PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934825

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934825

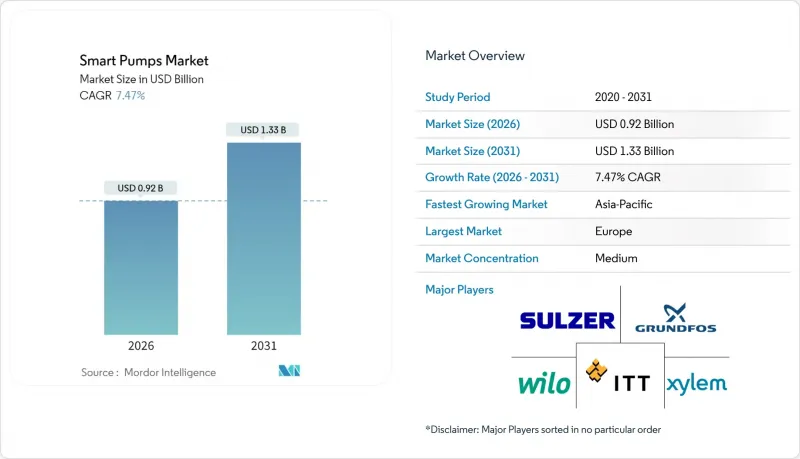

Smart Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The smart pumps market is expected to grow from USD 0.86 billion in 2025 to USD 0.92 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at 7.47% CAGR over 2026-2031.

Expanding digitization across industrial operations, rising deployment of IoT sensors, and stricter energy-efficiency mandates are moving end users away from conventional pumps toward intelligent, connected systems that cut electricity use and improve uptime. European Ecodesign rules, U.S. Department of Energy labelling requirements, and Canada's newly harmonized pool-pump standards underscore how regulation is reshaping fluid-handling choices. Oil and gas operators are adopting edge-computing platforms at remote wells, while water utilities are upgrading aging assets with AI-enabled predictive maintenance that anticipates failures months in advance. Consolidation among pump makers and software firms is accelerating as suppliers race to deliver unified hardware-software-service packages that demonstrate measurable cost savings for utilities and industrial plants.

Global Smart Pumps Market Trends and Insights

Digitization of Oil & Gas Industry

Smart artificial-lift projects now integrate variable-speed drives, downhole sensors, and edge analytics that let field teams optimize wells in real time. In mature U.S. basins, autonomous electric submersible pump (ESP) control has lifted output by more than 700 barrels per day at certain wells. Operating companies also report 20-60% drops in maintenance cost after moving from time-based servicing to data-driven models. As carbon-intensity targets tighten, energy firms see digital pumps as a direct route to lowering both emissions and lifting costs.

Increasing Adoption of IoT-Enabled Pumping Systems

Low-cost sensors paired with NB-IoT or LoRaWAN modules now monitor vibration, power draw, and temperature, predicting breakdowns up to five months in advance with more than 90% accuracy. Field trials at Asian water plants recorded 15.45% lower active-power demand once algorithms automatically trimmed pump speed. Broader facility platforms link pump data to building-management suites, extending insights to chillers, compressors, and valves. [2]

High Initial Cost of Installation & Retrofits

Smart-pump projects often require network upgrades, new drives, and secure gateways, pushing capital outlays well above those for standard replacements. Smaller treatment plants report payback periods extending past three years even when energy savings exceed 25%. Innovative "equipment-as-a-service" models that shift spending from CapEx to OpEx are emerging, but credit access remains limited in developing regions.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Energy-Efficiency Regulations for Fluid-Handling Equipment

- AI-Driven Predictive-Maintenance Programs in Utilities

- Cyber-Security and Data-Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal designs represented 63.20% of revenue in 2025, anchoring the smart pumps market through simple construction and economical operation. Variable-frequency drives integrated with AI now let these pumps adjust speed to track demand curves, keeping them relevant were high volume trumps flow accuracy. Positive displacement units, expanding at an 10.85% CAGR, appeal to oil, gas, and pharma sites that need tight volumetric control. The smart pumps market size for positive displacement technology is projected to widen sharply as shale players prioritize automated chemical-injection skids that trim OPEX.

Precision requirements in enhanced oil recovery, bioreactors, and drug formulation are tilting budgets toward digitally controlled gear, peristaltic, and diaphragm pumps. Developers are adding servo-actuated strokes, automated counterbalancing, and real-time viscosity compensation, narrowing lifecycle costs versus centrifugal rivals. As analytics platforms mature, buyers increasingly compare total cost of ownership instead of first cost, reinforcing the centrifugal leadership while creating profitable niches for specialty displacement products.

The 30-90 m3/h class supplied 31.45% of 2025 revenue as municipal stations and mid-sized factories gravitated to standardized packages with proven support networks. Remote firmware updates and embedded cyber-security modules simplify upkeep, helping this tier defend its share. Meanwhile, high-volume 180-360 m3/h systems are rising at a 9.88% CAGR on the back of mega-projects in desalination, flood mitigation, and steelmaking. Integrated ceramic coatings and composite wear rings now extend mean time between overhauls in abrasive duty, improving the smart pumps market size for these larger units.

Digital twins play a critical role at the higher end: operators feed sensor data into physics-based models to predict cavitation onset and schedule wash-downs just before efficiency dips. As water-transfer corridors widen and climate-resilience projects intensify, demand for intelligent high-flow pumps is likely to outpace replacement cycles in traditional mid-range fleets.

Smart Pumps Market is Segmented by Type (Centrifugal and Positive Displacement), Capacity (m3/H) (Up To 30, 30 - 90, and More), Connectivity (Wired (Ethernet, Fieldbus, HART), Wireless (Wi-Fi, Cellular, LPWAN)), Component (Pump Hardware, Sensors and Instrumentation, and More), End-User (Building Automation, Water and Wastewater, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe accounted for 29.10% of revenue in 2025, supported by binding efficiency mandates and large-scale water-cycle digitization programs such as Spain's PERTE fund, which backs 50 technology projects across utilities. The smart pumps market size for European utilities is further buoyed by renovation grants targeting ancient pipelines in Italy and Germany. EU member states expect electricity savings of 3.7 TWh yearly once new circulator rules fully take effect, underpinning steady procurement pipelines.

Asia-Pacific is the fastest-growing region at 10.45% CAGR through 2031 as China, India, and Southeast Asian nations build reservoirs, seawater desalination plants, and smart-city districts. Singapore's long-term water-self-sufficiency roadmap includes a nationwide sensor grid that dispatches maintenance crews based on AI-flagged anomalies, illustrating how public-sector adoption lifts volumes for private contractors. In energy, Australian LNG terminals and offshore platforms specify wireless-ready pumps for remote asset management, accelerating adoption in industrial roles. North America remains a technology leader thanks to DOE labelling rules and deep experience with industrial IoT. U.S. shale operators serve as reference customers for predictive-maintenance providers, while Canadian municipalities benefit from public-private partnerships that de-risk capital upgrades. South America, Middle East, and Africa add growth pockets tied to resource extraction and climate-resilience infrastructure. Qatar's new USD 22.2 billion civil-works plan, for instance, features smart drainage and pumping hubs that tap cloud dashboards for flood-risk alerts.

- Grundfos Holding A/S

- Xylem Inc.

- Sulzer Ltd.

- Flowserve Corporation

- Wilo SE

- ITT Inc.

- Emerson Electric Co.

- ABB Ltd.

- Pentair plc

- Kirloskar Brothers Limited

- Wanner International Ltd.

- KSB SE & Co. KGaA

- Ebara Corporation

- Franklin Electric Co., Inc.

- Nidec Motor Corporation

- Shanghai Kaiquan Pump (Group) Co., Ltd.

- Tsurumi Manufacturing Co., Ltd.

- DESMI A/S

- Dover Corporation (PSG)

- Torishima Pump Mfg. Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitization of oil and gas industry

- 4.2.2 Increasing adoption of IoT-enabled pumping systems

- 4.2.3 Stringent energy-efficiency regulations for fluid-handling equipment

- 4.2.4 AI-driven predictive-maintenance programs in utilities

- 4.2.5 Government stimulus for smart flood-control and drainage projects

- 4.2.6 Edge-computing deployment in remote mining operations

- 4.3 Market Restraints

- 4.3.1 High initial cost of installation and retrofits

- 4.3.2 Cyber-security and data-privacy concerns

- 4.3.3 Semiconductor-sensor supply-chain volatility

- 4.3.4 Protocol fragmentation and lack of interoperability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Centrifugal

- 5.1.2 Positive Displacement

- 5.2 By Capacity (m3/h)

- 5.2.1 Up to 30

- 5.2.2 30 - 90

- 5.2.3 90 - 180

- 5.2.4 180 - 360

- 5.2.5 Above 360

- 5.3 By Connectivity

- 5.3.1 Wired (Ethernet, Fieldbus, HART)

- 5.3.2 Wireless (Wi-Fi, Cellular, LPWAN)

- 5.4 By Component

- 5.4.1 Pump Hardware

- 5.4.2 Sensors and Instrumentation

- 5.4.3 Variable-Frequency Drives

- 5.4.4 Control and Analytics Software

- 5.5 By End-User

- 5.5.1 Building Automation

- 5.5.2 Water and Wastewater

- 5.5.3 Oil and Gas

- 5.5.4 Chemicals

- 5.5.5 Power Generation

- 5.5.6 Food and Beverage

- 5.5.7 Pharmaceuticals

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Italy

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 Japan

- 5.6.4.2 China

- 5.6.4.3 India

- 5.6.4.4 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 Israel

- 5.6.5.3 Qatar

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Kenya

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Grundfos Holding A/S

- 6.4.2 Xylem Inc.

- 6.4.3 Sulzer Ltd.

- 6.4.4 Flowserve Corporation

- 6.4.5 Wilo SE

- 6.4.6 ITT Inc.

- 6.4.7 Emerson Electric Co.

- 6.4.8 ABB Ltd.

- 6.4.9 Pentair plc

- 6.4.10 Kirloskar Brothers Limited

- 6.4.11 Wanner International Ltd.

- 6.4.12 KSB SE & Co. KGaA

- 6.4.13 Ebara Corporation

- 6.4.14 Franklin Electric Co., Inc.

- 6.4.15 Nidec Motor Corporation

- 6.4.16 Shanghai Kaiquan Pump (Group) Co., Ltd.

- 6.4.17 Tsurumi Manufacturing Co., Ltd.

- 6.4.18 DESMI A/S

- 6.4.19 Dover Corporation (PSG)

- 6.4.20 Torishima Pump Mfg. Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment