PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910883

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910883

Self Leveling Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

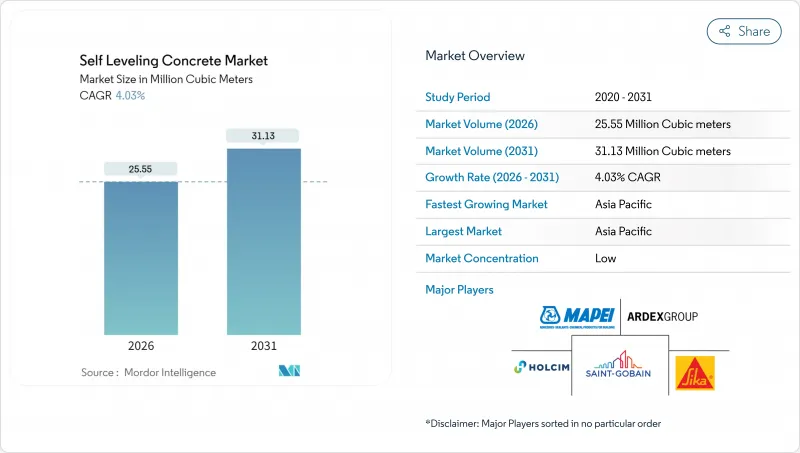

Self Leveling Concrete market size in 2026 is estimated at 25.55 Million Cubic meters, growing from 2025 value of 24.56 Million Cubic meters with 2031 projections showing 31.13 Million Cubic meters, growing at 4.03% CAGR over 2026-2031.

This steady trajectory reflects sustained renovation activity, the adoption of low-carbon binders, and rising demand for rapid-install flooring solutions. Strong uptake in e-commerce fulfillment centers, ongoing public-building refurbishment, and government incentives that reward VOC-free products continue to widen the user base. Contractors also view pump-truck delivery systems as a route to reduce labor requirements and maintain consistency on large pours, further propelling volume growth. At the same time, price volatility in specialty cement, a widening installation skill gap, and moisture-related callbacks temper near-term gains, underscoring the importance of training and cost-management initiatives.

Global Self Leveling Concrete Market Trends and Insights

Rapid Rebound of Commercial Renovation Projects Post-Pandemic

Commercial building owners have prioritized interior upgrades over ground-up construction since 2024, bolstered by asset-repositioning strategies in data centers, healthcare, and education. The Associated General Contractors survey shows 42% of firms anticipate more data-center work in 2025, with healthcare and education following close behind. These projects typically involve highly variable existing substrates, making self-leveling underlayments the product of choice to speed installation and meet tight re-occupancy deadlines. Adaptive-reuse conversions of legacy office towers further expand demand because substrate irregularities hinder the installation of modular carpet tiles and resilient floor coverings. U.S. federal infrastructure funding accelerates public-building refurbishment, and self-leveling compounds help agencies meet aggressive construction timetables while preserving existing structures.

Integration of Self-Drying, Low-Carbon CSA Binders

Calcium sulfoaluminate binders cut embodied-carbon emissions by up to 40% versus ordinary Portland cement and unlock same-day flooring readiness, attributes that resonate with owners pursuing LEED v4.1 points and net-zero goals. Contractors benefit from shorter project schedules, fewer dehumidification costs, and reduced moisture-testing risk. BASF and Sika have begun pairing CSA technology with advanced polymer hardeners to improve flexural strength and abrasion resistance, illustrating a collaborative approach to performance and sustainability. California's Buy Clean program has already positioned CSA-based self-levelers as a preferred specification in public work, and similar procurement rules are under review in British Columbia and the European Union.

Volatility in Specialty Cement and Admixture Prices

Carbon-pricing schemes added USD 18/tons to European clinker costs in 2024, pushing specialty cement prices up by nearly 11% year-on-year. Polymer-based flow modifiers and lithium carbonate also experienced abrupt shortages following weather-related mine closures, exposing contractors to bid risk on fixed-price jobs. Multinationals have responded by regionalizing admixture production to shorten lead times, but smaller formulators remain reliant on imported ingredients, making cost pass-through unavoidable. Owners have begun to implement steel-like escalation clauses in concrete contracts, yet not all public entities accept such provisions, creating a funding mismatch that can delay project starts.

Other drivers and restraints analyzed in the detailed report include:

- Fast-Track Flooring Schedules in E-Commerce Fulfillment Centers

- Adoption of Pump-Truck High-Volume SLU Systems on Megaprojects

- Installation Skill-Gap Causing Performance Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Underlayments held 64.58% self-leveling concrete market share in 2025, thanks to their role as the default solution for leveling out-of-tolerance substrates across virtually every building type. Bulk producers have optimized mix designs to balance flow, set time, and cost, drawing the category closer to commodity status. However, recurring training deficits frequently show up here, since crews may underestimate the importance of bonding primers and controlled water addition, leading to callbacks that dent contractor profitability.

Toppings, though smaller in absolute volume, are moving quickly toward mass adoption, projected to expand at a 4.34% CAGR over 2026-2031. Polished toppings now appear in retail chains, boutique hotels, and corporate amenity spaces, offering terrazzo-like aesthetics without the cost and installation complexity of traditional seeded systems. Innovations such as digital print-ready surfaces, translucent pigmented overlays, and hybrid PU-cement wear layers foster design flexibility. With owners hunting for unique finishes that still respect lean budgets, suppliers that can deliver creative, high-performance toppings at scale gain a clear advantage.

The Self Leveling Concrete Report is Segmented by Product (Topping and Underlayment), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Cubic Meters).

Geography Analysis

Asia-Pacific accounted for 38.34% of 2025 volume, supported by China's Belt and Road projects, India's Smart Cities Mission, and Southeast Asia's factory-expansion wave. Regional volume is projected to increase at a 4.14% CAGR through 2031 as governments channel spending into mass transit, airport, and data center programs. China alone is pouring more than USD 394 billion into provincial infrastructure in 2025, with self-leveling products specified for concourse overlays and terminal expansions. Holcim's SMARTFlow simulation program has found receptive audiences in Singapore and South Korea, where contractors value predictive pumpability models for high-rise construction.

North America remains a heavyweight, albeit with slower growth. Federal funding from the Infrastructure Investment and Jobs Act elevates demand in government buildings, bridges, and public-transit hubs, but private commercial starts are dampened by office-sector uncertainty. Interest-rate cuts expected in late 2025 should unlock some deferred projects, particularly in life-science research and campuses and advanced manufacturing.

Europe shows divergent trends. Western markets pursue sustainability leadership; Germany and France employ carbon-reduced CSA products on public procurement lists, while Spain and Italy refurbish aging hotels ahead of 2030 tourism goals. Eastern Europe continues to rely on EU cohesion funds, channeling grants into roadway and rail upgrades that include self-leveling bridge-deck overlays.

- ARDEX Group

- Arkema

- BASF

- Cemex S.A.B DE C.V.

- Duraamen Engineered Products, Inc.

- Flowcrete

- H.B. Fuller Company

- HOLCIM

- LATICRETE International, Inc.

- MAPEI S.p.A.

- Maxxon, Inc.

- PurEpoxy

- Saint-Gobain

- Sika AG

- Target Products Ltd

- TCC Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rebound of commercial renovation projects post-pandemic

- 4.2.2 Integration of self-drying, low-carbon CSA binders

- 4.2.3 Fast-track flooring schedules in e-commerce fulfillment centers

- 4.2.4 Adoption of pump-truck high-volume SLU systems on megaprojects

- 4.2.5 Government incentives for VOC-free indoor products

- 4.3 Market Restraints

- 4.3.1 Volatility in specialty cement and admixture prices

- 4.3.2 Installation skill-gap causing performance failures

- 4.3.3 Moisture-related callbacks in fast-track slabs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product

- 5.1.1 Topping

- 5.1.2 Underlayment

- 5.2 By End Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 South Korea

- 5.3.1.4 Japan

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 France

- 5.3.3.2 Germany

- 5.3.3.3 Italy

- 5.3.3.4 Russia

- 5.3.3.5 Spain

- 5.3.3.6 United Kingdom

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 ARDEX Group

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Cemex S.A.B DE C.V.

- 6.4.5 Duraamen Engineered

Products, Inc.

- 6.4.6 Flowcrete

- 6.4.7 H.B. Fuller Company

- 6.4.8 HOLCIM

- 6.4.9 LATICRETE International, Inc.

- 6.4.10 MAPEI S.p.A.

- 6.4.11 Maxxon, Inc.

- 6.4.12 PurEpoxy

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 Target Products Ltd

- 6.4.16 TCC Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment