PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934673

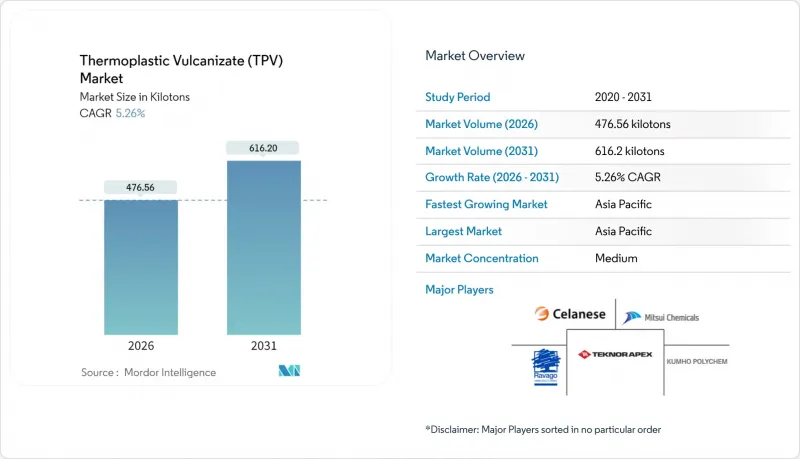

Thermoplastic Vulcanizate (TPV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Thermoplastic Vulcanizate market size in 2026 is estimated at 476.56 kilotons, growing from 2025 value of 452.75 kilotons with 2031 projections showing 616.2 kilotons, growing at 5.26% CAGR over 2026-2031.

This steady expansion reflects a decisive shift by automakers, medical-device firms, and consumer-goods producers toward recyclable elastomers that offer thermoset-like performance at lower overall system costs. Lightweighting imperatives in electric vehicles, regulatory pressure for circular-economy compliance, and rising demand for soft-touch finishes in electronics amplify adoption across regions. Cost analyses show that TPVs can lower part manufacturing expenses by more than 60% versus EPDM rubber, mainly through shorter cycle times and elimination of post-curing steps. Suppliers now promote bio-based and recycled-content grades that cut cradle-to-gate carbon footprints by as much as 50%, providing a credible path for original equipment manufacturers (OEMs) to meet science-based emissions targets. These attributes position the Thermoplastic Vulcanizate market as a material solution of choice, while propylene and EPDM feedstock volatility limits the attractiveness of legacy thermosets.

Global Thermoplastic Vulcanizate (TPV) Market Trends and Insights

Rising Lightweighting Demand from Automotive OEMs

Automakers accelerate material substitution to cut vehicle mass and meet carbon-dioxide fleet targets. TPV components weigh roughly 30% less than comparable EPDM seals yet maintain compression-set resilience, allowing battery-electric models to gain additional driving range. Recent dynamic-vulcanization advances have closed the gap in long-term fatigue performance, enabling TPVs to replace thermosets in door, glass-run, and sunroof systems without altering tooling. Regulatory pressure under the European Union's 2025 CO2 cap magnifies this shift, ensuring sustained demand inflow to the Thermoplastic Vulcanizate market.

Surge in TPV-based Soft-Touch Parts for Consumer Electronics

Handheld electronics brands adopt TPVs to deliver a premium tactile feel while avoiding paint or over-mold steps that complicate recycling streams. The resin's direct-moldable surface eliminates secondary coatings and drops total part cost for grips, bumpers, and wearable-device housings. Integrating 25%-40% recycled content further slashes embodied emissions, and Asia-based contract molders can use standard injection machines, reducing capital barriers. Faster cycle times and compliance with RoHS and REACH regulations reinforce momentum.

Inferior Long-Term Chemical/Wear Resistance vs. Thermoset Rubber

High-acid, oil-field, or abrasive environments still favor specialty thermosets because TPVs can suffer gradual property loss beyond 150 °C. Although polyacrylate-modified TPVs extend service life, they remain a secondary choice for aggressive-media service lines.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Recyclable Elastomeric Materials

- Emergence of Bio-based TPV Grades

- Lack of Closed-Loop Recycling Infrastructure for TPV Scrap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard EPDM/PP compounds accounted for 45.05% of the Thermoplastic Vulcanizate market size in 2025, thanks to lower cost and broad tooling compatibility. The mature formulations meet the majority of weather-seal and interior-trim specifications, offering OEM-qualified performance certifications. Manufacturers leverage twin-screw compounding lines to balance crosslink density and polypropylene melt-flow, enabling tight dimensional tolerances at high throughputs. As a result, global processors continue to prioritize standard grades for programs where cost competitiveness outweighs incremental performance gains.

Volume growth will increasingly originate from bio-based and recycled-content offerings that align with corporate emissions goals. Bio-attributed TPVs are projected to post the fastest 6.76% CAGR, aided by European mandates for circular-economy compliance. Recycled-content variants containing up to 40% post-industrial material give OEMs an immediate path to hit recycled-material thresholds without redesigning parts. High-temperature TPV grades remain niche but strategic, supplying turbo-charger hoses and under-hood gaskets that demand 150 °C continuous use.

The Thermoplastic Vulcanizate Report is Segmented by Product Type (Standard EPDM/PP TPV, High-Performance/Heat-Resistant TPV, and More), Application (Sealing Systems and Weather-Strips, Interior and Exterior Trim, and More), End-User Industry (Automotive, Building and Construction, Consumer Goods, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Kilo Tons).

Geography Analysis

Asia-Pacific led with a 45.70% revenue share in 2025 and is forecast to grow at 6.10% CAGR, outpacing other regions. China's annual production of over 25 million vehicles underpins surging demand for TPV weatherstrips, while Japan's material-science expertise spurs specialty-grade development. India's emerging car market adds incremental volume through local extrusion houses that substitute EPDM profiles with TPV to trim cycle times. Regional feedstock integration lowers polypropylene and EPDM costs, creating a unit-cost advantage that drives exports to Europe and North America. Avient's 2025 expansion of medical-grade TPU output in China evidences supplier commitment to serve Asia-based medical-device OEMs.

North America records steady demand concentrated in Michigan-centric automotive hubs and Mexico's expanding assembly corridors. The Inflation Reduction Act's EV incentives accelerate battery-pack production, boosting call-offs for low-conductivity TPV coolant hoses. Celanese's newly qualified compounder in Suzhou provides Asian-sourced Santoprene pellets for local and export molding operations, illustrating cross-regional supply-chain design. Europe remains the bellwether for sustainability adoption, where ISCC-PLUS-certified TPVs enjoy double-digit growth in premium vehicle lines and green-building facades. The End-of-Life Vehicles Directive pushes OEMs to document recycled content, lifting demand for PCR-infused TPV grades. South America, the Middle East, and Africa together occupy a smaller but rising stake in the Thermoplastic Vulcanizate market. Brazil's revived auto output sparks investments in local extrusion plants, while Gulf-region producers consider downstream TPV compounding leveraging abundant C3 and diene feedstocks. Africa's construction boom increases consumption of TPV water-stop profiles in infrastructure projects, yet limited recycling logistics delay full circularity benefits.

- Avient Corporation

- Celanese Corporation

- DuPont

- Elastron TPE

- FM Plastics

- HEXPOL AB

- Kumho Polychem

- LCY

- LOTTE Chemical CORPORATION

- Mitsubishi Chemical Group Corporation

- Mitsui Chemicals Inc.

- Orbia (Alphagary)

- Ravago

- RTP Company

- Shandong Dawn Polymer Materials Co. Ltd

- Teknor Apex

- Trinseo

- Zylog ElastoComp LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Lightweighting Demand from Global Automotive OEMs

- 4.2.2 Surge in TPV-Based Soft-Touch Parts for Consumer Electronics

- 4.2.3 OEM Shift Toward Recyclable Elastomeric Materials

- 4.2.4 Expansion of EV Battery-Pack Sealing Applications

- 4.2.5 Emergence of Bio-Based TPV Grades

- 4.3 Market Restraints

- 4.3.1 Volatility in Propylene and EPDM Feedstock Prices

- 4.3.2 Inferior Long-Term Chemical/Wear Resistance Vs. Thermoset Rubber

- 4.3.3 Lack of Closed-Loop Recycling Infrastructure for TPV Scrap

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Standard EPDM/PP TPV

- 5.1.2 High-Performance / Heat-Resistant TPV

- 5.1.3 Bio-based TPV

- 5.1.4 Recycled-content TPV

- 5.2 By Application

- 5.2.1 Sealing Systems and Weather-strips

- 5.2.2 Interior and Exterior Trim

- 5.2.3 Under-the-Hood Components

- 5.2.4 Hose and Tubing

- 5.2.5 Wire and Cable

- 5.2.6 Medical Devices

- 5.2.7 Consumer and Sporting Goods Parts

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Building and Construction

- 5.3.3 Consumer Goods

- 5.3.4 Healthcare

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Malaysia

- 5.4.1.7 Thailand

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Avient Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 DuPont

- 6.4.4 Elastron TPE

- 6.4.5 FM Plastics

- 6.4.6 HEXPOL AB

- 6.4.7 Kumho Polychem

- 6.4.8 LCY

- 6.4.9 LOTTE Chemical CORPORATION

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Mitsui Chemicals Inc.

- 6.4.12 Orbia (Alphagary)

- 6.4.13 Ravago

- 6.4.14 RTP Company

- 6.4.15 Shandong Dawn Polymer Materials Co. Ltd

- 6.4.16 Teknor Apex

- 6.4.17 Trinseo

- 6.4.18 Zylog ElastoComp LLP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment