PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934760

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934760

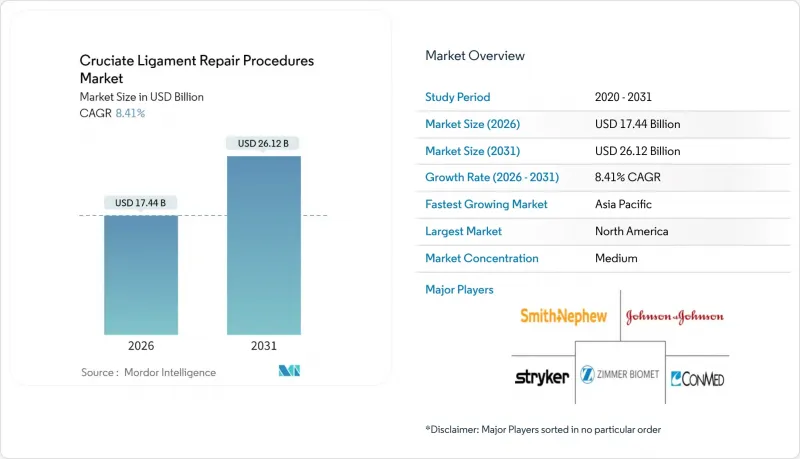

Cruciate Ligament Repair Procedures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cruciate ligament repair procedures market was valued at USD 16.09 billion in 2025 and estimated to grow from USD 17.44 billion in 2026 to reach USD 26.12 billion by 2031, at a CAGR of 8.41% during the forecast period (2026-2031).

Robust momentum stems from growing global sports participation, expanding access to minimally invasive arthroscopy, and the commercial launch of biologic augmentation devices such as the BEAR scaffold that preserve native tissue while reducing donor-site morbidity. Surgeons are increasingly shifting from traditional graft-based reconstruction toward repair-first protocols as six-year outcome studies show comparable stability with lower complication risk. At the same time, payer pressure to lower facility fees is accelerating the migration of routine knee ligament work to ambulatory surgery centers, where average procedure costs fall by up to 33% relative to hospital outpatient settings. Collectively, these trends position the cruciate ligament repair procedures market to deliver sustained double-digit revenue expansion through the decade.

Global Cruciate Ligament Repair Procedures Market Trends and Insights

Rising Prevalence Of Sports & Trauma Injuries

Annual ACL injury incidence tops 250,000 cases in the United States, with athletes aged 15-25 most affected. Cost-utility studies estimate that every surgically treated ACL injury yields USD 50,000 in lifetime societal benefit, translating to USD 10.1 billion in annual savings nationwide. Female athletes remain disproportionately vulnerable; women's soccer, gymnastics, basketball, and lacrosse register ACL injury rates of 0.95 per 10,000 exposures versus 0.80 for men's sports. Prevention programs therefore gain insurer backing as each USD 1 invested delivers USD 7.51 in downstream medical savings. Persistently high injury volumes underpin durable demand for surgical repair, reinforcing top-line expansion for the cruciate ligament repair procedures market.

Advances In Minimally-Invasive Arthroscopy

The introduction of 2 mm nano-arthroscopes enables diagnostic and therapeutic work under local anesthesia, limiting cartilage trauma and expediting post-op recovery. Marker-less navigation achieves femoral tunnel placement deviations of just 1.12-1.86 mm, surpassing conventional landmarks. Artificial-intelligence planning systems now predict femoral implant sizes with 90% accuracy versus 2-D templating at 78%, shortening operative time and inventory waste. Early robotic-assisted arthroscopy platforms further enhance scope control, though capital costs and training remain adoption hurdles. Collectively, these technologies elevate surgical precision and patient outcomes, spurring uptake across the cruciate ligament repair procedures market.

High Procedural & Implant Costs

Average ACL surgery costs USD 7,051 in the United States, with facility fees consuming 68% of the total. Cost-effectiveness assessments in the United Kingdom peg surgical reconstruction at GBP 19,346 per QALY, marginally above NICE's reference threshold. While biologic scaffolds promise faster recovery, they command premium prices that hamper adoption in resource-constrained health systems. Emerging-market payers face additional currency pressure, making high-cost implants difficult to reimburse. Until large-scale pricing discounts or bundled-payment models emerge, high acquisition costs will temper near-term expansion of the cruciate ligament repair procedures market.

Other drivers and restraints analyzed in the detailed report include:

- Higher Success Rates & Shorter Rehabilitation

- Biologic Augmentation (e.g., BEAR Scaffold) Adoption

- Post-Operative Complications & Revision Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ACL Reconstruction retained 54.83% of cruciate ligament repair procedures market share in 2025, underscoring decades of surgeon familiarity and robust long-term data. However, the cruciate ligament repair procedures market size attributed to ACL Repair is projected to grow at 11.53% CAGR through 2031, fueled by BEAR scaffold validation and improved understanding of early-stage healing biology. Meta-analyses covering acute tears find no significant difference in knee laxity or patient-reported outcomes between reconstruction and modern repair, leading more sports-medicine specialists to adopt repair-first protocols for fresh injuries.

In parallel, posterior cruciate ligament work remains niche but clinically important, with repair reserved for proximal avulsions and reconstruction preferred for midsubstance tears. Revision procedures form a small yet growing revenue pool as rerupture rates climb in adolescent athletes returning to pivoting sports. The convergence of percutaneous needle arthroscopy and biologic enhancement is expected to expand the addressable patient cohort, keeping procedure-mix dynamics in flux over the forecast horizon.

Autografts accounted for 46.95% of 2025 revenue, reflecting surgeon confidence in patient-specific tissue that eliminates disease-transmission risk. Nevertheless, biologic scaffolds are delivering a 13.38% CAGR, the fastest among graft types, as long-term follow-ups demonstrate stable kinematics with reduced donor-site pain. Allografts persist where rapid return to activity is prioritized, although processing methods can weaken initial mechanical strength. Synthetic grafts, historically hindered by early loosening, now benefit from bioactive coatings that encourage in-growth, helping the cruciate ligament repair procedures market diversify beyond classical tissue sources.

Looking ahead, multiphasic bone-ligament-bone constructs integrating growth factors and degradable polymers could compress healing timelines and lower revision risk. As regulatory bodies issue clear guidance, surgeon confidence in biologic solutions should rise, further redistributing graft-type shares.

The Cruciate Ligament Repair Procedures Market Report is Segmented by Procedure (Anterior Cruciate Ligament (ACL) Repair, Posterior Cruciate Ligament (PCL) Repair, and More), Graft Type (Autograft, Allograft and More), Fixation Device (Interference Screws, and More), End User (Hospitals, Ambulatory Surgical Centers and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated with 40.31% revenue share in 2025, propelled by high sports participation and rapid adoption of biologic scaffolds following FDA clearance. The United States alone performed more than 200,000 ACL reconstructions in 2024, and payer endorsement of ASCs accelerates outpatient penetration. Canada and Mexico add incremental demand through expanding private insurance coverage and orthopedic workforce development, though biologic reimbursement remains uneven.

Europe ranks second but displays heterogeneous growth. Universal health systems in Germany, France, and the United Kingdom provide broad access, yet cost-effectiveness hurdles can delay biologic uptake. The cruciate ligament repair procedures market size derived from cortical-button devices is expanding fastest in Scandinavia, where evidence-based purchasing favors implants with lower tunnel-widening risk. MDR compliance costs continue to lengthen product-approval timelines, but ultimately elevate surgeon confidence in newly launched devices.

Asia-Pacific is the fastest-growing region at 10.72% CAGR, reflecting expanding middle-class populations and government infrastructure spending in China and India. Japanese interest in motion-preservation techniques aligns well with repair-first approaches, while Australia and South Korea pioneer robotic-assisted arthroscopy deployments. Diverse reimbursement schemes necessitate country-specific launch strategies, yet the overall demographic tailwind ensures that the cruciate ligament repair procedures market gains scale rapidly across Asia-Pacific.

- Arthrex

- Smiths Group

- Stryker

- Zimmer Biomet

- Johnson & Johnson

- Conmed

- Corin Group

- Exactech

- RTI Surgical

- Tissue Regenix

- Integra LifeSciences

- Medtronic

- Miach Orthopaedics

- Enovis (Mathys)

- Bauerfeind

- Ossur

- Parcus Medical

- Orthocell

- Bioretec

- Cayenne Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Sports & Trauma Injuries

- 4.2.2 Advances In Minimally-Invasive Arthroscopy

- 4.2.3 Higher Success Rates & Shorter Rehab Boosting Uptake

- 4.2.4 Biologic Augmentation (E.g., BEAR Scaffold) Adoption

- 4.2.5 Shift To Cost-Effective Ambulatory Surgery Centers

- 4.2.6 AI-Guided Pre-Op Planning Enhancing Outcomes

- 4.3 Market Restraints

- 4.3.1 High Procedural & Implant Costs

- 4.3.2 Post-Operative Complications & Revision Risk

- 4.3.3 Regulatory Uncertainty For Next-Gen Biologics

- 4.3.4 Limited Reimbursement For Repair Vs Reconstruction

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Buyers/Consumers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Procedure

- 5.1.1 ACL Repair

- 5.1.2 ACL Reconstruction

- 5.1.3 PCL Repair

- 5.1.4 PCL Reconstruction

- 5.1.5 Revision Procedures

- 5.2 By Graft Type

- 5.2.1 Autograft

- 5.2.2 Allograft

- 5.2.3 Synthetic Graft

- 5.2.4 Biologic Scaffolds

- 5.3 By Fixation Device

- 5.3.1 Interference Screws

- 5.3.2 Cortical Buttons

- 5.3.3 Suture Anchors

- 5.3.4 Other Fixation Devices

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Orthopedic & Sports Medicine Clinics

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arthrex

- 6.3.2 Smith & Nephew

- 6.3.3 Stryker Corporation

- 6.3.4 Zimmer Biomet

- 6.3.5 Johnson & Johnson (DePuy Synthes)

- 6.3.6 CONMED Corporation

- 6.3.7 Corin Group

- 6.3.8 Exactech

- 6.3.9 RTI Surgical

- 6.3.10 Tissue Regenix

- 6.3.11 Integra LifeSciences

- 6.3.12 Medtronic

- 6.3.13 Miach Orthopaedics

- 6.3.14 Enovis (Mathys)

- 6.3.15 Bauerfeind

- 6.3.16 Ossur

- 6.3.17 Parcus Medical

- 6.3.18 Orthocell

- 6.3.19 Bioretec

- 6.3.20 Cayenne Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment