PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934584

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934584

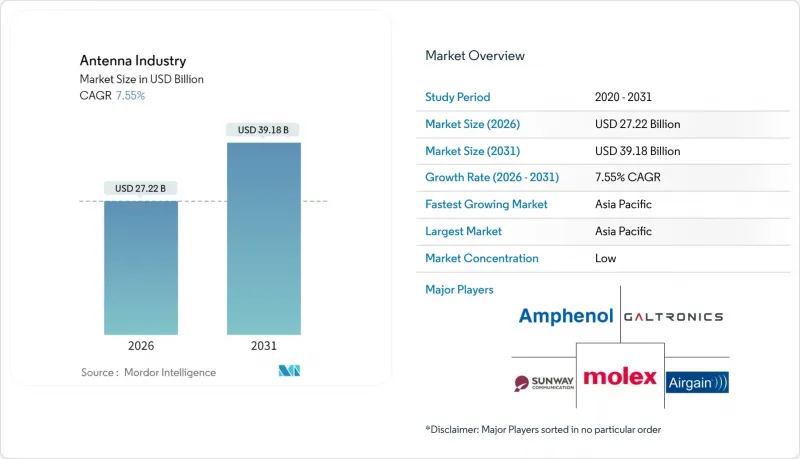

Antenna Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Antenna market size in 2026 is estimated at USD 27.22 billion, growing from 2025 value of USD 25.31 billion with 2031 projections showing USD 39.18 billion, growing at 7.55% CAGR over 2026-2031.

The growth outlook reflects aggressive 5G roll-outs, an expanding universe of IoT nodes, and rising automotive connectivity mandates that together raise demand for advanced multiband and mmWave antenna platforms. Mid-band spectrum densification, high-capacity mmWave deployments, and rapid small-cell proliferation are reshaping infrastructure requirements. Simultaneously, manufacturers are migrating toward Liquid Crystal Polymer and other low-loss substrates that sustain performance at 30 GHz and beyond. Heightened interest in phased-array and massive-MIMO architectures is pushing vendors to integrate beamforming logic within active antenna units. In parallel, power-efficient antenna-on-chip modules are expanding inside wearables and asset-tracking devices, tightening competition between discrete component suppliers and semiconductor incumbents.

Global Antenna Industry Trends and Insights

5G mmWave Infrastructure Acceleration

Operators are rolling out 64T64R and 128T128R massive-MIMO radios that embed hundreds of radiating elements within a single enclosure. Ericsson's 2024 capacity expansion in India underscores the push to localize production of these active antenna systems for regional deployments. The U.S. Federal Communications Commission unlocked additional 47-48 GHz spectrum in 2024, prompting carriers to plan fixed wireless access and enhanced mobile broadband services that demand sub-wavelength array spacing and dynamic beam steering. Such requirements translate into higher volumes of integrated antenna-radio units across macro and small-cell sites.

IoT Device Proliferation Driving Miniaturization

Global IoT node counts surpassed 20 billion in 2024, compelling designers to embed multiband performance into footprints measured in millimeters. Texas Instruments demonstrated antenna-on-chip solutions that collapse the radiating element and RF front end on a single die for sub-GHz industrial links. In asset-tracking beacons and wearable monitors, efficiency gains must coexist with low power budgets and rugged mechanical designs, enlarging the addressable antenna market.

Power-Efficiency Challenges at mmWave Frequencies

At 30 GHz and higher, free-space loss rises sharply, forcing handsets to rely on multiple antenna tiles driven by high-linearity power amplifiers. Studies show mmWave arrays draw 30-40% more energy than sub-6 GHz counterparts, compressing battery life and raising thermal loads in compact devices. Efficiency constraints can delay adoption in mass-market smartphones, tempering near-term growth of the antenna market.

Other drivers and restraints analyzed in the detailed report include:

- Automotive V2X Regulatory Mandates

- Defense Phased-Array System Expansion

- Supply-Chain Concentration Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The stamping category retained 32.74% of antenna market share in 2025 due to cost efficiency and entrenched tooling. LCP antennas, however, are on track for an 8.55% CAGR, gaining traction in 5G smartphones, automotive modules, and mmWave fixed wireless units. The antenna market size derived from LCP implementations will therefore expand more quickly than other material classes over the forecast horizon.

Advancements in low-dielectric-loss plastics allow LCP antennas to inch toward mass-production economies, though specialized ovens and tight moisture-control protocols limit the qualified supplier base. Flexible printed circuit and LDS variants continue to fill mid-tier and niche three-dimensional requirements respectively. Market participants active in LCP processing are expected to capture premium design-win margins as 5G frequencies climb toward 71 GHz.

Printed and flexible technologies held 31.10% share of antenna market size in 2025 because they dominate entry-level IoT and legacy LTE devices. Active phased-array units integrated with RFIC beamformers are now registering a 8.88% CAGR as operators densify 5G macro and small-cell layers. This upswing is pushing antenna vendors toward multidisciplinary competencies spanning materials science, RFIC design, and thermal engineering.

Antennas-in-package and antenna-on-chip architectures are proliferating in wearables and ultra-compact trackers where single-board real estate is scarce. At the opposite end of the spectrum, infrastructure-grade smart antennas feature digital beam steering, self-diagnostics, and remote tilt capabilities. Vendors that bundle software-defined control stacks alongside the hardware are positioned to differentiate beyond commodity price points.

The 1-6 GHz category represented 38.05% of antenna market size in 2025, covering mainstream cellular, Wi-Fi, and Bluetooth. Yet the >30 GHz mmWave slice is delivering an 8.31% CAGR, reflecting heavy investment in 5G FR2 and emerging automotive radar applications. mmWave products confront design hurdles such as oxygen absorption and rain attenuation, requiring higher-gain arrays and lens-based directivity control.

Regulators in the United States and several European nations freed additional 47-48 GHz and 64-71 GHz blocks in 2024, introducing new spectral real estate for fixed wireless access backhaul. Antenna suppliers are developing metamaterial superstrates and hybrid analog-digital beamformers to mitigate link-budget penalties while keeping module power within thermal envelopes.

The Antenna Market Report is Segmented by Type (Stamping, FPC, and More), Technology (AoC, Aip, and More), Frequency Range (Sub-1 GHz, 1-6 GHz, and More), Product (Smartphone, and More), Application (Cellular, Bluetooth/BLE, and More), Installation (Embedded/Internal, and More), End-User Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the antenna market with a 41.00% share in 2025, anchored by China's installation of more than 3 million 5G base stations and India's Digital India fiber-backhaul mandates. Japan's vehicle OEMs pioneer V2X multi-port assemblies while South Korea's semiconductor ecosystem supports advanced substrate fabrication. Regional manufacturing clusters deliver cost and logistics synergies, yet geopolitical frictions spur diversification into Vietnam and India.

North America benefits from the FCC's structured 5G mid-band and mmWave auctions that underpin network densification and fixed wireless access. Ongoing Wi-Fi 7 enterprise refresh cycles reinforce steady demand for multi-band indoor access-point antennas. The European Union aligns spectrum policy under its 5G Action Plan, with automotive V2X mandates catalyzing vehicular antenna expenditures across Germany, France, and Italy.

The Middle East & Africa represent the fastest-growing region at an 7.74% CAGR. Gulf Cooperation Council smart-city programs such as NEOM and Dubai 10X emphasize edge connectivity and IoT sensor grids that require robust antenna infrastructure. Sub-Saharan operators are extending rural coverage through low-band LTE and emergent non-terrestrial networks, creating incremental opportunities for high-gain panel and satellite flat-panel arrays.

- Molex

- Amphenol

- Airgain

- Galtronics

- Sunway Communication

- Luxshare Precision

- Murata Manufacturing

- TE Connectivity

- Qualcomm Technologies

- Texas Instruments

- AAC Technologies

- Fujikura

- KYOCERA-AVX

- Laird Connectivity

- Cobham Advanced Electronic Solutions

- CommScope

- Kathrein SE

- Huizhou SPEED Wireless

- Vishay Intertechnology

- Johanson Technology

- Nordic Semiconductor

- Intel Corporation

- Microchip Technology

- Harman International

- Kymeta Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 5G and mmWave roll-outs requiring high-density active antennas

- 4.2.2 Proliferation of IoT endpoints driving multi-band, ultra-compact designs

- 4.2.3 Automotive V2X mandates in US/EU boosting multi-port vehicular antennas

- 4.2.4 Defense demand for rugged phased-array and conformal antennas

- 4.2.5 Satellite flat-panel growth for mobility and non-Terrestrial Networks (NTN)

- 4.2.6 Flexible/wearable antennas for healthcare and consumer AR devices

- 4.3 Market Restraints

- 4.3.1 Rising RF front-end power-efficiency constraints at mmWave

- 4.3.2 Supply-chain concentration in East Asia creating geopolitical risk

- 4.3.3 Environmental regulations on fluorinated antenna substrates

- 4.3.4 Competition from integrated chip-antenna modules reducing discrete demand

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Stamping Antenna

- 5.1.2 FPC Antenna

- 5.1.3 LDS Antenna

- 5.1.4 LCP Antenna

- 5.1.5 MPI / Meta-Polymer Antenna

- 5.2 By Technology

- 5.2.1 Antenna-on-Chip (AoC)

- 5.2.2 Antenna-in-Package (AiP)

- 5.2.3 Active / Smart Antenna Systems

- 5.2.4 Printed and Flexible Antennas

- 5.2.5 Phased-Array and Massive-MIMO Antennas

- 5.3 By Frequency Range

- 5.3.1 Sub-1 GHz (LF, VHF, UHF)

- 5.3.2 1 to 6 GHz (L, S, C bands)

- 5.3.3 6 to 30 GHz (X, Ku, K, Ka)

- 5.3.4 > 30 GHz (mmWave, EHF, 5G FR2)

- 5.4 By Product

- 5.4.1 Smartphone

- 5.4.2 Laptop and Tablet

- 5.4.3 Wearables and Hearables

- 5.4.4 Networking Equipment (Routers, APs)

- 5.4.5 Other Connected Devices

- 5.5 By Application

- 5.5.1 Main Cellular

- 5.5.2 Bluetooth / BLE

- 5.5.3 Wi-Fi / WLAN

- 5.5.4 GNSS / GPS

- 5.5.5 NFC / RFID / UHF

- 5.6 By Installation

- 5.6.1 Embedded / Internal

- 5.6.2 External / Mounted

- 5.6.3 Infrastructure and Base-Station

- 5.7 By End-user Industry

- 5.7.1 Consumer Electronics

- 5.7.2 Military and Defense

- 5.7.3 Automotive and Mobility

- 5.7.4 Healthcare and Medical Devices

- 5.7.5 Industrial IoT and Smart Cities

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Russia

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 South Korea

- 5.8.4.4 India

- 5.8.5 Middle East and Africa

- 5.8.5.1 Israel

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 United Arab Emirates

- 5.8.5.4 South Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Molex

- 6.4.2 Amphenol

- 6.4.3 Airgain

- 6.4.4 Galtronics

- 6.4.5 Sunway Communication

- 6.4.6 Luxshare Precision

- 6.4.7 Murata Manufacturing

- 6.4.8 TE Connectivity

- 6.4.9 Qualcomm Technologies

- 6.4.10 Texas Instruments

- 6.4.11 AAC Technologies

- 6.4.12 Fujikura

- 6.4.13 KYOCERA-AVX

- 6.4.14 Laird Connectivity

- 6.4.15 Cobham Advanced Electronic Solutions

- 6.4.16 CommScope

- 6.4.17 Kathrein SE

- 6.4.18 Huizhou SPEED Wireless

- 6.4.19 Vishay Intertechnology

- 6.4.20 Johanson Technology

- 6.4.21 Nordic Semiconductor

- 6.4.22 Intel Corporation

- 6.4.23 Microchip Technology

- 6.4.24 Harman International

- 6.4.25 Kymeta Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment