PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910932

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910932

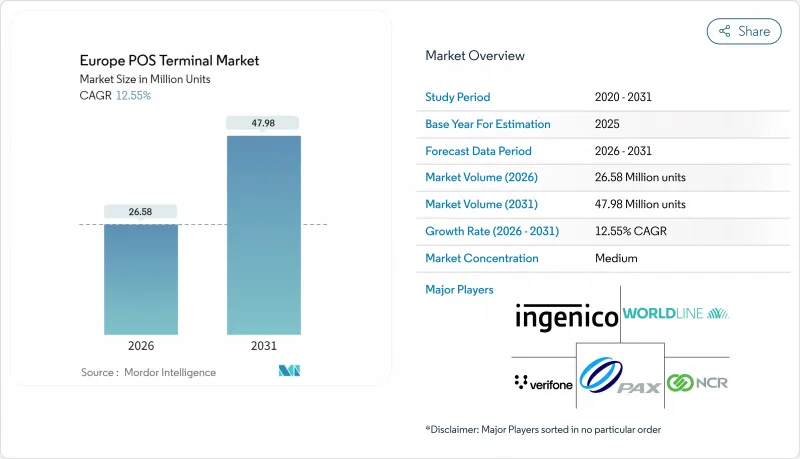

Europe POS Terminal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe POS terminal market was valued at USD 23.62 million units in 2025 and estimated to grow from USD 26.58 million units in 2026 to reach USD 47.98 million units by 2031, at a CAGR of 12.55% during the forecast period (2026-2031).

The expansion has been underpinned by accelerated contactless adoption, regulatory mandates that force periodic hardware refresh, and merchants' search for unified payment infrastructure that lowers total cost of ownership. Strong consumer preference for tap-to-pay, transit system digitization, and subsidy-backed roll-outs in smaller cities have collectively pushed shipment volumes higher in Western and Central Europe. Vendors that combine Android-based terminals, cloud analytics, and subscription billing have captured wallet share as merchants prioritize ROI. Meanwhile, SoftPOS introductions have broadened the addressable base by turning smartphones into certified acceptance points, challenging legacy fixed units but also enlarging overall payment acceptance capacity.

Europe POS Terminal Market Trends and Insights

PIDF subsidies accelerating Tier-3-Tier-6 roll-outs

Payment Infrastructure Development Fund programs lowered merchant on-boarding cost and spurred shipments into previously under-served rural districts. Worldline alone enrolled 6,300 micro-merchants on its Tap on Mobile platform during H1 2024, signaling how subsidy alignment quickly converts latent demand into active transaction volumes. The subsidy window created a new recurring revenue stream as newly digitized merchants required value-added services such as analytics and inventory modules.

Surging credit-card base lifts card-swipe volumes

The European card base surpassed 100 million active cards in 2024, feeding higher card-present volumes and reinforcing merchant economics for upgrading POS estates. Higher swipe density improved acquirer margins, encouraged loyalty-program integration, and strengthened the business case for contactless limits expansion.

Zero-MDR UPI erodes small-merchant economics

When regulators capped merchant discount at zero for instant payments, micro-merchants pivoted toward fee-free QR alternatives, slashing hardware rentals. Acquirers saw service fee compression, and POS suppliers lost first-unit sales in the cafe and kiosk segment. Larger chains, however, continued to rely on card rails because of richer data capture and chargeback management, tempering the downside.

Other drivers and restraints analyzed in the detailed report include:

- Omni-payment Android POS integration

- GST e-invoice compliance driving real-time POS upgrades

- QR-code ubiquity dampens new POS demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless units delivered 12.65% CAGR through 2031 even though contact-based devices held a 53.90% Europe POS terminal market share in 2025. The higher limit for tap-to-pay without PIN in the EEA trimmed checkout friction, and transit systems such as Brussels STIB recorded 57% contactless adoption for single rides in 2024. Europe POS terminal market size expansion within this segment was further propelled by wallet providers like Apple Pay and Google Pay adding loyalty receipt delivery, raising merchant acceptance incentives.

Legacy contact-based terminals remained indispensable for high-ticket transactions and markets with older banking cards. Nonetheless, multi-interface devices such as Verifone's P400 allowed merchants to replace dual hardware with one converged pinpad, moderating the cannibalization rate. As payment security upgrades migrate toward biometric user verification by 2028, contactless share is projected to edge past the 60% threshold, cementing its role as the principal growth engine of the Europe POS terminal market.

The Europe POS Terminal Market Report is Segmented by Mode of Payment Acceptance (Contact-Based, and Contactless), POS Type (Fixed Point-Of-Sale Systems, and Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More), and Country (Germany, United Kingdom, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (Units).

List of Companies Covered in this Report:

- Ingenico S.A.

- Worldline S.A.

- Verifone Systems, Inc.

- PAX Technology Limited

- NCR Corporation

- Diebold Nixdorf Incorporated

- Toshiba Corporation

- HP Inc.

- Castles Technology Co., Ltd.

- Adyen N.V.

- Stripe, Inc.

- SumUp Payments Limited

- Block, Inc. (Square)

- Fiserv, Inc. (Clover Network, LLC)

- Elavon, Inc.

- EVO Payments, Inc.

- Nexi S.p.A.

- myPOS Europe Ltd.

- Yavin SAS

- PayPal Holdings, Inc. (Zettle)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in contactless card penetration

- 4.2.2 Omnichannel retail demand for integrated POS

- 4.2.3 EU MPoC-certified SoftPOS roll-outs

- 4.2.4 Hybrid debit (girocard + scheme) upgrade cycle

- 4.2.5 EU Green Deal energy-efficient hardware push

- 4.2.6 Cashless-compliant unattended vending growth

- 4.3 Market Restraints

- 4.3.1 High TCO for SMEs and compliance costs

- 4.3.2 Fragmented fiscal/fiscalisation rules

- 4.3.3 Rural technician shortage extends downtime

- 4.3.4 Higher cyber-insurance premiums for legacy POS

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (UNITS)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-user Industries

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ingenico S.A.

- 6.4.2 Worldline S.A.

- 6.4.3 Verifone Systems, Inc.

- 6.4.4 PAX Technology Limited

- 6.4.5 NCR Corporation

- 6.4.6 Diebold Nixdorf Incorporated

- 6.4.7 Toshiba Corporation

- 6.4.8 HP Inc.

- 6.4.9 Castles Technology Co., Ltd.

- 6.4.10 Adyen N.V.

- 6.4.11 Stripe, Inc.

- 6.4.12 SumUp Payments Limited

- 6.4.13 Block, Inc. (Square)

- 6.4.14 Fiserv, Inc. (Clover Network, LLC)

- 6.4.15 Elavon, Inc.

- 6.4.16 EVO Payments, Inc.

- 6.4.17 Nexi S.p.A.

- 6.4.18 myPOS Europe Ltd.

- 6.4.19 Yavin SAS

- 6.4.20 PayPal Holdings, Inc. (Zettle)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment