PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910823

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910823

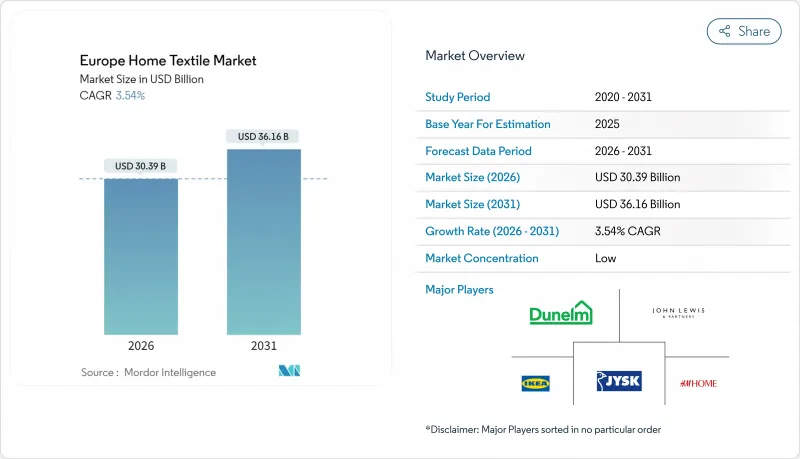

Europe Home Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Europe home textile market size in 2026 is estimated at USD 30.39 billion, growing from 2025 value of USD 29.35 billion with 2031 projections showing USD 36.16 billion, growing at 3.54% CAGR over 2026-2031.

Renovation incentives, hospitality recovery, and circular-economy legislation are reshaping procurement strategies, allowing established and challenger brands to capture new demand pockets. Budget hotel expansion, coupled with e-commerce-driven decor cycles, is shortening replacement intervals and lifting average volumes even when discretionary spending softens. Record flax cultivation and expanding recycled-fiber capacity are lowering entry prices for sustainable materials, encouraging mainstream adoption in both residential and commercial settings. Competitive dynamics remain fragmented as retailers balance affordability programs against premium innovation, while direct-to-business channels grow as institutional buyers prioritize traceability.

Europe Home Textile Market Trends and Insights

EU-Wide Renovation Wave Boosting Replacement Demand

The European Commission aims to renovate 35 million buildings by 2030, and each deep retrofit triggers holistic interior upgrades that routinely include textiles. Homeowners replacing windows and insulation often synchronize purchases of premium bed linen, curtains, and upholstery to align with refreshed decor schemes. Higher project budgets lift average selling prices, enabling manufacturers to plan capacity around predictable multi-year pipelines. Design advisers embedded in renovation teams are standardizing specification lists, streamlining supplier onboarding, and shortening lead times. Consequently, the Europe home textile market benefits from a steadier order cadence that reduces inventory risk for mills and converters.

Growing Footprint of Budget Hotel Chains Spurring Linen Refresh Cycles

Normalized RevPAR levels allow budget chains to reinstate 18-24-month linen replacement programs, a cadence far shorter than luxury hotels' three-year norm. Centralized e-procurement tools aggregate demand across portfolios, offering volume visibility that encourages manufacturers to invest in automated finishing lines. Consistency mandates drive custom Pantone colors and logo weaves, protecting margins for mills able to comply. Sustainability clauses now appear in every master supply agreement, pushing chains to pre-qualify vendors with Life-Cycle Assessments. Stable demand from this segment provides a buffer when residential orders soften.

Volatile Cotton Prices Squeezing SME Margins

The National Cotton Council signals that 2025 grower costs outstrip market prices, exposing mills to margin whipsaws. Southern European workshops relying on Egyptian Extra-Long-Staple quotes between USD 4,000-9,000 per ton face monthly price swings that erode profitability. Limited hedging instruments leave SMEs vulnerable compared with vertically integrated conglomerates that lock in futures contracts. Currency volatility post-Brexit compounds exposure, forcing some firms to shorten order books and raise deposit requirements from buyers. The knock-on effect limits their ability to stock innovative yarns, slowing diversification away from commodity cotton.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Recycled-Fiber Capacity Lowering Premium Price Points

- Corporate ESG Procurement Mandates Favoring Sustainably Certified Suppliers

- Post-Pandemic Hospitality Bankruptcy Overhang Dampening Commercial Orders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bed linen accounted for 38.20% of the European home textile market share in 2025, underscoring its status as the most frequently replaced category across households and hotels. The category benefits from smart-textile upgrades such as phase-change coatings, lifting average unit prices even as volumes remain steady. Bath linen, projected to post a 5.22% CAGR through 2031, outpaces all other segments as spa-inspired bathrooms become renovation focal points. Kitchen textiles hold stable demand on the back of pandemic-era cooking enthusiasm, while upholstery purchases mirror seven-year furniture cycles. Carpets preserve relevance in premium residential and acoustic sensitive hospitality spaces despite the rise of hard flooring.

Consumers increasingly bundle bedding and bath sets during promotional campaigns, a tactic that raises basket values for omnichannel retailers. Smart bed linen capable of regulating temperature attracts wellness-oriented buyers willing to pay double-digit premiums. The forthcoming Digital Product Passport will allow shoppers to verify fiber origin and chemical compliance at the point of sale, bolstering trust. Bath linen also rides the sustainability wave as brands introduce hemp-cotton blends with natural antimicrobial traits. These dynamics collectively reinforce the European home textile market's resilience against discretionary-spend volatility.

