PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934724

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934724

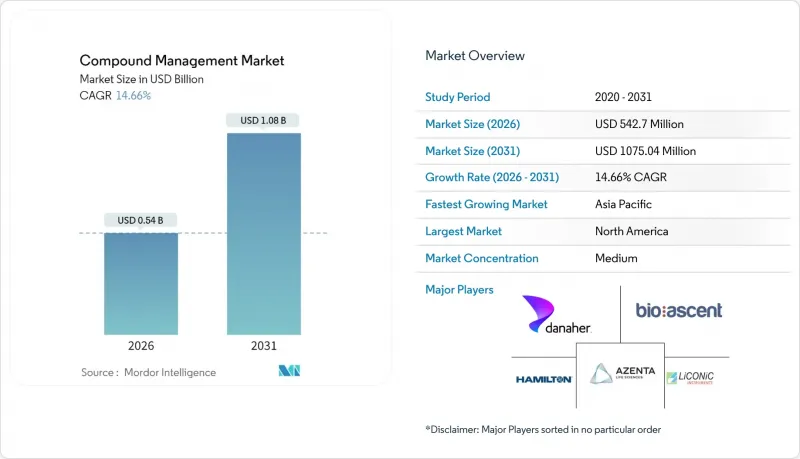

Compound Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Compound Management market is expected to grow from USD 473.32 million in 2025 to USD 542.7 million in 2026 and is forecast to reach USD 1075.04 million by 2031 at 14.66% CAGR over 2026-2031.

Demand is powered by accelerated drug-discovery timelines, AI-enabled screening systems that generate higher sample throughput, and stricter regulatory expectations for automated cold-chain compliance. Large pharmaceutical companies are prioritizing in-house automated stores to safeguard proprietary compound libraries while smaller biotechnology firms adopt specialized biorepositories to manage cell- and gene-therapy samples. Expansion of biologics pipelines, growing venture funding for laboratory robotics, and energy-efficient automation that lowers operating costs are further supporting momentum in the compound management market. Together, these forces are transforming sample storage from a discrete laboratory task into a strategic capability tightly integrated with data analytics and quality-by-design workflows.

Global Compound Management Market Trends and Insights

Expanding AI-Enabled High-Content Screening Platforms

High-content screening systems now link machine-learning algorithms directly to automated storage, enabling real-time retrieval of millions of plates annually and removing manual intervention points that once slowed discovery. Integration requires robust sample tracking, low-temperature robotics, and data pipelines that feed analysis engines without latency. Pharmaceutical R&D groups view these closed-loop workflows as a way to shorten lead-optimization cycles while minimizing false positives. Vendors able to supply integrated hardware-software ecosystems rather than standalone freezers gain competitive advantage. As AI matures, demand for scalable compound libraries rises, underpinning sustained purchases of multi-tier, high-density stores from ambient to -190 °C.

Surging Biologics & Cell-Gene Therapy Pipelines

Cell- and gene-therapy candidates require cryogenic storage reaching -190 °C and chain-of-custody documentation governed by Title 21 CFR 1271.260, which mandates strict temperature bands and contamination safeguards. Automated stores equipped with liquid-nitrogen redundancy protect sample viability while integrated monitoring delivers audit-ready temperature logs. As regulators increase oversight, demand for systems capable of uninterrupted ultra-low storage escalates. Large-volume biologics now outpace small molecules in phase-III pipelines, pushing sponsors to expand cryostorage capacity both in house and at contract development and manufacturing partners. The rise of complex modalities therefore magnifies the role of the compound management market as a foundational element of advanced-therapy supply chains.

High Capex for -80 °C and LN2 Automated Stores

Comprehensive installations capable of holding millions of vials under -80 °C or liquid-nitrogen conditions demand initial investments that can surpass USD 10 million per site. The expense spans stainless-steel racking, robotics, redundant refrigeration, and clean-room infrastructure. Operational costs add monitoring, calibration, backup generators, and routine validation, all of which strain the budgets of early-stage biotech firms. Many innovators therefore opt for outsourcing, but that choice can limit direct control over proprietary libraries. The capital hurdle slows universal adoption and yields a two-tier structure in the compound management market wherein resource-rich pharma groups deploy full in-house automation while smaller entities depend on third-party repositories.

Other drivers and restraints analyzed in the detailed report include:

- Outsourcing of Sample Libraries to Specialized Biorepositories

- Cold-Chain Automation Mandates in Regulated Markets

- Data-Integrity & Cyber-Security Risks in Cloud LIMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Products accounted for 72.64% in 2025 owned infrastructure that grants direct oversight of proprietary libraries. Automated storage systems, liquid-handling robots, and integrated sample-tracking modules account for the largest capital expenditures. In contrast, the services category is projected to expand more rapidly because smaller biotechnology companies lack the funds for large-scale installations yet still require GMP-compliant storage. The shift illustrates how the compound management market size for services will climb with 16.07% between 2026 -2031 steadily alongside robust hardware demand.

Demand for turnkey solutions is blurring traditional lines between the two categories. Manufacturers increasingly provide subscription packages that fold continuous maintenance, software updates, and remote monitoring into a single contract. Hybrid models therefore enable hardware providers to capture recurring revenue streams while clients enjoy predictable operating budgets. This convergence positions fully managed offerings as a gateway for firms that will later migrate to owned assets once pipelines mature.

Chemical libraries continue to anchor discovery programs, explaining their leading share of 51.04% in 2025. Decades of accumulated small-molecule assets and well-defined storage protocols favor automated stores that operate between -20 °C and -80 °C. Yet the fastest growth arises from biosamples used in monoclonal antibodies, cell therapies, and mRNA-based vaccines. Cryostorage requirements for these high-value materials create fresh revenue pools for liquid-nitrogen cabinets equipped with robotic retrieval. The compound management market share for biosamples is therefore set to climb exhibit the fastest rise at an 15.72% CAGR through 2031.

R&D organizations are deploying high-density, low-O2 environments to maintain biological integrity and minimize freeze-thaw cycles. Recent installations couple 384-tube racks with robotic arms that reduce preanalytical errors and run 24/7 to match continuous bioprocessing schedules. The resulting increase in throughput heightens demand for precision temperature monitoring and robust information management, expanding the addressable base for hardware and software suppliers alike.

The Compound Management Market Report is Segmented by Type (Products [Automated Compound/Sample Storage Systems, and More], Services), Sample Type (Chemical Compounds, Biosamples), Application (Drug Discovery, Gene Synthesis, and More), End User (Pharmaceutical Companies, and More), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated the highest revenue with 40.80% in 2025 on the back of concentrated pharmaceutical R&D spend, clear regulatory guidance on electronic records, and a venture-capital ecosystem that funds next-generation laboratory automation. FDA oversight pushes sponsors toward integrated, audit-ready platforms, reinforcing demand for comprehensive hardware-software suites. Mature cold-chain logistics support both in-house and outsourced storage, ensuring the compound management market size in the region remains the largest worldwide.

Asia Pacific is the fastest-growing territory with CAGR 17.16% through 2031, propelled by national policies that seek to localize advanced-therapy manufacturing and shorten drug-approval timelines. China's ongoing regulatory reforms encourage domestic biotechs to invest in automated stores that align with global good-manufacturing-practice requirements. Japan, South Korea, and India are strengthening biopharmaceutical pipelines that increasingly include vaccines and cell therapies, both of which require cryogenic storage solutions. Regional suppliers are stepping up capabilities, yet many projects still rely on imported systems, expanding opportunities for established global vendors.

Europe holds a sizable portion of demand underpinned by rigorous data-protection laws and ambitious carbon-reduction targets. Manufacturers respond with energy-efficient refrigeration, natural-refrigerant alternatives, and closed-loop asset-tracking software that complies with GDPR. Middle East & Africa as well as South America represent emerging pockets of growth where multinational firms place secondary manufacturing sites, although adoption is tempered by limited capital budgets and patchy technical skills. Nevertheless, gradual infrastructure upgrades and government-backed innovation hubs will broaden uptake and contribute incremental gains to the compound management market.

- Azenta

- Beckman Coulter Life Sciences

- BioAscent

- Brooks Automation (SampleStore)

- Evotec

- Hamilton Company

- LiCONiC

- SPT Labtech

- Tecan Group

- Titian Software

- Biosero

- HighRes Biosolutions

- Thermo Fisher Scientific

- FluidX (Azenta)

- Ziath

- Inheco GmbH

- Heraeus CryoPac

- NEXUS Cryogenic Solutions

- Yokogawa RAPID-Lab

- Abcam Compound Libraries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding AI-Enabled High-Content Screening Platforms

- 4.2.2 Surging Biologics & Cell-Gene Therapy Pipelines

- 4.2.3 Outsourcing of Sample Libraries to Specialised Biorepositories

- 4.2.4 Cold-Chain Automation Mandates in Regulated Markets

- 4.2.5 Venture Capital Inflows into Robotic Life-Science Infrastructure

- 4.2.6 ESG-Driven De-Carbonised Lab Operations

- 4.3 Market Restraints

- 4.3.1 High Capex for -80 °C & Ln2 Automated Stores

- 4.3.2 Data-Integrity & Cyber-Security Exposure of Cloud LIMs

- 4.3.3 Shortage of Compound-Management Skillsets in Emerging Hubs

- 4.3.4 Volatile Supply of Lab-Grade Co2/N2 for Cryostorage

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Type

- 5.1.1 Products

- 5.1.1.1 Automated Compound/Sample Storage Systems

- 5.1.1.2 Automated Liquid-Handling Systems

- 5.1.1.3 Other Storage/Handling Systems

- 5.1.2 Services

- 5.1.1 Products

- 5.2 By Sample Type

- 5.2.1 Chemical Compounds

- 5.2.2 Biosamples

- 5.3 By Application

- 5.3.1 Drug Discovery

- 5.3.2 Gene Synthesis

- 5.3.3 Biobanking

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biopharmaceutical Companies

- 5.4.3 Contract Research Organisations

- 5.4.4 Academic & Government Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Azenta Life Sciences

- 6.3.2 Beckman Coulter Life Sciences

- 6.3.3 BioAscent

- 6.3.4 Brooks Automation (SampleStore)

- 6.3.5 Evotec SE

- 6.3.6 Hamilton Company

- 6.3.7 LiCONiC AG

- 6.3.8 SPT Labtech

- 6.3.9 Tecan Trading AG

- 6.3.10 Titian Software

- 6.3.11 Biosero

- 6.3.12 HighRes Biosolutions

- 6.3.13 Thermo Fisher Scientific

- 6.3.14 FluidX (Azenta)

- 6.3.15 Ziath

- 6.3.16 Inheco GmbH

- 6.3.17 Heraeus CryoPac

- 6.3.18 NEXUS Cryogenic Solutions

- 6.3.19 Yokogawa RAPID-Lab

- 6.3.20 Abcam Compound Libraries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment