PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911466

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911466

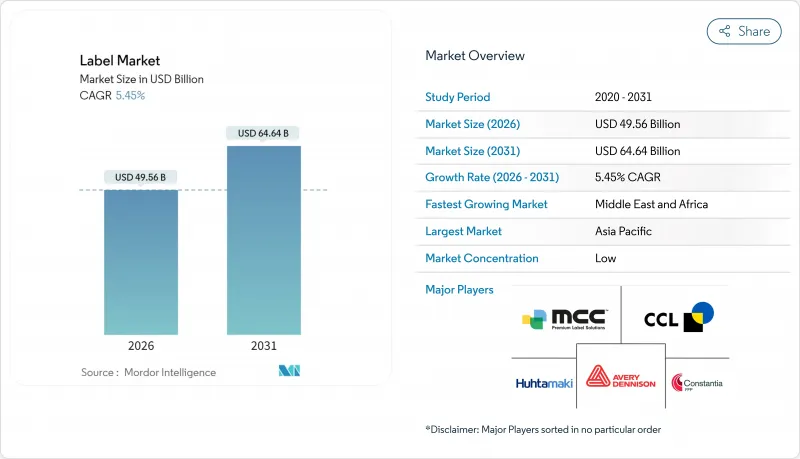

Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Global label market was valued at USD 47 billion in 2025 and estimated to grow from USD 49.56 billion in 2026 to reach USD 64.64 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031).

This steady trajectory reflects the sector's capacity to adjust to e-commerce expansion, sustainability regulations, and smart packaging adoption. Regulatory pressure for recyclable materials continues to push converters toward liner-less constructions and bio-based films, while retailers' demand for real-time product authentication accelerates the shift toward connected packaging. Digital printing's economics favor short runs and customization, raising margins despite its modest share of total output. Competitive momentum favors firms that can integrate RFID, NFC, and QR solutions at scale, turning labels into data touchpoints that enhance supply-chain visibility and consumer engagement. The convergence of these forces positions the label market for durable growth even as direct-to-container printing presents a substitution threat in specific beverage categories.

Global Label Market Trends and Insights

E-commerce Boom Driving Variable-Data Shipping Labels

Worldwide parcel volume reached 21.7 billion in 2023 and is tracking toward 29 billion by 2029, pushing converters to supply labels capable of real-time, order-specific data. Dimensional-weight billing and omnichannel fulfillment require scannable graphics that survive automated sortation. Amazon's 15.7% volume surge in 2023 underscores the scale of demand for durable thermal and pressure-sensitive constructions. Logistics providers prefer adhesives that remain tacky across diverse corrugated substrates, while brand owners seek layouts that accommodate late-stage customization. As a result, converters investing in high-speed digital presses capture the premium associated with quick-change print jobs, reinforcing e-commerce as a structural growth engine for the label market.

Sustainability Regulations Accelerating Liner-Less and Recyclable Formats

The EU Packaging and Packaging Waste Regulation mandates 70% recyclability by weight by 2030, compelling redesign of face stocks, liners, and adhesives. CELAB-Europe targets recycling of 75% of spent liners by 2025, pushing collection schemes beyond voluntary pilots. Extended Producer Responsibility in U.S. states imposes fee differentials as high as 300% between compliant and non-compliant packaging, making sustainability a profit determinant. Converters responding with liner-less labels reduce waste by up to 40% and unlock logistics efficiencies. Material science advances, including bio-adhesives with 85% renewable content, ease the transition without sacrificing application speed, reinforcing the driver's long-term impact on label market growth.

Raw-Material Cost Volatility

Petrochemical supply disruptions from hurricanes in the U.S. Gulf Coast have tightened feedstock availability for acrylics and polyolefins, lifting adhesive prices and extending lead times. Europe's adhesives market, expected to reach EUR 22.2 billion by 2026, competes for the same inputs, squeezing smaller converters that lack purchasing leverage. To manage volatility, converters hold larger safety stocks, raising working-capital needs and pressuring earnings in the short term, thereby restraining label market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Food and Beverage Demand for Premium Compliance-Driven Packaging

- Smart/Connected Packaging Opening New Revenue Streams

- Shift Toward Stand-Up Pouches and Direct-to-Object Printing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure-sensitive formats held 32.75% of the label market share in 2025, thanks to their versatility across food, personal care, and logistics applications. Sleeve products, although smaller in absolute terms, are projected to expand at an 8.71% CAGR as brand owners pursue 360-degree graphics and tamper evidence. This sleeve uptake lifts the label market size in premium beverages and nutraceuticals, while wrap-around formats encounter substitution risk from cap-print and embossing. Pressure-sensitive innovation continues with recyclable adhesives 35% lower carbon footprints help sustain share even as sustainability scrutiny intensifies. Consequently, a two-track pattern sets in: commodity beverages pivot to direct print, while premium SKUs adopt sophisticated sleeves, each path reinforcing differentiated value pools inside the global label market.

Flexography controlled 57.55% of the label market size in 2025 due to speed and cost advantages on runs above 50,000 linear meters. Digital inkjet and electrophotography, however, are pacing at 8.87% CAGR, securing 16.20% of revenue from just 4.10% of output. The economics hinge on software-driven job changeovers that slash downtime and enable SKU proliferation. Recent patents on composite black inks accelerate drying on porous substrates, boosting press throughput and lowering per-unit cost. .Analog stalwarts gravure, offset, and screen retain niches such as foil-on-foil spirits labels and high-speed canning, yet investment trends unambiguously favor digital. Over the outlook period, converters that master hybrid press workflows capture both commodity scale and premium customization, deepening their penetration of the expanding label market.

The Global Label Market Report is Segmented by Label Type (Pressure-Sensitive, Shrink and Stretch Sleeves, and More), Printing Technology (Flexography, Gravure, Offset, Digital, Screen and Other Analog), Material (Paper and Paperboard, PVC, and More), End-User Industry (Food and Beverages, Pharmaceutical and Healthcare, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 44.60% of label market share in 2025, fueled by China's scale and India's growth in packaged foods. Government incentives for advanced manufacturing and the clustering of press-builders lower capital costs, encouraging capacity additions. Thailand's and South Korea's shifts toward labelless bottles illustrate how some APAC regulators leapfrog legacy practices, thereby shaping the global conversation on sustainable labeling.

Middle East and Africa, though only 6.10% of 2025 revenue, will post a 5.24% CAGR through 2031, propelled by food-processing investments and retail modernization. Mega-projects in Saudi Arabia's NEOM and Egypt's industrial zones spur corrugated and label demand, while African e-commerce platforms fuel shipping-label growth. Limited liner recycling infrastructure, however, keeps liner-less solutions nascent, offering upside for suppliers exporting turnkey technologies into the region.

North America remains the technological bellwether, home to over 2,000 converters and a deep installed base of digital presses. RFID mandates at Walmart and the proliferation of direct-fulfillment warehouses intensify demand for smart labels. Europe, while mature, continues to set the regulatory pace on recyclability, driving adoption of wash-off adhesives and mono-material solutions. South America rebounds as macro conditions stabilize; Brazil's beverage giants adopt sleeves for flavored-water SKUs, widening product breadth. Collectively, cross-regional dynamics reinforce a balanced yet opportunity-rich landscape for the global label market.

- CCL Industries Inc.

- Avery Dennison Corporation

- Multi-Color Corporation

- Huhtamaki Oyj

- Constantia Flexibles GmbH

- UPM Raflatac (UPM Group)

- Mondi plc

- Fuji Seal International Inc.

- Fort Dearborn Company

- Lintec Corporation

- 3M Company

- Smurfit WestRock

- Amcor plc

- Taghleef Industries

- Stora Enso Oyj

- Xeikon BV

- KRIS Flexipacks Pvt Ltd

- Royal Sens Group

- Leading Edge Labels & Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom driving variable-data shipping labels

- 4.2.2 Sustainability regulations accelerating liner-less and recyclable formats

- 4.2.3 Food-and-beverage demand for premium compliance-driven packaging

- 4.2.4 Smart/connected packaging (QR, RFID) opening new revenue streams

- 4.2.5 EV battery-safety mandates spurring high-spec pressure-sensitive labels

- 4.2.6 ASEAN label-free bottle pilots catalyzing direct-to-container printing

- 4.3 Market Restraints

- 4.3.1 Raw-material cost volatility (films, adhesives)

- 4.3.2 Shift toward stand-up pouches and direct-to-object printing

- 4.3.3 Limited global liner-waste recycling infrastructure

- 4.3.4 Emerging label-free bottle regulations shrinking wrap-around demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Supply-Chain Analysis

- 4.9 Assessment of COVID-19 and Geopolitical Impacts

5 MARKET SIZE & GROWTH FORECASTS (VALUE, 2021-2030)

- 5.1 By Label Type

- 5.1.1 Pressure-Sensitive Labels

- 5.1.2 Shrink and Stretch Sleeves

- 5.1.3 In-Mold Labels

- 5.1.4 Wet-Glue Labels

- 5.1.5 Thermal-Transfer Labels

- 5.1.6 Wrap-Around Labels

- 5.2 By Printing Technology

- 5.2.1 Flexography

- 5.2.2 Gravure

- 5.2.3 Offset

- 5.2.4 Digital (Inkjet and Electrophotographic)

- 5.2.5 Screen and Other Analog

- 5.3 By Material

- 5.3.1 Paper and Paperboard

- 5.3.2 PVC

- 5.3.3 PET

- 5.3.4 PE and PP

- 5.3.5 Bio-based and Compostable Films

- 5.4 By End-User Industry

- 5.4.1 Food and Beverages

- 5.4.2 Pharmaceutical and Healthcare

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Retail and Logistics

- 5.4.5 Industrial and Automotive

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 UAE

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Saudi Arabia

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CCL Industries Inc.

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Multi-Color Corporation

- 6.4.4 Huhtamaki Oyj

- 6.4.5 Constantia Flexibles GmbH

- 6.4.6 UPM Raflatac (UPM Group)

- 6.4.7 Mondi plc

- 6.4.8 Fuji Seal International Inc.

- 6.4.9 Fort Dearborn Company

- 6.4.10 Lintec Corporation

- 6.4.11 3M Company

- 6.4.12 Smurfit WestRock

- 6.4.13 Amcor plc

- 6.4.14 Taghleef Industries

- 6.4.15 Stora Enso Oyj

- 6.4.16 Xeikon BV

- 6.4.17 KRIS Flexipacks Pvt Ltd

- 6.4.18 Royal Sens Group

- 6.4.19 Leading Edge Labels & Packaging

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space & Unmet-Need Assessment