PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934647

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934647

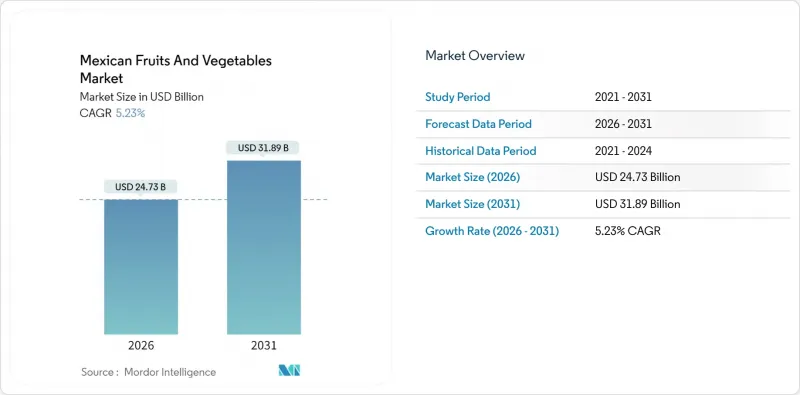

Mexican Fruits And Vegetables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Mexican fruits and vegetables market size in 2026 is estimated at USD 24.73 billion, growing from 2025 value of USD 23.5 billion with 2031 projections showing USD 31.89 billion, growing at 5.23% CAGR over 2026-2031.

This growth trajectory reflects Mexico's strategic positioning as North America's agricultural powerhouse, leveraging proximity to the United States market and year-round production capabilities that few competitors match. Mexico supplies 63% of the United States' vegetable imports and 47% of fruit imports, validating the country's role as North America's year-round produce hub . Northwest supply chains ensure winter supermarket shelves remain stocked, while greenhouses in the Central Highlands are extending berry harvest periods. However, challenges loom, an appreciating peso is tightening export margins, and labor shortages are driving up costs, pushing producers towards automation and scaling. Climate challenges, from northern droughts to intensified Gulf hurricanes, heighten operational risks. Yet, these challenges are spurring quicker adoption of precision irrigation and disease-resistant crops. Meanwhile, investors are making strategic long-term investments in cold-chain logistics, greenhouse plastics, digital agronomy services, and organic certifications, eyeing premium market segments.

Mexican Fruits And Vegetables Market Trends and Insights

Rising United States Import Demand Post-USMCA

The tariff-free architecture of USMCA (United States-Mexico-Canada Agreement) cements Mexico as the default supplier for out-of-season United States produce, with exporters poised to lift shipment values 35% by 2030 . Mexican growers exploit proximity advantages to deliver tomatoes, peppers, and berries during the United States winter deficits, reinforcing dependency that reached USD 18 billion in 2023 . Verification audits are tightening, however, prompting investment in digital traceability to ensure rule-of-origin compliance. The strategy raises switching costs for United States buyers and heightens exposure to future policy shocks. This dependency creates strategic leverage for Mexican exporters while exposing them to United States policy volatility and potential tariff disruptions.These factors collectively underline the critical role of USMCA (United States-Mexico-Canada Agreement) in influencing market dynamics and shaping future trade strategies in the region.

Expansion Of Greenhouse/Protected Cultivation

The protected agriculture market is witnessing significant growth, driven by the expansion of structures by over 1,500 hectares annually. Currently, 66% of tomato production occurs in controlled environments, which enhance pest management and ensures yield consistency, thereby boosting the market's potential. Advanced polyethylene greenhouses are a key driver, enabling Mexican growers to achieve yields 3-4 times higher than open-field cultivation while reducing water consumption by 40% through precision irrigation systems. This technological advancement is propelling the market forward by improving efficiency and sustainability. The capital-intensive nature of the market favors larger enterprises, particularly those with foreign financing, as they meet the stringent food-safety audits required by the United States. However, smaller farmers face challenges due to high upfront costs, which is accelerating market consolidation. The high initial capital requirements and technical complexities act as barriers for smallholder farmers, further contributing to the consolidation trend. These dynamics are shaping the competitive landscape of the protected agriculture market, influencing its growth trajectory.

Labor Shortages and Rising Wages

Farm payroll makes up as much as 40% of specialty-crop costs, and Mexico lost thousands of workers to higher-paying United States H-2A contracts in 2024. Domestic wage inflation hit 20% in Sinaloa and Baja California, squeezing berry profit margins. Technology offers escape routes, but harvest automation remains limited for delicate fruits, widening the gap between capital-rich and traditional operators. New labor laws affecting operational costs compound wage inflation pressures, forcing producers to invest in automation or accept reduced profit margins. The labor shortage creates opportunities for technology adoption but requires significant capital investment that smaller operations cannot afford, potentially accelerating industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy and Social-Program Support

- Export-Driven Berry Acreage Boom

- Climate Volatility (Droughts, Hurricanes)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, vegetables dominate with a 55.20% market share, bolstered by tomato exports worth USD 2.7 billion. Mexico stands tall as the world's eighth-largest tomato producer, meeting 25% of global demand. Notably, Sinaloa contributes a significant 22% to the nation's tomato output. Meanwhile, cucumber and pepper cultivation are rapidly expanding in protected environments across northern states. The established export infrastructure and long-term contracts with United States distributors not only stabilize revenue streams but also fuel investments in greenhouse technology. Yet, the vegetable sector grapples with heightened competition from Central American suppliers and rising production costs, spurred by labor shortages and volatile energy prices.

Fruits are on an upward trajectory, boasting a 6.62% CAGR through 2031. This growth is largely attributed to premium berry exports and a burgeoning avocado industry, both of which injected a hefty USD 6 billion into Mexico's economy in 2024. Avocado production, primarily in Michoacan and Jalisco, constitutes 85% of Mexico's total output and caters to over 90% of the United States' imports. Citrus production sees a 4% uptick in 2024-25, driven by lime production, with Mexico harvesting a leading 2.4 million tons annually. Mango exports hit 80 million boxes in 2024, with a promising 10-15% growth forecasted for 2025. Additionally, stone fruit production, encompassing peaches and cherries, is on the rise, fueled by domestic demand and opportunities for import substitution.

The Mexican Fruits and Vegetables Market is Segments by Crop Type (Fruits, Vegetables). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Market Overview

- Market Drivers

- Market Restraints

- Regulatory Landscape

- Technological Outlook

- Value / Supply-Chain Analysis

- PESTLE Analysis

- List of Key Stakeholders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising United States import demand post-USMCA (United States-Mexico-Canada Agreement)

- 4.2.2 Expansion of greenhouse/protected cultivation

- 4.2.3 Government subsidy & social-program support

- 4.2.4 Export-driven berry acreage boom

- 4.2.5 Niche growth of organic bananas

- 4.2.6 Cold-chain start-ups cutting post-harvest loss

- 4.3 Market Restraints

- 4.3.1 Labor shortages & rising wages

- 4.3.2 Climate volatility (droughts, hurricanes)

- 4.3.3 Strong peso compressing export margins

- 4.3.4 Tomato Brown Rugose Fruit Virus outbreaks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Value / Supply-Chain Analysis

- 4.7 PESTLE Analysis

5 Market Size and Growth Forecasts (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- 5.1 By Crop Type

- 5.1.1 Fruits

- 5.1.2 Vegetables

6 Competitive Landscape

- 6.1 List of Key Stakeholders

- 6.1.1 Secretaria de Agricultura y Desarrollo Rural (SADER)

- 6.1.2 Servicio de Informacion Agroalimentaria y Pesquera (SIAP)

- 6.1.3 Consejo Nacional Agropecuario (CNA)

- 6.1.4 Asociacion Nacional de Exportadores de Berries (Aneberries)

- 6.1.5 Confederacion de Asociaciones Agricolas del Estado de Sinaloa (CAADES)

- 6.1.6 Grupo DRISCOLL'S de Mexico

- 6.1.7 Grupo Alta (Division Agricola)

- 6.1.8 Hortifrut Mexico

- 6.1.9 Divemex

- 6.1.10 SanLucar

- 6.1.11 Grupo Agroexportadora las Brisas

- 6.1.12 Terminal Maritima de Manzanillo

- 6.1.13 Lineage Logistics

- 6.1.14 Netafim

- 6.1.15 Agropark Queretaro

7 Market Opportunities & Future Outlook