PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934887

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934887

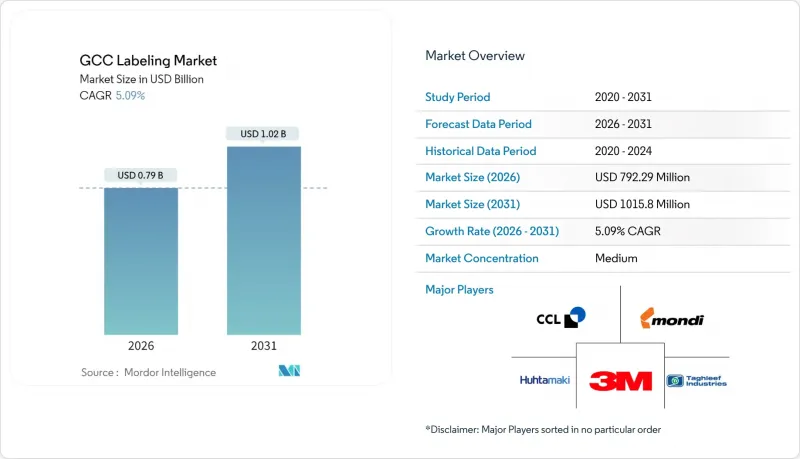

GCC Labeling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

GCC labeling market size in 2026 is estimated at USD 792.29 million, growing from 2025 value of USD 753.84 million with 2031 projections showing USD 1015.8 million, growing at 5.09% CAGR over 2026-2031.

Consistent demand from fast-moving consumer goods, pharmaceuticals, and e-commerce fulfillment continues to drive the GCC labeling market's solid growth path, as regulators push for transparent supply chains and brands seek premium shelf appeal. Pressure-sensitive formats retain a commanding lead because automated lines, prevalent in Saudi Arabia and the United Arab Emirates, favor their quick application. At the same time, the GCC labeling market benefits from a pronounced shift toward digital inkjet presses that support shorter runs and variable data, aligning with mandated traceability codes. Saudi Arabia's industrial localization and the UAE's smart infrastructure collectively amplify regional opportunities, while sustainability commitments accelerate a pivot toward recyclable substrates.

GCC Labeling Market Trends and Insights

Digitally-Printed Label Adoption Surges

Converters in the GCC labeling market are migrating to digital inkjet presses because brand owners favor short runs, faster artwork changes, and serialized coding. The 6.58% CAGR for digital technology reflects cost-efficient LED-UV curing systems that lower power use by nearly 80%, as demonstrated when Paragon ID in the United Kingdom shifted to Fujifilm's LuXtreme platform. Enhanced variable-data capability also meets traceability rules tied to Saudi and Emirati food safety legislation, giving early digital adopters a service advantage. Local converters that invest in modular inkjet heads position themselves for higher margins on premium, versioned labels. However, laggards face potential loss of key accounts as procurement teams prioritize suppliers able to deliver just-in-time volumes with near-zero plate changeover delays. The trajectory, therefore, elevates capital-intensive, digitally agile plants as preferred partners in the GCC labeling market.

Food-Grade Regulatory Tightening

The UAE's mandatory nutritional panel mandate, effective in 2024, and Saudi Arabia's stricter shelf-life disclosures under the Saudi Food and Drug Authority's rules intensify compliance requirements. Manufacturers are increasingly requiring ISO 22000-certified converters to avoid product recalls, thereby expanding opportunities for firms with integrated quality labs in the GCC labeling market. Specialized low-migration inks and migration-tested adhesives have become essential, prompting material suppliers to certify their products and raising the entry bar for unqualified competitors. Consolidation of vendor lists favors converters with documented hazard-analysis protocols and automated vision inspection. Those capabilities convert regulatory pressure into premium pricing opportunities, reinforcing transparency as a commercial differentiator.

Capital Intensity of High-Speed Lines

Modern hybrid presses capable of speeds of 200 meters per minute cost more than USD 2 million each, a hurdle for family-owned firms that dominate local supply bases. Many lenders still perceive printing equipment as specialized collateral, limiting financing options in the GCC labeling market. Without access to capital, smaller converters struggle to match lead times demanded by multinational beverage fillers, risking disqualification from preferred vendor lists. Leasing or toll-printing partnerships offer interim relief, yet sustained competitiveness ultimately hinges on balance-sheet strength. Consequently, larger groups with stronger banking relationships tend to gain market share, thereby increasing consolidation pressure across Saudi Arabia and the UAE.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Packaging and IoT-Enabled Labels

- Localization Push under GCC Industrial Strategies

- Volatile Petrochemical-Based Raw Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure-sensitive formats delivered 53.72% of GCC labeling market revenue in 2025, supported by straightforward application on automated fillers and compatibility with multiple container shapes. This dominance highlights the continued buoyancy of the GCC labeling market size for pressure-sensitive labels, even as new formats emerge. Demand is reinforced by Saudi dairy and Emirati ready-meal producers that require high-speed, low-downtime labeling. Yet, shrink labels, benefiting from beverage bottlers seeking 360-degree graphics, are forecast to grow at a rate of 5.92% annually through 2031. Their heat-application process enables tamper-evident packaging and brilliant shelf appeal, resonating with premium soft drink launches across the UAE. Converters investing in hybrid narrow-web lines capture both pressure-sensitive and shrink work, mitigating volume swings. Extended-content and heat-transfer labels serve niche chemical drums and regulatory-heavy pharma packs, supplying dependable but lower-volume orders. As marketing teams pursue unique unboxing experiences, demand fragments across multiple label types, prompting converters to expand their portfolios and compress lead times in the GCC labeling market.

