PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934736

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934736

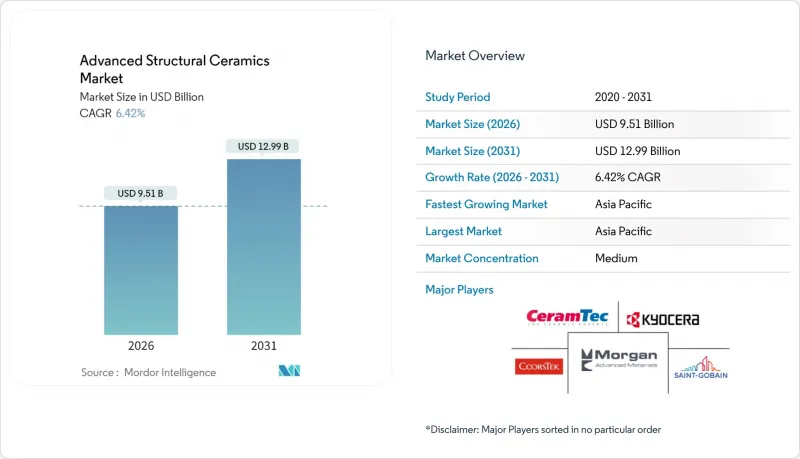

Advanced Structural Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Advanced Structural Ceramics Market was valued at USD 8.94 billion in 2025 and estimated to grow from USD 9.51 billion in 2026 to reach USD 12.99 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Commercial gains stem from the material's ability to operate where metals and polymers fall short, especially in electrified powertrains, 5G infrastructure, and hydrogen turbines. Demand accelerates as aerospace manufacturers seek fuel-saving engines, semiconductor fabs adopt low-loss substrates, and energy firms design hotter, leaner turbines. Consolidation also shapes growth: CoorsTek's USD 245 million purchase of Saint-Gobain Advanced Ceramics improves scale and cuts supply risk. Asia-Pacific retains a production edge thanks to deep semiconductor clusters and strong automotive electrification policies, while additive manufacturing reduces waste and speeds customization, opening fresh revenue pools for specialized grades.

Global Advanced Structural Ceramics Market Trends and Insights

Growing Demand for Lightweight, High-Temperature Materials in Aerospace and Defense

Jet-engine makers now target inlet temperatures above 1,600 °C, a range where silicon carbide and silicon nitride retain full mechanical strength. These ceramics raise fuel efficiency by 15-20% in new turbine platforms, while the U.S. Department of Defense funds hypersonic vehicle programs that rely on ultra-high-temperature composites for Mach 5 flight. Spaceflight demands compound the need, as reusable launch vehicles require thermal-protection systems that survive hundreds of cycles without mass penalties.

Electrification of Powertrains Boosting Thermal-Management Ceramics in EVs

Aluminum nitride and silicon carbide substrates dissipate battery and inverter heat at rates five to ten times higher than polymer fillers. Tesla uses silicon carbide in Model 3 inverters, improving efficiency by around 9% and trimming overall system mass. Premium electric cars now shift to 800 V architectures, and ceramic interface materials keep cells within safe temperature bands during fast charging, extending pack life and enabling shorter pit-stop times.

High Processing Cost Versus Engineered Metals and Polymers

Fully dense silicon carbide parts cost three to five times more than equivalent nickel alloys because powders require 99.9% purity, diamond grinding, and long sintering cycles. Yttria-stabilized zirconia feedstock prices rose 17% after 2024 supply constraints. Added requirements for non-destructive testing and tight statistical controls lift conversion expenses another 10-15%, discouraging use in price-sensitive electronics and small-engine components.

Other drivers and restraints analyzed in the detailed report include:

- Rising 5G and Advanced-Node Semiconductor Deployment Requiring Ceramic Substrates

- Additive Manufacturing Lowers Waste and Enables Complex Ceramic Geometries

- Brittleness Limits Design Flexibility in Dynamic Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina generated 28.55% of the advanced structural ceramics market size in 2025 and remains the workhorse for wear rings, substrates, and implant fixtures. Its broad property set and accessible cost profile ensure sustained demand, particularly in industrial valves and medical tools that require chemical inertness. Silicon carbide forms the next largest slice, lifted by semiconductor and EV traction inverters that need wide-band-gap compatibility at high switching speeds. Zirconate's 8.45% CAGR signals a pivot toward ultrahigh-temperature furnaces and turbine shrouds, where its lower thermal expansion shrinks stress cracks. In response, top producers invest in larger spray-dry towers and isostatic presses to scale volumes while preserving pore-size control.

Broader adoption also hinges on ISO 17025 testing that certifies batch homogeneity and trace element thresholds. As labs meet these standards, aerospace primes feel more confident integrating newer chemistries into hot-section tests. Meanwhile, additive manufacturing enables functionally graded bilayers that marry alumina and zirconate within a single part, optimizing cost and stress distribution. These advances protect alumina's volume base while unlocking higher margins for specialty grades, keeping the advanced structural ceramics market on a balanced growth path.

The Advanced Structural Ceramics Report is Segmented by Material Type (Alumina, Carbides, Zirconate, Nitrides, and Others), End-Use Industry (Automotive, Semiconductors, Medical, Energy, Industrial, Aerospace and Defense, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific posted 53.45% revenue in 2025 and will extend its lead with a 6.98% CAGR thanks to tight coupling between raw-powder refining, component fabrication, and end-product assembly. China commissions fresh kilns capable of 2,200 °C sintering, while Japan advances processing know-how through cross-licensing among KYOCERA, NGK, and Denka.

North America concentrates on high-performance segments tied to aerospace, defense, and medtech. CoorsTek's 2024 purchase of Saint-Gobain Advanced Ceramics folds in new U.S. capacity for armor tiles and semiconductor fixtures, improving domestic supply security. Regulatory rigor, including FDA class-III implant approval and AS9100 quality audits, limits competitive entrants yet stabilizes pricing, allowing producers to recoup research and development outlays.

Europe maintains leadership in ceramic matrix composites, additive manufacturing, and hydrogen-ready turbines. German auto suppliers embed silicon nitride bearings in high-speed e-drives, while the United Kingdom funds ceramics for reusable space engines. The bloc's REACH and CE frameworks ensure environmental compliance and consistent labeling. Emerging Southeast Asian hubs and India start to gain share as multinationals co-locate powder-prep and pressing lines near next-generation electronics assembly, but technical skill gaps remain a medium-term hurdle.

- 3M

- Advanced Ceramics Manufacturing

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek, Inc.

- Ferrotec Holdings Corporation

- KYOCERA Corporation

- MATERION CORPORATION

- Maxon

- Morgan Advanced Materials plc

- Murata Manufacturing Co., Ltd

- Nishimura Advanced Ceramics Co.,Ltd.

- Ortech Advanced Ceramics

- Paul Rauschert GmbH and Co. KG.

- Saint-Gobain

- Schunk Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Lightweight, High-Temperature Materials in Aerospace and Defence

- 4.2.2 Electrification of Powertrains Boosting Thermal-Management Ceramics in EVs

- 4.2.3 Rising 5G and Advanced-Node Semiconductor Deployment Requiring Ceramic Substrates

- 4.2.4 Hydrogen Turbines Creating Need for Sic/Si3N4 Hot-Section Parts

- 4.2.5 Additive Manufacturing Lowers Waste and Enables Complex Ceramic Geometries

- 4.3 Market Restraints

- 4.3.1 High Processing Cost Versus Engineered Metals and Polymers

- 4.3.2 Brittleness Limits Design Flexibility in Dynamic Applications

- 4.3.3 Critical Raw-Material Supply Risks (Yttria, Zirconia, Boron)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Carbides

- 5.1.3 Zirconate

- 5.1.4 Nitrides

- 5.1.5 Other

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Semiconductors

- 5.2.3 Medical

- 5.2.4 Energy

- 5.2.5 Industrial

- 5.2.6 Aerospace and Defense (including Space)

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Ceramics Manufacturing

- 6.4.3 Blasch Precision Ceramics, Inc.

- 6.4.4 CeramTec GmbH

- 6.4.5 CoorsTek, Inc.

- 6.4.6 Ferrotec Holdings Corporation

- 6.4.7 KYOCERA Corporation

- 6.4.8 MATERION CORPORATION

- 6.4.9 Maxon

- 6.4.10 Morgan Advanced Materials plc

- 6.4.11 Murata Manufacturing Co., Ltd

- 6.4.12 Nishimura Advanced Ceramics Co.,Ltd.

- 6.4.13 Ortech Advanced Ceramics

- 6.4.14 Paul Rauschert GmbH and Co. KG.

- 6.4.15 Saint-Gobain

- 6.4.16 Schunk Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment