PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910916

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910916

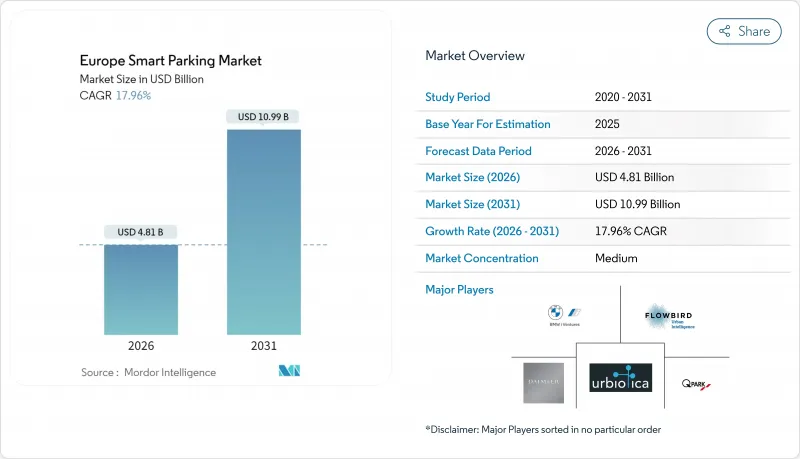

Europe Smart Parking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe smart parking market is expected to grow from USD 4.08 billion in 2025 to USD 4.81 billion in 2026 and is forecast to reach USD 10.99 billion by 2031 at 17.96% CAGR over 2026-2031.

Mandates on real-time parking data, rapid EV adoption, and corporate Scope 3 reporting requirements combine to accelerate investment in intelligent parking systems across the region. Municipal demand concentrates on scalable cloud platforms that dovetail with existing ITS architecture, while corporates look for space-saving solutions that feed sustainability dashboards. Consolidation among platform vendors is tightening competitive intensity, and integrated mobility ecosystems are starting to blur the lines between parking, charging, and ticketing services. Privacy-by-design obligations under GDPR add complexity, but they also push suppliers toward higher-value managed services and analytics.

Europe Smart Parking Market Trends and Insights

EV-Driven Parking Space Stress

Electric vehicle mandates force cities to retrofit or repurpose large sections of parking stock. The Energy Performance of Buildings Directive requires one charger per 20 spaces by 2025 and one per 10 by 2027, pushing municipalities to adopt systems that dynamically switch bays between charging and conventional use. Operators such as APCOA, through its partnership with Clever in Denmark, are embedding charging hardware into existing facilities and layering the sites with real-time occupancy analytics. Dynamic allocation eases queuing, while tariff engines balance revenue with EV incentives. As charging infrastructure spreads, pressure grows on algorithms to reconcile grid capacity limits with peak-hour parking demand. German and Nordic cities treat these analytics-centric projects as cornerstone use cases for broader ITS deployments.

Rise of Mobile Payments and Parking Apps

Digital payment penetration has crossed 75% in major Dutch municipalities. Interoperable mobile wallets and in-vehicle apps slash enforcement costs, sharpen demand forecasts, and open the door to congestion-responsive pricing. BMW's operating system now settles parking fees in 12 European countries, resetting user expectations for one-click, car-native transactions. The United Kingdom's National Parking Platform records more than 500,000 monthly transactions across 10 councils even as funding uncertainties loom. Platform data feeds machine-learning models that predict turnover, letting operators pre-price inventory and reduce revenue leakage. Privacy safeguards mandated by GDPR have pushed vendors to implement tokenization and edge processing, increasing demand for outsourced compliance expertise.

Up-Front Sensor and Civil-Works Costs

Embedded sensors range from USD 250 to USD 500 per unit before trenching and resurfacing, placing a heavy load on tight municipal budgets. Pardubice in the Czech Republic laid 3,421 sensors, boosting annual parking revenue from CZK 23 million to almost CZK 40 million yet demonstrating the steep capex hurdle. Surface-mounted devices cut installation time but demand more maintenance; flush-mounted options last longer but disrupt streets during deployment [PARKING.NET]. Cities weigh durability against budget cycles, often phasing projects over several fiscal years, slowing the Europe smart parking market rollout.

Other drivers and restraints analyzed in the detailed report include:

- EU Smart-City Funding for MaaS Pilots

- Corporate Scope-3 Decarbonization Targets

- Fragmented Municipal Procurement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional operators controlled 41.02% of 2025 revenue, a lead built on long-term concessions and large garage portfolios. This base underpinned the Europe smart parking market size for the segment, though peer-to-peer platforms are eating into growth with a 19.79% CAGR through 2031. EasyPark's link-up with ParkBee opened 120 Belgian garages to app-based rentals without adding physical assets. Operators counter by white-labeling their inventory to platforms and layering dynamic tariffs that raise yield per bay. Management companies sit between asset owners and tech vendors, bundling maintenance and data-analytics SLAs that municipalities increasingly outsource.

Despite slower growth, operators leverage balance-sheet capacity to fund sensor retrofits and EV charger installations, sustaining their hold over the Europe smart parking market share. Acquisition pipelines, exemplified by INDIGO's purchase of APCOA Belgium, convert regional strongholds into multicountry platforms able to negotiate SDK integrations directly with automotive OEMs. Peer-to-peer challengers differentiate through predictive pricing models that unlock driveways and underused corporate lots, but they rely on municipal approval for curbside blending, which can be politically fraught in dense city cores.

Cloud platforms accounted for 44.92% revenue in 2025 thanks to one-to-many scalability, cementing software's rank within the Europe smart parking market. However, services are forecast to outpace all other categories at a 20.36% CAGR as cities outsource GDPR compliance, maintenance, and AI model tuning. JustPark's Insights-Reach-Optimize suite blends reporting dashboards with tariff algorithms, demonstrating the pivot from one-off licenses toward recurring managed services.

Hardware providers confront margin pressure because municipalities can defer full-sensor coverage by adopting hybrid schemes that mix overhead cameras and crowd-sourced occupancy data. Cleverciti's mast-mounted radar units cover up to 100 spaces and cut per-space capex, easing sales into mid-tier cities. As software shifts to SaaS, the Europe smart parking market size for services is expected to converge with software revenue by the decade's end.

The Europe Smart Parking Market Report is Segmented by Type (Parking Operators, Parking Management Companies, Infrastructure Providers, and More), Solution (Hardware, Software, and Services), Technology (In-Ground Sensors, Camera/ANPR, Iot Platforms, Mobile Apps, and EV-Charging Integration), End-User (Municipalities, Commercial Car-Parks, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APCOA Parking Holdings GmbH

- EasyPark Group AB (Arrive Mobility)

- Indigo Group S.A.

- Q-Park NV

- Flowbird SASU (Parkeon SA)

- Parkopedia Ltd.

- Urbiotica SL

- Cleverciti Systems GmbH

- JustPark Parking Ltd.

- Parclick S.L.

- ParkBee B.V.

- RingGo Ltd.

- Telpark (Empark Aparcamientos y Servicios S.A.)

- Parklio d.o.o.

- ParkHub Inc.

- FlashParking, Inc.

- ParkAir Systems AB

- Daimler Mobility

- Parklio d.o.o.

- Park+ Mobility B.V.

- Bosch Service Solutions SE (Parking-as-a-Service)

- BMW i Ventures (ParkNow heritage assets)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV-driven parking space stress

- 4.2.2 Rise of mobile payments and parking apps

- 4.2.3 EU Smart-City funding for MaaS pilots

- 4.2.4 EU data-sharing mandates (ITS-Directive rev.)

- 4.2.5 Corporate scope-3 decarbonisation targets

- 4.2.6 15-Minute-City zoning accelerating curb reforms

- 4.3 Market Restraints

- 4.3.1 Up-front sensor and civil-works costs

- 4.3.2 Fragmented municipal procurement cycles

- 4.3.3 GDPR-driven restrictions on ANPR analytics

- 4.3.4 EV-first kerb allocation shrinking paid bays

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Ecosystem Analysis

- 4.8 Case Studies - Flagship European Deployments

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Parking Operators

- 5.1.2 Parking Management Companies

- 5.1.3 Infrastructure Providers (HW and SW)

- 5.1.4 Peer-to-Peer (P2P) Parking Platforms

- 5.1.5 Aggregators / Marketplaces

- 5.2 By Solution

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Technology

- 5.3.1 In-ground / Ultrasonic Sensors

- 5.3.2 Camera / Computer-Vision and ANPR

- 5.3.3 IoT Connectivity Platforms

- 5.3.4 Mobile Apps and Digital Payments

- 5.3.5 EV-Charging Integrated Parking

- 5.4 By End-User

- 5.4.1 Municipalities and Government

- 5.4.2 Commercial Car-Parks and Malls

- 5.4.3 Transport Hubs (Airports, Rail)

- 5.4.4 Corporate Campuses and Business Parks

- 5.4.5 Residential and Mixed-Use Developments

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Netherlands

- 5.5.7 Nordics

- 5.5.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 APCOA Parking Holdings GmbH

- 6.4.2 EasyPark Group AB (Arrive Mobility)

- 6.4.3 Indigo Group S.A.

- 6.4.4 Q-Park NV

- 6.4.5 Flowbird SASU (Parkeon SA)

- 6.4.6 Parkopedia Ltd.

- 6.4.7 Urbiotica SL

- 6.4.8 Cleverciti Systems GmbH

- 6.4.9 JustPark Parking Ltd.

- 6.4.10 Parclick S.L.

- 6.4.11 ParkBee B.V.

- 6.4.12 RingGo Ltd.

- 6.4.13 Telpark (Empark Aparcamientos y Servicios S.A.)

- 6.4.14 Parklio d.o.o.

- 6.4.15 ParkHub Inc.

- 6.4.16 FlashParking, Inc.

- 6.4.17 ParkAir Systems AB

- 6.4.18 Daimler Mobility

- 6.4.19 Parklio d.o.o.

- 6.4.20 Park+ Mobility B.V.

- 6.4.21 Bosch Service Solutions SE (Parking-as-a-Service)

- 6.4.22 BMW i Ventures (ParkNow heritage assets)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Opportunity Hotspots (2025-2030)

- 7.3 Strategic Roadmap for Stakeholders