Polypropylene films accounted for 37.21% of 2025 sales, as they strike a balance between rigidity, print receptivity, and cost, making them the de facto choice for personal care and chilled-food applications. The GCC labeling market share held by polypropylene reflects the abundant local resin output from Saudi and Emirati petrochemical complexes, which anchors domestic supply stability. Even so, polyethylene terephthalate substrates are projected to rise at a 6.05% CAGR, as brands adopt mono-material packaging strategies that match bottle and label materials for easier recycling. The GCC labeling market size, represented by PET labels, is thus expected to increase, particularly in premium beverages that favor high-gloss clarity. Paper continues to be used in dry goods and ambient retail, but loses ground where condensation resistance is a concern. Polyethylene films excel in industrial lubricants due to their chemical durability. Material suppliers now emphasize post-consumer recycled content and APR-certified constructions, such as UPM Raflatac's HDPE-compatible labels, which transitioned from the trial stage to commercial scale in 2024. This shift keeps sustainability at the center of procurement decisions.

The GCC Labeling Market Report is Segmented by Type (Pressure-Sensitive Labels, Shrink Labels, In-Mold Labels, Wrap-Around Labels, and Other Types), Material (Paper, Polypropylene, Polyethylene, PET, and Other Plastics), Print Technology (Flexographic, Offset, Gravure, Digital Inkjet, and Screen), End-User Industry (Food, Beverage, and More), and Geography (UAE, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- CCL Industries Inc.

- Avery Dennison Corporation

- Taghleef Industries Inc.

- Mondi plc

- 3M Company

- Huhtamaki Oyj

- Brady Corporation

- Honeywell International Inc.

- Sigma Middle East Label Industries LLC

- Print Pack Labels LLC

- Rotopack Labeling Solutions LLC

- Gulf Printing and Packaging Co.

- Zebra Technologies Corporation

- Sato Holdings Corporation

- Multi-Color Corporation

- UPM Raflatac Oy

- Fujifilm Holdings Corporation

- Domino Printing Sciences

- HP Development Company L.P.

- Durst Phototechnik AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitally-printed label adoption surges

- 4.2.2 Food-grade regulatory tightening

- 4.2.3 Smart-packaging and IoT-enabled labels

- 4.2.4 Localization push under GCC industrial strategies

- 4.2.5 E-commerce fulfillment labeling boom

- 4.2.6 Foreign direct investment in FMCG manufacturing

- 4.3 Market Restraints

- 4.3.1 Capital intensity of high-speed lines

- 4.3.2 Volatile petrochemical-based raw material prices

- 4.3.3 Skills gap in digital pre-press operations

- 4.3.4 Fragmented regulatory barcode standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

- 4.9 Import and Export Analysis

- 4.10 Labeling Equipment Suppliers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Pressure-Sensitive Labels

- 5.1.2 Shrink Labels

- 5.1.3 In-mold Labels

- 5.1.4 Wrap-around Labels

- 5.1.5 Other Types

- 5.2 By Material

- 5.2.1 Paper

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyethylene (PE)

- 5.2.4 Polyethylene-terephthalate (PET)

- 5.2.5 Other Plastics

- 5.3 By Print Technology

- 5.3.1 Flexographic Printing

- 5.3.2 Offset Printing

- 5.3.3 Gravure Printing

- 5.3.4 Digital Inkjet Printing

- 5.3.5 Screen Printing

- 5.4 By End-user Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Healthcare and Pharmaceutical

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Chemicals and Industrial

- 5.5 By Geography

- 5.5.1 United Arab Emirates

- 5.5.2 Saudi Arabia

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Bahrain

- 5.5.6 Oman

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CCL Industries Inc.

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Taghleef Industries Inc.

- 6.4.4 Mondi plc

- 6.4.5 3M Company

- 6.4.6 Huhtamaki Oyj

- 6.4.7 Brady Corporation

- 6.4.8 Honeywell International Inc.

- 6.4.9 Sigma Middle East Label Industries LLC

- 6.4.10 Print Pack Labels LLC

- 6.4.11 Rotopack Labeling Solutions LLC

- 6.4.12 Gulf Printing and Packaging Co.

- 6.4.13 Zebra Technologies Corporation

- 6.4.14 Sato Holdings Corporation

- 6.4.15 Multi-Color Corporation

- 6.4.16 UPM Raflatac Oy

- 6.4.17 Fujifilm Holdings Corporation

- 6.4.18 Domino Printing Sciences

- 6.4.19 HP Development Company L.P.

- 6.4.20 Durst Phototechnik AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment