PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934806

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934806

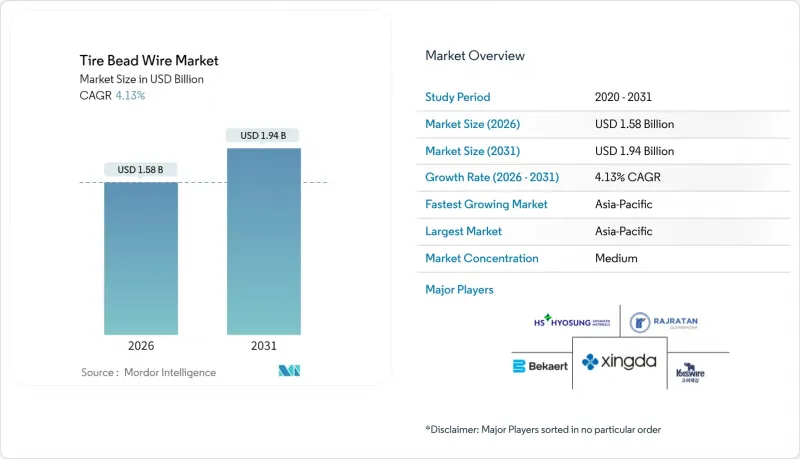

Tire Bead Wire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Tire Bead Wire Market was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 1.94 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031).

The tire bead wire market enjoys a structural tailwind from Asia-Pacific's large-scale vehicle assembly plants, stricter global safety regulations that favor premium reinforcement materials, and an accelerating replacement cycle among commercial fleets that carry e-commerce traffic. High-tensile grades with enhanced ductility dominate value because they reduce rim-slip risk and permit narrower bead sections that save tire weight, an attribute that boosts rolling efficiency for passenger cars and electric vans alike. Manufacturers continue upgrading furnaces and wire-drawing lines to produce ultraclean high-carbon steel that minimizes inclusions; concurrent investments in optical inspection and laser flaw detection improve process capability and support the longer warranty cycles expected by original-equipment tire makers. Competitive dynamics remain mixed: vertically integrated giants secure raw-steel rod under long-term contracts, while mid-tier firms hedge volatility through multi-regional sourcing and scrap-steel blending.

Global Tire Bead Wire Market Trends and Insights

Rising Global Vehicle Production

Global automotive production recovery has created sustained demand for tire bead wire, with tire manufacturers investing a record USD 13 billion in new factories and capacity expansions during 2024. Mexico's tire industry exemplifies this expansion, with production capacity expected to exceed 100 million tires as companies like Yokohama, Zhongce, and Sailun allocate over USD 1 billion for new projects. The strategic positioning of these facilities near major automotive markets reduces logistics costs while meeting stringent supply chain requirements. Cambodia has emerged as another significant manufacturing hub, attracting USD 335 million in tire manufacturing investments during 2025, positioning the country as a key player in the global tire supply chain. This geographic diversification of production capacity creates multiple demand centers for bead wire suppliers, reducing concentration risks while expanding market opportunities.

Expanding Demand from Aviation and Aerospace Tyres

The aerospace sector's robust recovery has generated specialized demand for high-performance bead wire applications. Aircraft tires operate under extreme conditions requiring bead wire with exceptional tensile strength and fatigue resistance, specifications that command premium pricing and drive technological advancement across the broader tire industry. The FAA's stringent maintenance standards for aircraft tire retreading and repair create additional demand for replacement bead wire components, as outlined in Advisory Circular AC 145-4A. Military spending increases, with the U.S. defense budget projected at approximately USD 886 billion for 2024, further support specialized tire applications in defense vehicles and aircraft. This niche segment's technical requirements often pioneer innovations that eventually cascade into commercial tire applications, making aerospace demand a catalyst for broader market advancement.

Volatile Steel and Copper Prices

The Economist Intelligence Unit expects industrial raw-material indices to rise in both 2025 and 2026, sending rubber to USD 2,643 per tonne and pushing ferrous feedstock costs upward. Bead-wire margins shrink whenever high-carbon rod moves in tandem with energy tariffs because producers fix prices under six-month tire-maker contracts. Imports of low-priced tires from Cambodia, Vietnam, India, and Thailand kept U.S. truck-tire prices level during 2024 even as steel costs advanced, creating a squeeze for domestic wire-drawers who cannot pass through surcharges. Currency swings layer on additional unpredictability; a sudden yuan depreciation, for instance, cheapens Chinese rod exports and resets global reference prices overnight. To survive, tier-two vendors engage in financial hedging and scrap-mix optimization, but neither fully shields EBIT margins during sharp spikes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Penetration of Radial Tyres in Developing Economies

- Surge in EV-Specific Bead Designs for Low Rolling-Resistance Tyres

- Tightening Environmental Rules on Wire-Drawing Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-tensile wire supplied 56.63% of tire bead wire market share in 2025, and this slice will expand at 4.59% CAGR through 2031 as regulators and fleet operators favor longer warranty periods. Process innovation is central: vacuum-degassing cuts hydrogen porosity, while calcium-injection controls sulfide morphology to curb brittle failure. Simulation work shows that reducing TiN inclusions below 0.003% by weight slashes wire-drawing breakage incidents by 24%, lowering scrap rates and improving delivery reliability.

Demand granularity is shifting. Passenger-car tire makers now specify tensile strengths of 2,500 MPa and up to 3,000 MPa for run-flat platforms, while EV manufacturers request slender bead gauges that necessitate even cleaner microstructures. Aerospace tires, though low volume, demand 3,400 MPa wire with crack-propagation resistance exceeding 1 million cycles at 60% load, a specification that only a handful of mills can meet. Regular-tensile grades still occupy cost-sensitive niches such as small two-wheel applications and agricultural equipment but face downward price pressure due to commoditized competitive rivalry.

The Tire Bead Wire Report is Segmented by Grade (High-Tensile Strength and Regular-Tensile Strength), Type (Radial Tyres and Bias Tyres), Application (Passenger Vehicle Tires, Commercial Vehicle Tires, and Other Tires), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific furnished 40.02% of global revenue in 2025 and will accelerate at a 5.41% CAGR to 2031, anchored by China's 24.28% tire-industry revenue leap and its 19.22 million-unit output surge during the first three quarters of 2024. The tire bead wire market benefits from government incentives in India that refund import duties on raw steel under the Production Linked Incentive scheme, further lowering cost barriers for new capacity.

North America, while mature, focuses on premium EV and aerospace lines where bead-wire cleanliness is non-negotiable. ArcelorMittal's Alabama mill will supply both electric-motor laminations and ultra-pure SWRH wire rod, providing local feedstock that mitigates freight risk for Arkansas-based Bekaert, which itself invested in new drawing equipment and 38 additional jobs in 2024.

Europe maintains steady volume mainly in Germany and Poland where premium tire brands operate. Stringent EU Green Deal objectives push bead-wire plants toward renewable-energy electric arc furnaces and force a transition to water-based lubricants that curb volatile-organic-compound emissions. Emerging geographies such as Mexico and Cambodia establish themselves as secondary hubs; Mexico's output will breach 100 million tires post-2026, a shift that diversifies sourcing for U.S. vehicle OEMs.

- Aarti Steel International Limited

- Arcelor Mittal

- Bekaert

- Daye Co., Ltd.

- HBT RUBBER INDUSTRIAL CO.,LTD

- HS HYOSUNG ADVANCED MATERIALS

- Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- Kiswire Ltd.

- Rajratan Global Wire Limited

- Shandong Xinhao Tire Materials Co., Ltd.

- Shanghai Metal Corporation

- SNTAI INDUSTRIAL GROUP LTD.

- TIANJIN BLADDER TECHNOLOGY CO.,LTD

- WireCo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Vehicle Production

- 4.2.2 Expanding Demand from Aviation and Aerospace Tyres

- 4.2.3 Rapid Penetration of Radial Tyres in Developing Economies

- 4.2.4 Surge in EV-Specific Bead Designs for Low Rolling-Resistance Tyres

- 4.2.5 Development of High-Modulus Hybrid Bead Reinforcements

- 4.3 Market Restraints

- 4.3.1 Volatile Steel and Copper Prices

- 4.3.2 Tightening Environmental Rules on Wire-Drawing Emissions

- 4.3.3 Concentration Risk in High-Carbon Steel Rod Supply

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 High-Tensile Strength

- 5.1.2 Regular-Tensile Strength

- 5.2 By Type

- 5.2.1 Radial Tyres

- 5.2.2 Bias Tyres

- 5.3 By Application

- 5.3.1 Passenger Vehicle Tires

- 5.3.2 Commercial Vehicle Tires

- 5.3.3 Other Tires

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level overview, market level overview, core segments, financials as available, strategic information, market rank/share, products and services, recent developments)

- 6.4.1 Aarti Steel International Limited

- 6.4.2 Arcelor Mittal

- 6.4.3 Bekaert

- 6.4.4 Daye Co., Ltd.

- 6.4.5 HBT RUBBER INDUSTRIAL CO.,LTD

- 6.4.6 HS HYOSUNG ADVANCED MATERIALS

- 6.4.7 Jiangsu Xingda Steel Tyre Cord Co., Ltd.

- 6.4.8 Kiswire Ltd.

- 6.4.9 Rajratan Global Wire Limited

- 6.4.10 Shandong Xinhao Tire Materials Co., Ltd.

- 6.4.11 Shanghai Metal Corporation

- 6.4.12 SNTAI INDUSTRIAL GROUP LTD.

- 6.4.13 TIANJIN BLADDER TECHNOLOGY CO.,LTD

- 6.4.14 WireCo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment