PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910922

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910922

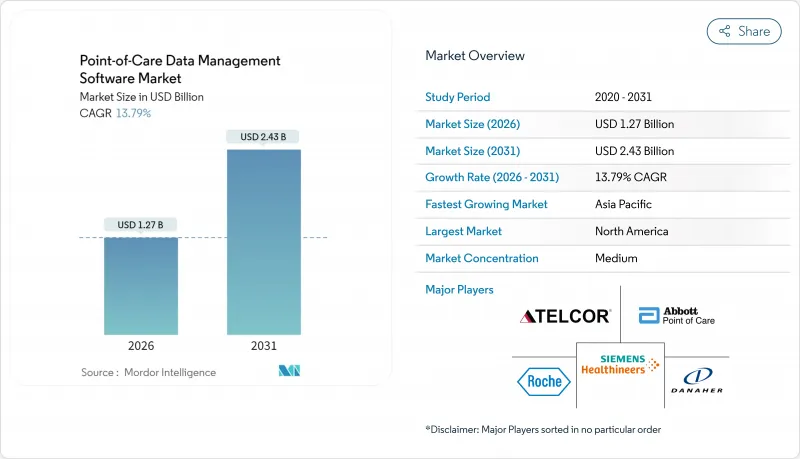

Point-of-Care Data Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The point-of-care data management software market is expected to grow from USD 1.12 billion in 2025 to USD 1.27 billion in 2026 and is forecast to reach USD 2.43 billion by 2031 at 13.79% CAGR over 2026-2031.

This brisk expansion springs from health systems' pivot toward real-time diagnostics, wider government funding for flexible connectivity, and a rising preference for outcome-based reimbursement. Cloud migration, AI-driven analytics, and middleware that links hundreds of device types are now central buying criteria. Vendors able to bundle software, services, and cybersecurity safeguards stand to capture share as hospitals standardize data workflows and home-care programs scale. Consolidation among large incumbents coexists with niche innovators, creating a moderate-concentration landscape poised for steady deal activity.

Global Point-of-Care Data Management Software Market Trends and Insights

Innovation in Flexible Connectivity and Interface Solutions

Health systems are demanding interoperable middleware that links more than 200 distinct point-of-care devices through standardized FHIR R4 APIs, a capability spurred by CMS's Interoperability and Patient Access Rule. Vendors now treat connectivity as core infrastructure, not add-on code, to avoid data silos and accelerate clinical decision-making. The arrival of 5G and edge-computing nodes cuts latency for cloud-native deployments, letting multi-site operators harmonize workflows across dispersed facilities. FDA's Digital Health Software Precertification Program further elevates connectivity by embedding it in regulatory review, creating an incentive for continuous performance monitoring. As a result, buyers prioritize middleware depth and future-proof interface roadmaps when awarding contracts.

Expansion of Healthcare Infrastructure Budgets

Governments spent USD 200 billion on health-infrastructure projects in 2024, earmarking sizable funds for digital platforms that include point-of-care data management software. Programs like India's National Digital Health Mission and China's Healthy China 2030 channel budget toward IT modernization, opening doors for vendors able to meet country-specific data-localization rules. Private-public partnerships often bundle software clauses into construction tenders, effectively converting optional tech into mandatory kit. As new hospitals and diagnostic centers go live, they specify analytics suites that feed value-based care dashboards, ensuring software procurement aligns with bricks-and-mortar schedules. This spends surge enlarges the addressable base in mid-income economies and smooths revenue visibility for suppliers through long-term maintenance deals.

High Deployment and Integration Costs

Comprehensive rollouts cost USD 500,000-USD 2 million per facility, a hurdle that stalls adoption in smaller or rural hospitals where 40% of IT posts sit vacant. Legacy-system heterogeneity inflates interface coding and workflow redesign, often stretching timelines past budget cycles. Total cost of ownership widens when annual maintenance, staff training, and upgrade subscriptions enter the calculus. For facilities with thin patient volumes, payback models remain weak, nudging them toward grant funding or SaaS options with phased billing. Vendors able to package modular, cloud-hosted offerings at lower entry prices can unlock pent-up demand and counter this drag on CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Government Funding Initiatives for POC Testing

- Data Privacy and Cybersecurity Threats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployments still commanded 51.62% revenue in 2025, showing the historical sway of in-house servers for direct data custody. Yet cloud solutions are sprinting at a 15.88% CAGR, fuelled by robust disaster-recovery, auto-patching, and elastic storage benefits. A hybrid approach acts as a transition bridge: many systems keep latency-sensitive modules on-site while pushing analytics to HIPAA-compliant clouds. Multi-site chains prize cloud-centric dashboards that synchronize performance metrics across campuses, trimming duplicated infrastructure. FDA's recent guidance equating validated cloud configurations with local installations further eases CIO concerns, nudging purchase orders toward SaaS models. Savings from hardware refresh deferral often finance cybersecurity upgrades, accelerating the migration curve.

Cloud vendors tout FedRAMP and HITRUST credentials to win federal and academic accounts, denting the head-start enjoyed by legacy on-premises incumbents. Rising ransomware threats also make off-site backups imperative, a default feature in many cloud contracts. Conversely, research institutes handling genomic data still lean on local clusters to maximize compute throughput. Even here, containerized workloads permit burst capacity in the cloud during peak demand, showcasing a future where line-blurring hybrid architectures dominate. Over time, service-based pricing shifts vendor focus from perpetual licenses to retention-driven roadmaps rich in AI modules and API marketplaces that monetize ecosystem participation.

Hospitals and critical-care units retained the lion's 46.15% share in 2025, supported by emergency-department throughput targets and lab turnaround mandates. Nevertheless, home-health programs are clocking a 14.71% CAGR, buoyed by Medicare's Hospital-at-Home expansion and aging-population dynamics. Portable analyzers and telehealth kits feed a need for lightweight, browser-based dashboards that caregiver's access from patient residences. Diagnostic centers integrate auto-verification rules to handle ballooning specimen loads while clinics lean on point-of-care data to shorten visit cycles under capitated payment plans.

Home-care operators grapple with variable broadband quality, propelling interest in store-and-forward architecture that syncs when connectivity resumes. Hospitals continue to invest in enterprise-wide middleware that flags quality-control drifts and consolidates reagent inventory data, improving supply chain efficiency. Outpatient clinics adopt shared-service models, licensing centralized analytics but maintaining autonomy over local device pools. The growing "other" category spanning long-term care and occupational-health sites creates opportunities for modular UI skins tailored to non-hospital workflows, widening addressable revenue.

The Point-Of-Care Data Management Software Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), End User (Hospitals/Critical Care Units, Diagnostic Centers, Clinics/Outpatient, Home Healthcare, and More), Application (Infectious Disease Devices, Glucose Monitoring, and More), Component (Software Platform, and Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained a 38.21% share in 2025, anchored by NIH grants, BARDA's DRIVe program, and mature EHR penetration. U.S. hospitals deploy analytics to satisfy Medicare Advantage quality metrics, whereas Canada's provincial systems fund rural-access upgrades that hinge on middleware interoperability. Venture capital flows and predictable FDA pathways make the region a test bed for AI-rich modules, giving suppliers early feedback loops.

Asia Pacific is set to compound at 16.52% CAGR, the fastest worldwide. China's USD 15 billion health-digitization budget funnels into county-level hospitals eager for cloud-hosted dashboards. India's Ayushman Bharat Digital Mission enforces interoperability, nudging buyers toward standards-compliant software. Japan leverages Society 5.0 to back aging-care pilots that marry home-monitoring kits with centralized analytics. Singapore acts as the regional deployment hub, exporting expertise across Southeast Asia. The mosaic of regulations rewards platforms sporting flexible data-sovereignty toggles and multilingual interfaces.

Europe exhibits steady, regulation-driven uptake. Germany's Digital Healthcare Act finances hospital IT overhauls, while the United Kingdom's NHS Digital campaign pushes all acute trusts onto a shared interoperability standard. France and Spain tap EU Recovery funds for telemedicine and lab IT modernization. Strict GDPR rules require baked-in consent management and encryption, extending deployment cycles but enhancing trust. Suppliers that pre-validate compliance templates gain bidding advantages. South America, the Middle East, and Africa trail in share but post mid-teens growth as public-private buildouts stipulates digital kits from the outset.

- Siemens Healthineers AG (Conworx)

- Abbott Point of Care Inc. (Alere Inc.)

- Danaher Corporation (HemoCue AB and Radiometer Medical ApS)

- F. Hoffmann-La Roche Ltd

- TELCOR Inc.

- Orchard Software Corporation

- Randox Laboratories Ltd

- Thermo Fisher Scientific Inc.

- EKF Diagnostics Holdings plc

- HORIBA Ltd

- Nova Biomedical Corporation

- Sysmex Corporation

- Werfen S.A.

- Alcor Scientific Inc.

- PTS Diagnostics LLC

- Masimo Corporation

- Becton, Dickinson and Company

- Beckman Coulter Inc.

- Medtronic plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Innovation in Flexible Connectivity and Interface Solutions

- 4.2.2 Expansion of Healthcare Infrastructure Budgets

- 4.2.3 Government Funding Initiatives for POC Testing

- 4.2.4 Payor Shift Toward Outcome-Based Reimbursement

- 4.2.5 AI-Driven Analytics Modules for Antimicrobial Stewardship

- 4.2.6 Growing Cybersecurity Compliance Requirements

- 4.3 Market Restraints

- 4.3.1 High Deployment and Integration Costs

- 4.3.2 Data Privacy and Cybersecurity Threats

- 4.3.3 Fragmented Legacy Device Firmware Ecosystem

- 4.3.4 Shortage of Skilled IT Staff in Rural Facilities

- 4.4 Impact of Macroeconomic Factors

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By End User

- 5.2.1 Hospitals / Critical Care Units

- 5.2.2 Diagnostic Centers

- 5.2.3 Clinics / Outpatient

- 5.2.4 Home Healthcare

- 5.2.5 Other End Users

- 5.3 By Application

- 5.3.1 Infectious Disease Devices

- 5.3.2 Glucose Monitoring

- 5.3.3 Coagulation Monitoring

- 5.3.4 Urinalysis

- 5.3.5 Cardiometabolic Monitoring

- 5.3.6 Cancer Markers

- 5.3.7 Hematology

- 5.3.8 Other POC Applications

- 5.4 By Component

- 5.4.1 Software Platform

- 5.4.2 Middleware

- 5.4.3 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Siemens Healthineers AG (Conworx)

- 6.4.2 Abbott Point of Care Inc. (Alere Inc.)

- 6.4.3 Danaher Corporation (HemoCue AB and Radiometer Medical ApS)

- 6.4.4 F. Hoffmann-La Roche Ltd

- 6.4.5 TELCOR Inc.

- 6.4.6 Orchard Software Corporation

- 6.4.7 Randox Laboratories Ltd

- 6.4.8 Thermo Fisher Scientific Inc.

- 6.4.9 EKF Diagnostics Holdings plc

- 6.4.10 HORIBA Ltd

- 6.4.11 Nova Biomedical Corporation

- 6.4.12 Sysmex Corporation

- 6.4.13 Werfen S.A.

- 6.4.14 Alcor Scientific Inc.

- 6.4.15 PTS Diagnostics LLC

- 6.4.16 Masimo Corporation

- 6.4.17 Becton, Dickinson and Company

- 6.4.18 Beckman Coulter Inc.

- 6.4.19 Medtronic plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment