PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934858

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934858

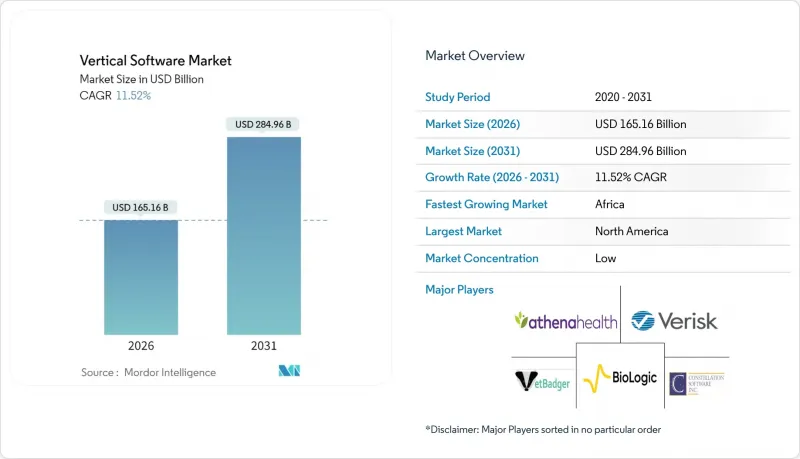

Vertical Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The vertical software market was valued at USD 148.10 billion in 2025 and estimated to grow from USD 165.16 billion in 2026 to reach USD 284.96 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Cloud-first delivery models, embedded regulatory frameworks, and artificial-intelligence toolkits are accelerating adoption across regulated industries, mid-sized manufacturing, and agriculture. Intensifying competition between incumbent horizontal vendors and pure-play specialists is sharpening product differentiation through domain-level workflows and embedded payments. North America retains a leadership position, but Africa is expanding fastest as governments support digital modernization and as subscription pricing lowers barriers for small and medium enterprises. Simultaneously, rising cyber-liability premiums and persistent legacy data silos in the public sector temper deployment velocity.

Global Vertical Software Market Trends and Insights

Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US & Europe

Purpose-built industry clouds radically shorten implementation cycles by bundling compliant data models and pre-configured workflows. Rapid uptake is evident in the European cloud market, which rose from USD 197 billion in 2023 to USD 232 billion in 2024. Hospitals, factories, banks, and retailers increasingly choose turnkey platforms to minimise custom coding and audit risk. Embedded financial services within these clouds augment recurring revenue and lock-in, driving the +3.5% lift to the overall vertical software market CAGR. Capabilities such as real-time data lineage, reference architectures, and continuous compliance monitoring further strengthen switching costs and create defensible moats.

Regulatory Compliance Pressures in BFSI & Healthcare Boosting Specialized Solutions

Evolving fair-lending rules effective October 2025 require automated valuation models, pushing banks toward software that embeds audit trails and model-risk governance. Parallel scrutiny surrounds AI-enabled medical devices, compelling providers to rely on platforms with traceable data pipelines and managed updates. These pressures escalate demand for sector-specific SaaS, producing a +2.8% contribution to growth as buyers seek to avoid fines and reputational risk.

Legacy Data Silos Slowing Vertical Cloud Migration in the Public Sector

Fragmented on-premise estates hinder interoperability, as documented by the US Defense Innovation Board's assessment of poor data discoverability and access. Complex migration programs inflate budgets and extend timelines, causing a -1.2% drag on the vertical software market. Agencies often require phased dual-run architectures that slow realisation of cloud benefits until legacy retirement is complete.

Other drivers and restraints analyzed in the detailed report include:

- AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- Rising Cyber-Liability Insurance Costs Inflating TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based offerings account for 69.92% of the vertical software market size in 2025. Pay-as-you-go pricing, auto-scaling, and managed compliance services lower total ownership costs by up to 30%. Enterprises also value built-in integration to public cloud AI services that sharpen decision support. Conversely, on-premise solutions, while only 30.08% of spending, register a 13.97% CAGR as data-sovereignty mandates and air-gapped security requirements re-enter the planning agenda.

Hybrid architectures are becoming standard; organisations retain customer PII or genomic data on-site while streaming anonymised telemetry into cloud analytics engines. The approach satisfies regulators yet still captures agility. IoT adoption amplifies this mix, as operational sensors feed both local edge servers and cloud models, yielding real-time insights and long-term optimisation. Suppliers that offer unified orchestration across these environments now enjoy premium win rates.

Enterprises accounted for 51.67% of 2025 revenue, reflecting multi-site rollouts and complex compliance demands. They typically execute phased global templates that anchor vendor roadmaps and feed account expansion via embedded payments or data-exchange modules. However, SME uptake is accelerating, delivering a 14.38% CAGR that outpaces the overall vertical software market. Pay-monthly pricing, guided implementation wizards, and marketplace add-ons lower both financial and skills barriers.

Big-data analytics drive measurable gains for smaller firms, with studies showing revenue and efficiency improvements once proprietary dashboards reveal supplier and customer behavior. Vendors respond with modular packaging that allows incremental adoption, ensuring immediate value before upsell. Rural broadband expansion and mobile-first interfaces further open latent demand, particularly in Africa and Southeast Asia, reinforcing the long-run addressable pool for the vertical software industry.

The Vertical Software Market Report Segmented by Deployment Model (Cloud, and On-Premises), Organization Size (Small and Medium Enterprise, and Large Enterprise), End-User Industry (Banking, Financial Services, and Insurance (BFSI), Educational Institution, and More), Application (Customer Relationship Management, Enterprise Resource Planning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 51.76% of 2025 revenue, supported by sophisticated cloud infrastructure, deep venture funding, and strict compliance regimes that reward domain-rich platforms. Federal incentives for electronic health-record modernisation and open banking APIs further cement demand. Large-scale reference customers in regulated arenas provide proof points that ripple through mid-market segments, reinforcing network effects and the overall vertical software market.

Asia-Pacific is advancing at a 14.02% CAGR. Manufacture-heavy economies, such as China, Japan, and South Korea, deploy AI toolkits for predictive maintenance and smart-factory orchestration, while India's SME population leverages subscription models to leapfrog legacy systems. Regional AI spending is expected to hit USD 90.7 billion by 2027. Although talent constraints persist, tier-one universities and cross-border training partnerships are helping to narrow the skills gap.

Europe presents mixed dynamics with a stringent data-protection framework spurs demand for industry clouds with certified controls, yet cross-border regulatory divergence introduces complexity and cost. Providers able to localise hosting, attest to sovereign-cloud standards, and integrate ESG reporting tools are winning procurement contests and reinforcing momentum in the vertical software market. Africa is expanding at fastest CAGR of 15.97%. Driven by swift SME digitization and robust demand in agriculture, fintech, and healthcare, Africa is carving out a pivotal role in the vertical software market. South Africa, Nigeria, and Egypt are at the forefront, championing the adoption of vertical SaaS solutions that cater to local compliance, language nuances, and a mobile-first approach, all bolstered by government-led digital transformation initiatives.

- Constellation Software Inc.

- Verisk Analytics, Inc.

- athenahealth, Inc.

- Bio-Logic Science Instruments SA

- VetBadger LLC

- FastBound LLC

- Mail Technologies Inc.

- Granular, Inc. (Corteva)

- Farmbrite, LLC

- Renderforest LLC

- Veeva Systems Inc.

- Guidewire Software, Inc.

- Epic Systems Corporation

- Procore Technologies, Inc.

- Toast, Inc.

- Shopify Inc.

- Oracle Health (Cerner Corp.)

- Teladoc Health, Inc.

- IFS AB

- Infor, Inc.

- ServiceTitan, Inc.

- Blackbaud, Inc.

- MINDBODY, Inc.

- Intelerad Medical Systems Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US and Europe

- 4.2.2 Regulatory Compliance Pressures in BFSI and Healthcare Boosting Specialized Solutions

- 4.2.3 AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- 4.2.4 Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- 4.2.5 Government-funded Smart-Hospital Programs Propelling Health-tech Software

- 4.2.6 Subscription Pricing Unlocking SME Penetration in Africa

- 4.3 Market Restraints

- 4.3.1 Legacy Data Silos Slowing Vertical Cloud Migration in Public Sector

- 4.3.2 Shortage of Domain-savvy Talent Limiting Customization Speed

- 4.3.3 Rising Cyber-Liability Insurance Costs Inflating TCO

- 4.3.4 Multi-jurisdiction Regulations Hindering Cross-border Rollouts in EU and ASEAN

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Education

- 5.3.4 Government and Legal

- 5.3.5 Media, Entertainment and Hospitality

- 5.3.6 Clothing and Apparel

- 5.3.7 Agriculture and Farming

- 5.3.8 Other End-user Industries

- 5.4 By Application

- 5.4.1 Customer Relationship Management

- 5.4.2 Enterprise Resource Planning

- 5.4.3 Supply Chain Management

- 5.4.4 Human Resource Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emiartes

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overviews, Segments, Financials, Strategy, Rank/Share, Products, Developments)

- 6.4.1 Constellation Software Inc.

- 6.4.2 Verisk Analytics, Inc.

- 6.4.3 athenahealth, Inc.

- 6.4.4 Bio-Logic Science Instruments SA

- 6.4.5 VetBadger LLC

- 6.4.6 FastBound LLC

- 6.4.7 Mail Technologies Inc.

- 6.4.8 Granular, Inc. (Corteva)

- 6.4.9 Farmbrite, LLC

- 6.4.10 Renderforest LLC

- 6.4.11 Veeva Systems Inc.

- 6.4.12 Guidewire Software, Inc.

- 6.4.13 Epic Systems Corporation

- 6.4.14 Procore Technologies, Inc.

- 6.4.15 Toast, Inc.

- 6.4.16 Shopify Inc.

- 6.4.17 Oracle Health (Cerner Corp.)

- 6.4.18 Teladoc Health, Inc.

- 6.4.19 IFS AB

- 6.4.20 Infor, Inc.

- 6.4.21 ServiceTitan, Inc.

- 6.4.22 Blackbaud, Inc.

- 6.4.23 MINDBODY, Inc.

- 6.4.24 Intelerad Medical Systems Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment