PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910806

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910806

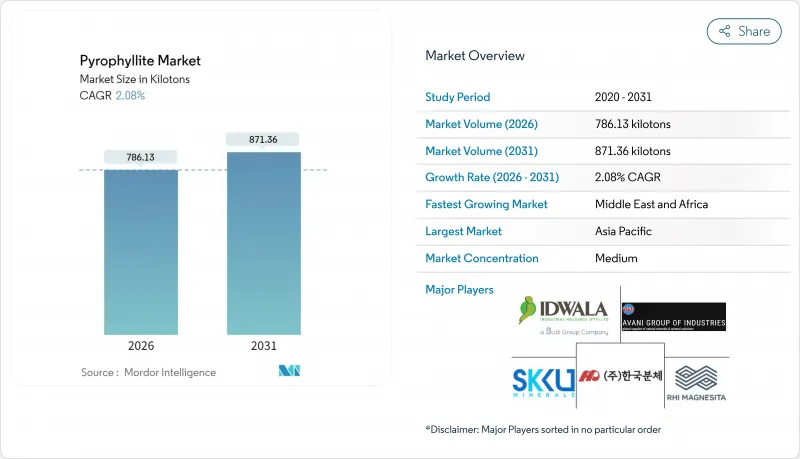

Pyrophyllite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Pyrophyllite Market was valued at 770.11 kilotons in 2025 and estimated to grow from 786.13 kilotons in 2026 to reach 871.36 kilotons by 2031, at a CAGR of 2.08% during the forecast period (2026-2031).

This steady expansion reflects the mineral's dependable physical attributes-thermal stability, chemical inertness, and low-shrinkage behavior-that help industrial users maintain reproducible product quality. Demand growth is anchored in Asia-Pacific, where ceramics capacity build-outs and electric-arc steelmaking together keep throughput volumes high. Solid-state battery ceramics and high-build protective coatings create incremental demand points that offset slower growth in legacy filler uses. Intensifying regulatory oversight of respirable crystalline silica raises mining costs, yet also elevates quality-control standards that favor well-capitalized suppliers with robust dust-mitigation technology. Competitive consolidation-illustrated by RHI Magnesita's 2024 purchase of Resco Products-reinforces supply security for large refractory buyers, underlining the pyrophyllite market's role as a strategic materials platform.

Global Pyrophyllite Market Trends and Insights

Ceramics Capacity Build-out in Asia-Pacific

Robust expansions in tile and sanitary-ware lines throughout China and India underpin the pyrophyllite market by absorbing large volumes into triaxial porcelain mixes. Producers cite up to 24% strength gains over kaolin-based recipes, enabling lighter-weight products that cut logistics costs. Shorter firing cycles further lower energy consumption and trim carbon footprints in line with regional decarbonization policies. As government stimulus pushes affordable housing, tile makers secure forward contracts that lock in pyrophyllite at predictable terms, shielding them from kaolin price swings. The mineral's predictable thermal conversion to mullite also minimizes glaze defects, supporting premium tile SKUs that command higher margins. These structural gains make the pyrophyllite market integral to Asia-Pacific's ceramic competitiveness.

Rising Refractory Demand in Electric-Arc Steelmaking

Electric-arc furnaces now account for a growing share of crude steel output, and each unit requires ladle and tundish refractories that resist rapid thermal cycling. Japanese steelmakers have relied on pyrophyllite (locally called roseki) for decades, validating its mullite-forming behavior under 1,600 °C service loads. New EAF rollouts across India and Southeast Asia replicate those material specifications, driving regional procurement contracts. Multinational refractory houses hedge supply risk through vertical integration, as seen in RHI Magnesita's 2024 U.S. asset acquisition. As steel mills intensify scrap melting to curtail Scope 1 emissions, the pyrophyllite market enjoys tailwinds that reinforce its refractory franchise.

Occupational Dust-Hazard Regulations

The U.S. Mine Safety and Health Administration in 2024 cut allowable respirable crystalline silica levels to 50 μg/m3 and mandated action at 25 μg/m3, triggering new engineering controls and medical surveillance obligations. European directives align closely, making compliance a global imperative. Upgrading ventilation, installing baghouse filters, and conducting ISO-compliant monitoring impose capital outlays that weigh on margins, especially for mid-tier miners. However, larger operators leverage these mandates to differentiate via third-party certified "low-dust" supply programs, potentially consolidating share within the pyrophyllite market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Mineral Fillers for High-Build Industrial Coatings

- Shift from Talc to Pyrophyllite in Cosmetics After Asbestos Litigation

- Abundant Substitute Minerals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural grades constituted 86.64% of the pyrophyllite market in 2025 on the strength of straightforward crushing-and-screening flowsheets that keep delivered-cost economics favorable. Rajasthan and North Carolina mines anchor global trade, supplying refractory and ceramic plants directly with minimal upgrading. These volumes underpin baseline growth that aligns with macro industrial output.

Processed "other" grades occupy a smaller base yet outpace natural grades at a 2.68% CAGR to 2031. Producers deploy magnetic separation, flotation, and de-ionized water washing to slash iron to below 0.4 wt%, unlocking advanced uses such as translucent spark-plug insulators and solid-state electrolyte frameworks. Microwave roasting coupled with wet-high-intensity magnetic separation achieves 96% iron removal, widening acceptance among electronics manufacturers. Dual-product strategies let miners monetize the pyrophyllite market's commodity tier while capturing specialty margins, ultimately strengthening their revenue mix.

The Pyrophyllite Market Report is Segmented by Type (Natural Pyrophyllite, Other Types), Application (Ceramics, Refractory, Filler Materials, Fiberglass, Rubber and Roofing, Fertilizers, Ornamental Stones, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 75.50% of 2025 consumption, underpinned by integrated mine-to-kiln supply chains in China, India, and Japan. India alone produced roughly 150,000 tons, equal to 24-25% of global output, conferring raw-material security to regional ceramics clusters. Chinese tile producers, accounting for half of world ceramic-tile shipments, front-load annual purchase contracts to lock in freight advantage. Concurrently, Japan leverages high-purity roseki for niche refractories in continuous-casting operations, underscoring the region's sophisticated application spectrum.

The Middle East and Africa is the fastest-growing geography at 2.74% CAGR through 2031. Gulf Cooperation Council infrastructure visions push tile demand, while North African steel mini-mills specify local refractory supply to cut import reliance. Mineral developers in South Africa and Morocco survey aluminous schist belts for new deposits, aiming to foster indigenous feedstock streams that could recalibrate trade flows into the pyrophyllite market.

North America sustains modest growth amid stringent federal silica rules that lift compliance costs but incentivize best-available-control-technology adoption. Appalachian operators bank on proximity to midwestern steel customers, whereas West-Coast ports facilitate Asian exports of upgraded powders. Europe focuses on high-margin technical ceramics and specialty coatings, importing value-added grades from India when local deposits lack required purity. South America's latent potential rests on Brazil's 45.153 million-ton talc-and-pyrophyllite reserve base, which underpins future domestic beneficiation hubs once downstream demand scales.

- Anand Talc

- Avani Group

- Hankook Mineral Powder Co. Ltd.

- Hebei Yayang Spodumene Co., Ltd.

- Idwala Industrial Holdings

- Jinhae Pyrophyllite

- Liaoyuan Pharmaceutical Co., Ltd.

- NINGBO INNO PHARMCHEM CO., LTD.

- PT Gunung Bale

- R.T. Vanderbilt Holding Company, Inc.

- RHI Magnesita

- SAMIROCK Company

- SEPRA

- SKKU Minerals

- Wonderstone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ceramics capacity build-out in Asia

- 4.2.2 Rising refractory demand in electric-arc steelmaking

- 4.2.3 Lightweight mineral fillers for high-build industrial coatings

- 4.2.4 Shift from talc to pyrophyllite in cosmetics after asbestos litigation

- 4.2.5 Solid-state battery ceramics requiring high-purity Al-Si feedstocks

- 4.3 Market Restraints

- 4.3.1 Occupational dust-hazard regulations

- 4.3.2 Abundant substitute minerals (talc, kaolin, feldspar)

- 4.3.3 Scarcity of low-iron, high-Al2O3 ore bodies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Natural Pyrophyllite

- 5.1.2 Other Types

- 5.2 By Application

- 5.2.1 Ceramics

- 5.2.2 Refractory

- 5.2.3 Filler Materials (Paper, Paints, Insecticides)

- 5.2.4 Fiberglass

- 5.2.5 Rubber and Roofing

- 5.2.6 Fertilizers (Soil Conditioners)

- 5.2.7 Ornamental Stones

- 5.2.8 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anand Talc

- 6.4.2 Avani Group

- 6.4.3 Hankook Mineral Powder Co. Ltd.

- 6.4.4 Hebei Yayang Spodumene Co., Ltd.

- 6.4.5 Idwala Industrial Holdings

- 6.4.6 Jinhae Pyrophyllite

- 6.4.7 Liaoyuan Pharmaceutical Co., Ltd.

- 6.4.8 NINGBO INNO PHARMCHEM CO., LTD.

- 6.4.9 PT Gunung Bale

- 6.4.10 R.T. Vanderbilt Holding Company, Inc.

- 6.4.11 RHI Magnesita

- 6.4.12 SAMIROCK Company

- 6.4.13 SEPRA

- 6.4.14 SKKU Minerals

- 6.4.15 Wonderstone

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment