PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911746

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911746

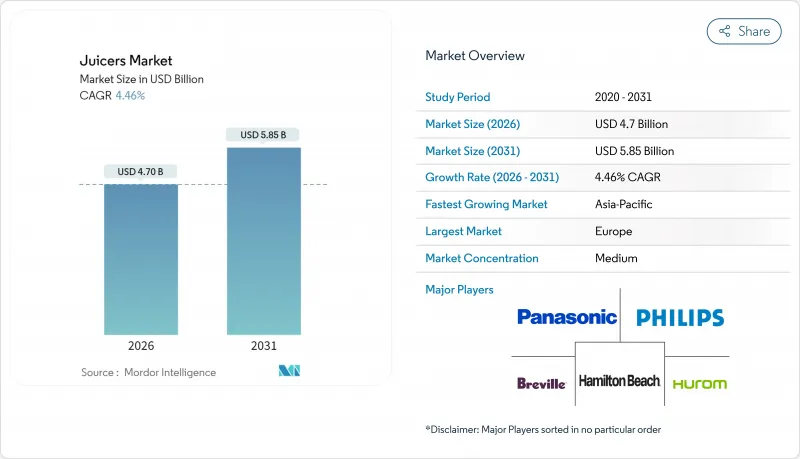

Juicers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The juicers market is expected to grow from USD 4.50 billion in 2025 to USD 4.70 billion in 2026 and is forecast to reach USD 5.85 billion by 2031 at 4.46% CAGR over 2026-2031.

This steady trajectory reflects a maturing replacement cycle in North America and Europe while capturing incremental volumes from first-time buyers in the Asia-Pacific. Heightened interest in preventive health, the popularity of juice detox regimens, and the spread of specialty juice bars are creating parallel demand streams across residential and commercial applications. Technology upgrades, especially low-noise motors, precision pulp ejection, and cold-press mechanisms, encourage premium trade-ups even in price-sensitive segments. Retail dynamics support growth as online channels accelerate discovery and direct-to-consumer engagement, yet brick-and-mortar specialists remain influential through live product demonstrations that shorten decision time for higher-ticket purchases. Manufacturers also benefit from favorable regulatory signals that emphasize nutrient-dense diets and food-waste reduction, which align with juicer capabilities and reinforce their value proposition. Together, these factors position the juicers market as a stable mid-single-digit grower rather than a fad-driven category.

Global Juicers Market Trends and Insights

Rising Health Consciousness & DIY Fresh-Juice Trend

Western dietary guidelines increasingly recommend whole-food nutrient density, steering consumers toward minimally processed beverage options. Parents view countertop juicers as tools for controlling sugar levels and maximizing vitamin intake, aligning with the USDA's 2025 advisory that caps daily packaged-juice servings for children. Peer-reviewed work shows cold-press extraction retains up to 60% more bioactive compounds than shelf-stable juices, strengthening the perceived health edge of home preparation. Social media amplifies success narratives around immunity, weight management, and detox cleanses, translating aspirational wellness goals into actual product demand. Brands counter previous perceptions of messy cleanup by introducing auto-rinse functions and dishwasher-safe parts, thereby lowering daily-use friction. The confluence of scientific validation and lifestyle marketing underpins a durable shift rather than a fad, keeping the juicers market on a predictable upswing. Expect health-centric positioning to deepen as population-aging accelerates in developed economies, intensifying focus on functional nutrition.

Expansion of Juice Bars & Food-Service Chains

Franchise-driven rollouts create standardized equipment tenders that favor suppliers with proven uptime and service networks. Nekter Juice Bar expanded to 199 outlets with USD 120 million in sales in 2024, highlighting the scalability of fresh-juice concepts. Restaurant association surveys indicate that 67% of the United States diners now expect functional beverages on menus, elevating fresh-pressed juice from a niche item to a core traffic driver . Equipment specifications focus on throughput of 200-300 servings per hour, motor durability, and NSF-certified sanitation design, drawing clear lines between commercial and residential models. Replacement cycles tighten to 3-5 years in high-volume sites, creating recurring sales independent of underlying consumer demand trends. As franchise density increases in Asia-Pacific, suppliers that package financing and preventive-maintenance contracts gain an inside track on chain-wide standardization. The knock-on effect is stronger brand visibility in consumer settings, which translates into higher awareness and credibility for the same brands at retail.

High Upfront Cost of Premium Appliances

In lower-income regions, a USD 300-600 cold-press juicer can equal multiple months of disposable household income, limiting first-time adoption. Even in mature markets, consumers weigh the amortization period against purchasing freshly pressed servings for USD 6-12 each. Brands employ tiered portfolios entry centrifugal at USD 70, mid-range masticating at USD 200, and premium twin-gear at USD 400+ to widen the funnel, yet price steps remain pronounced. Financing options such as zero-interest installments ease sticker shock but introduce credit-risk exposure for vendors. Currency fluctuations further complicate pricing strategies in import-dependent nations, occasionally triggering sudden retail hikes that stall momentum. Competitive pressure from lower-spec clones originating in China compresses margin headroom for innovation-focused brands. Until production scale or alternative materials drive meaningful cost reductions, price sensitivity will continue to clip demand in value-oriented segments.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Low-Noise, High-Yield Extraction Technology

- Cold-Press Subscription Services Boosting At-Home Adoption

- Substitution by Ready-to-Drink Packaged Juices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal models held 44.10 of % juicer market share in 2025, buoyed by attractive price points and fast operation suited for large-batch prep. However, masticating and triturating systems are forecast to widen their position at an 7.72% CAGR, reflecting nutrition-first purchasing criteria. The juicers market size associated with slow-juicing platforms is therefore expanding faster than the overall category, signalling a tilt toward quality over speed. Consumers respond to lab-verified claims of 60% higher vitamin C retention and reduced oxidation, features heavily spotlighted in point-of-sale messaging. At the same time, twin-gear variants target juice bars seeking maximum yield per kilogram of produce, where waste-reduction metrics influence profit margins. Product engineers now add self-cleaning auger housings and quick-release filter baskets to cut downtime, minimizing one of the historical disadvantages of slow-juicing formats. Competitive rivalry intensifies as mid-tier brands introduce hybrid machines that toggle between high-speed and slow-juicing modes to capture fence-sitters who want versatility.

End-user testimonials reinforce the appetite for premiumization, with many households upgrading after only three years of centrifugal use. Price elasticity remains favorable among health-dedicated demographics, and installment-plan availability has unlocked younger cohorts. Brand storytelling leverages third-party certifications, such as NSF food-safety approval for commercial deployment, to transcend purely cosmetic differentiation. Future iteration cycles look poised to merge slow-juicing mechanics with connected-device analytics, using motor load data to predict maintenance schedules and extend product life. Such investments underscore the shift from commoditized hardware to service-enabled appliances that create lifetime customer value well beyond the initial sale.

Electric configurations command 79.90% share within the juicers market size and continue to expand at 5.65% CAGR, propelled by successive generations of quieter, more energy-efficient motors. User research indicates that even occasional juicers prefer push-button simplicity over the challenging work required by manual presses. Manufacturers answer sustainability critiques by integrating eco-mode settings that drop idle wattage without slowing extraction speeds, easing energy-cost concerns in regulated markets. Mid-premium units now include whisper-quiet operation below 70 decibels, enabling late-night or early-morning use without household disturbance. Manual models cling to niches such as mobile food trucks, camping, or emergency situations where electricity is unavailable, yet they shed market share annually. Conversion is accelerating as compact electric units become lighter and lower in cost, often bundled with travel-friendly accessories.

Emerging markets once favoured manual devices due to unstable power supply, but grid improvements and battery-backup portability undermine that last barrier. Governments implementing right-to-repair legislation also indirectly strengthen electric adoption, as modular part replacement extends useful life and enhances resale value. The next wave of differentiation will revolve around firmware updates that refine extraction algorithms based on produce type, a feature manual device cannot replicate. Consequently, manual juicers may settle as souvenir-style products rather than practical kitchen workhorses, carving a minor footprint in the broader juicers market.

The Juicers Market Report is Segmented by Type (Centrifugal, Masticating, Triturating, Others), Category Type (Manual, Electric), End-User (Commercial, Residential), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe delivered 21.60% of 2025 revenue, buoyed by high ASPs and strict WEEE compliance that privileges quality-driven brands. Germany exemplifies this premium narrative, where engineering-centric offerings enjoy brand loyalty and low return rates. France and Italy show robust replacement activity, fueled by a culinary culture that values fresh ingredients and aesthetic appliance design. Scandinavia sets the bar for eco-design and energy efficiency, often dictating pan-European regulatory direction. Still, replacement cycles lengthen to 6-7 years as build quality improves, tempering unit-growth prospects. Asia-Pacific, with a projected 7.74% CAGR to 2031, ascends as the juicers market's primary volume engine. China balances robust domestic manufacturing with rising middle-class adoption, though import tariffs influence the competitive calculus for foreign brands. India adds momentum through rapid urbanization and dietary shifts away from sugar-laden packaged drinks toward nutrient-dense alternatives. Japan and South Korea lead in smart appliance uptake, frequently serving as launch pads for IoT innovations that later migrate to Western markets. Southeast Asia's emerging economies favor versatile juicer-blender hybrids that accommodate varied local produce, extending market reach beyond affluent capitals.

North America stands as a testbed for experiential retail and functional beverage crossover concepts, from in-store sampling to wellness retreats that integrate live juice preparation. The highest juicer ASPs in the region tie directly to features like Bluetooth recipe syncing and self-clean cycles that address hassle-barriers. Commercial sales thrive on franchise expansions, with operators negotiating volume discounts and service-level agreements that guarantee sub-24-hour spare-part delivery. Seasonal produce cycles prompt equipment rental programs in cold climates, diversifying revenue for OEMs and rental agencies alike. Regulatory transparency through NSF and UL certifications provides a clear compliance roadmap, encouraging continuous product improvements. Demographic shifts toward smaller households and plant-forward diets sustain per-capita consumption despite stable population counts. Looking ahead, impending single-use plastic restrictions may push consumers further toward home juicing as an environmentally friendly alternative to bottled beverages.

- Breville Group Ltd

- Koninklijke Philips N.V.

- Panasonic Corporation

- Kuvings (NUC Electronics)

- Hurom Co., Ltd.

- Hamilton Beach Brands Holding Co.

- SharkNinja Operating LLC

- Cuisinart (Conair Corporation)

- Omega Juicers (Legacy Companies)

- Tribest Corporation

- Black+Decker (Stanley Black & Decker)

- Aicok (Keyton International)

- JUILIST

- Braun GmbH (De'Longhi Group)

- Russell Hobbs (Spectrum Brands)

- Electrolux AB

- SKG Electric Group

- Sunbeam Products Inc.

- Dash (StoreBound LLC)

- Sage Appliances GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health consciousness & DIY fresh-juice trend

- 4.2.2 Expansion of juice bars & food-service chains

- 4.2.3 Advances in low-noise, high-yield extraction technology

- 4.2.4 Cold-press subscription services boosting at-home adoption

- 4.2.5 Smart/IoT-enabled juicers offering personalized guidance

- 4.2.6 Food-waste incentives driving pulp-reutilization features

- 4.3 Market Restraints

- 4.3.1 High upfront cost of premium appliances

- 4.3.2 Substitution by ready-to-drink packaged juices

- 4.3.3 Stricter e-waste regulations raising disposal costs

- 4.3.4 Growing safety concerns over raw-juice allergens

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Centrifugal Juicer

- 5.1.2 Masticating Juicer

- 5.1.3 Triturating Juicer

- 5.1.4 Others

- 5.2 By Category Type

- 5.2.1 Manual Juicers

- 5.2.2 Electric Juicers

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Residential

- 5.4 Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Online

- 5.4.4 Other Distribution Channels

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Breville Group Ltd

- 6.4.2 Koninklijke Philips N.V.

- 6.4.3 Panasonic Corporation

- 6.4.4 Kuvings (NUC Electronics)

- 6.4.5 Hurom Co., Ltd.

- 6.4.6 Hamilton Beach Brands Holding Co.

- 6.4.7 SharkNinja Operating LLC

- 6.4.8 Cuisinart (Conair Corporation)

- 6.4.9 Omega Juicers (Legacy Companies)

- 6.4.10 Tribest Corporation

- 6.4.11 Black+Decker (Stanley Black & Decker)

- 6.4.12 Aicok (Keyton International)

- 6.4.13 JUILIST

- 6.4.14 Braun GmbH (De'Longhi Group)

- 6.4.15 Russell Hobbs (Spectrum Brands)

- 6.4.16 Electrolux AB

- 6.4.17 SKG Electric Group

- 6.4.18 Sunbeam Products Inc.

- 6.4.19 Dash (StoreBound LLC)

- 6.4.20 Sage Appliances GmbH

7 Market Opportunities & Future Outlook

- 7.1 Modular juicers enabling plant-based milk extraction

- 7.2 Multi-functional appliances demand in emerging economies