacific, where the marble market is driven by rapid urban expansion and infrastructure spending, is predicted to outpace all other regions at a 6.16% CAGR. Intensifying consolidation among established quarriers and processors is intersecting with agile technology-led entrants that apply digital extraction, water recycling, and predictive maintenance to cut costs and waste. At the same time, stricter silica-dust regulations are reshaping operating practices and capital budgets, particularly in North America and Europe.

Global Marble Market Trends and Insights

Rapid Growth in the Construction Industry

Construction spending is cascading into higher marble demand as developers specify premium stone for floors, walls, and countertops in luxury homes and mixed-use towers. Governments across Asia-Pacific continue to funnel budget into transport hubs and civic buildings that feature large-format stone cladding, lifting structural as well as decorative usage. Prefabricated marble panels, factory-cut to tight tolerances, are saving installation time and reducing on-site breakage, helping contractors meet schedule guarantees. Thin 3-5 mm veneers are opening high-rise facades to lighter loads, and marble-concrete composites are appearing in projects seeking green-building certifications due to weight and embodied-carbon advantages, supporting the growth in the marble market.

Increase in Luxury Real Estate and Infrastructure Projects

Luxury hospitality groups and premium office developers are turning to distinctive stone to craft memorable entrances, wellness areas, and dining venues. Designers working on five-star hotels in Dubai, Singapore, and New York specify statement slabs with dramatic veining because natural variance signals exclusivity to guests. Boutique brands extend the same ethos to small properties, boosting demand for rare colors that differentiate from engineered look-alikes, reflecting growth in the marble market.

Health Hazard Related to Marble Dust

Respirable crystalline silica generated during cutting and polishing is under heightened scrutiny after California recorded 127 silicosis cases and 13 fatalities by April 2024, prompting new exposure limits and mandated wet-cutting protocols. Although natural marble contains less than 10% silica, regulators are applying similar controls across all stone operations. Compliance costs include enclosed workstations, high-vacuum extraction, and personal monitoring systems, pressuring small fabricators that lack the capital to upgrade in the marble market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Marble Powder as Supplementary Cementitious Material

- Technological Advancements in Extraction and Processing

- Competition from Synthetic Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic grades dominated 80.65% of the marble market in 2025 as industrial resin systems reproduced the look of premium Carrara and Calacatta while providing hardness and stain resistance. The segment is projected to extend leadership at a 4.72% CAGR, supported by home-center channels and accelerated fabrication. Natural marble stays relevant in projects where authenticity and long-term patina outweigh maintenance concerns. Designers of flagship hotels and bespoke residences still specify large blocks for reception desks, staircases, and sculpture. Countries such as Brazil have improved quarry yield through wire saws and drone mapping, bringing new white marble varieties to global showrooms.

White stones captured 36.02% of demand in 2025 and are on track for a 5.60% CAGR through 2031, significantly above the marble market. Designers cite neutrality, light reflectance and association with classical architecture as key reasons for preference, particularly in wellness spas and minimalist corporate lobbies. The marble market size for white varieties is expanding in China and the Gulf, where bright interiors counter hot climates.

Black marbles, led by Nero Marquina, secure orders for contrast features in retail flagships and penthouse kitchens. Yellow, red, and green types cater to regional tastes in the Middle East and parts of Asia, often tied to local cultural symbolism. Multicolored and brecciated stones attract avant-garde architects seeking statement walls. Color choice is increasingly curated through digital twin libraries that allow clients to preview entire slabs at the design stage, reducing uncertainty and waste.

The Marble Market Report Segments the Industry by Product Type (Natural Marble and Synthetic/Artificial Marble), Color (White, Black, Yellow, Red, and Other Colors), Application (Building and Decoration, Statues and Monuments, and More), End-User Sector (Residential Buildings, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 33.62% of the marble market in 2025 and is forecast to post the highest 6.10% CAGR. India's smart-city roll-out and Indonesia's new capital development add fresh demand for flooring and facade stone. Producers in Vietnam and Pakistan are expanding quarry output to meet regional specifications.

Europe is anchored by Italy and Turkey. Carrara delivers iconic whites, yet waste remains a pain point, with up to 70% of extracted mass discarded as sludge. Regulation and social pressure are catalyzing investment in water recycling, dry shaping, and waste-to-product initiatives such as marble-based 3D printing filament. German and Spanish processors market verified low-emission stone to architects pursuing green certifications.

North America maintains premium pricing and a tight supply of distinctive varieties. Demand centers on luxury residential towers, boutique hotels, and upmarket retail.

South America is emerging as a supply hub, with Brazil's white quartzites and marble winning specifications in US and European projects. The Middle East and Africa show robust demand linked to mega-projects in Saudi Arabia, the United Arab Emirates and South Africa.

- Antolini Luigi & C. S.p.a.

- BC Marble Products Ltd

- Best Cheer Stone Group

- China Kingstone Mining Holdings Limited

- Dimpomar

- Eco Buildings Group Plc

- F.H.L.

- Fox Marble

- HELLENIC GRANITE Co

- Hilltop Stones Pvt. Ltd.

- Kangli stone group

- Levantina y Asociados de Minerales, S.A.

- Mohawk Industries, Inc.

- Mumal Marbles Pvt. Ltd.

- NQ Acrylic and Stone

- Polycor Inc.

- Santucci Group Srl

- TEKMAR MERKEZ OF?S

- Temmer Marble

- Topalidis S.A.

- UMGG

- XISHI GROUP LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth in the Construction Industry

- 4.2.2 Increase in Luxury Real Estate and Infrastructure Projects

- 4.2.3 Rising Adoption of Marble powder as Supplementary Cementitious Material for Low-carbon Concrete

- 4.2.4 Growing Inclination on Marble as a Natural and Sustainable Material

- 4.2.5 Technological Advancements in Extraction and Processing Driving Growth in the Marble Industry

- 4.3 Market Restraints

- 4.3.1 Health Hazard Related to Marble Dust

- 4.3.2 Competition from Synthetic Alternatives

- 4.3.3 Waste Generation and Recycling Challenges

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Trade Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Natural Marble

- 5.1.2 Synthetic/Artificial Marble

- 5.2 By Color

- 5.2.1 White

- 5.2.2 Black

- 5.2.3 Yellow

- 5.2.4 Red

- 5.2.5 Other Colors

- 5.3 By Application

- 5.3.1 Building and Construction

- 5.3.2 Statues and Monuments

- 5.3.3 Furniture

- 5.3.4 Other Applications (Decorative Infrastructure)

- 5.4 By End-user Sector

- 5.4.1 Residential Buildings

- 5.4.2 Commercial and Hospitality

- 5.4.3 Industrial and Institutional

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Turkey

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, Partnerships, Quarry Integration)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Antolini Luigi & C. S.p.a.

- 6.4.2 BC Marble Products Ltd

- 6.4.3 Best Cheer Stone Group

- 6.4.4 China Kingstone Mining Holdings Limited

- 6.4.5 Dimpomar

- 6.4.6 Eco Buildings Group Plc

- 6.4.7 F.H.L.

- 6.4.8 Fox Marble

- 6.4.9 HELLENIC GRANITE Co

- 6.4.10 Hilltop Stones Pvt. Ltd.

- 6.4.11 Kangli stone group

- 6.4.12 Levantina y Asociados de Minerales, S.A.

- 6.4.13 Mohawk Industries, Inc.

- 6.4.14 Mumal Marbles Pvt. Ltd.

- 6.4.15 NQ Acrylic and Stone

- 6.4.16 Polycor Inc.

- 6.4.17 Santucci Group Srl

- 6.4.18 TEKMAR MERKEZ OF?S

- 6.4.19 Temmer Marble

- 6.4.20 Topalidis S.A.

- 6.4.21 UMGG

- 6.4.22 XISHI GROUP LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Use of Marble Slabs and Powder