Cotton retained a 52.65% share of the European home textile market in 2025, buoyed by entrenched processing ecosystems and consumer comfort familiarity. Flax-derived linen, growing at a 4.63% CAGR, reflects record 185,849-hectare European cultivation that secures local supply lines. Recycled polyester gains traction in commercial linens where durability trumps natural aesthetics, supported by PET-to-fiber capacity expansions. Niche materials such as bamboo and hemp carve out premium micro-segments, leveraging biodegradability claims. Wool and silk remain anchored in luxury categories where tactile experience commands margin multiples.

REACH compliance drives mills to eliminate restricted substances from cotton finishing, increasing cost and opening doors for alternatives requiring fewer chemicals. Linen's antibacterial properties and lower water footprint align with corporate procurement scorecards, escalating its penetration in hotel bedding programs. Recycled synthetics address circular-economy mandates, especially when combined with take-back schemes that close the materials loop. As fiber portfolios diversify, retailers position multi-material bundles targeting specific consumer priorities, further entrenching variety within the Europe home textile market.

The Europe Home Textile Market Report is Segmented by Application (Bed Linen, Bath Linen, Kitchen Linen, and More), Material (Cotton, Linen, Synthetic Fibres, and More), End-User (Residential, Commercial), Distribution Channel (B2C/Retail Channels, B2B/Direct), and Geography (UK, Germany, France, Spain, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- IKEA Group

- H&M Home

- JYSK

- Dunelm Group plc

- John Lewis plc

- Associated Weavers Europe

- Zorlu Textiles (TAC)

- Mistral Home NV

- Eurofirany

- Aquinos Home

- Tisca Austria

- Textil Antilo

- Manterol Casa

- WestPoint Home

- Springs Global

- Victorial Classics

- Ralph Lauren Home

- Hermes Maison

- Sodra Textiles

- Laura Ashley

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - Europe Home Textile Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 EU-wide renovation wave boosting replacement demand

- 5.2.2 Growing footprint of budget hotel chains spurring linen refresh cycles

- 5.2.3 Rising e-commerce decor influencers accelerating trend turnover

- 5.2.4 Expansion of recycled-fiber capacity lowering premium price points

- 5.2.5 Smart-textile integrations (temperature regulation) opening new price tiers

- 5.2.6 Corporate ESG procurement mandates favouring sustainably-certified suppliers

- 5.3 Market Restraints

- 5.3.1 Volatile cotton prices squeezing SME margins

- 5.3.2 Skill shortages in European cut-and-sew facilities

- 5.3.3 Post-pandemic hospitality bankruptcy overhang dampening commercial orders

- 5.3.4 Cross-border e-commerce returns driving up logistics costs

- 5.4 Industry Value Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat of New Entrants

- 5.5.2 Bargaining Power of Suppliers

- 5.5.3 Bargaining Power of Buyers

- 5.5.4 Threat of Substitutes

- 5.5.5 Competitive Rivalry

- 5.6 Insights into the Latest Trends and Innovations in the Market

- 5.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

6 Market Size & Growth Forecasts (Value in USD)

- 6.1 By Application

- 6.1.1 Bed Linen

- 6.1.2 Bath Linen

- 6.1.3 Kitchen Linen

- 6.1.4 Upholstery

- 6.1.5 Carpets & Area Rugs

- 6.2 By Material

- 6.2.1 Cotton

- 6.2.2 Linen

- 6.2.3 Synthetic Fibres

- 6.2.4 Other Materials (Wool, Hemp, Silk, Jute, Bamboo)

- 6.3 By End-User

- 6.3.1 Residential

- 6.3.2 Commercial

- 6.4 By Distribution Channel

- 6.4.1 B2C/Retail Channels

- 6.4.1.1 Mass Merchandisers (Hypermarkets/Supermarkets)

- 6.4.1.2 Home Centers

- 6.4.1.3 Specialty Stores

- 6.4.1.4 Local Mom and Pop Stores

- 6.4.1.5 Online

- 6.4.1.6 Other Distribution Channels

- 6.4.2 B2B/Direct from the Manufacturers

- 6.4.1 B2C/Retail Channels

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 Germany

- 6.5.3 France

- 6.5.4 Spain

- 6.5.5 Italy

- 6.5.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 6.5.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 6.5.8 Rest of Europe

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 IKEA Group

- 7.4.2 H&M Home

- 7.4.3 JYSK

- 7.4.4 Dunelm Group plc

- 7.4.5 John Lewis plc

- 7.4.6 Associated Weavers Europe

- 7.4.7 Zorlu Textiles (TAC)

- 7.4.8 Mistral Home NV

- 7.4.9 Eurofirany

- 7.4.10 Aquinos Home

- 7.4.11 Tisca Austria

- 7.4.12 Textil Antilo

- 7.4.13 Manterol Casa

- 7.4.14 WestPoint Home

- 7.4.15 Springs Global

- 7.4.16 Victorial Classics

- 7.4.17 Ralph Lauren Home

- 7.4.18 Hermes Maison

- 7.4.19 Sodra Textiles

- 7.4.20 Laura Ashley

8 Market Opportunities & Future Outlook

- 8.1 Circular Economy Boosting Recyclable Textile Designs

- 8.2 Luxury Linen Growth through Hospitality Contracts