PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934910

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934910

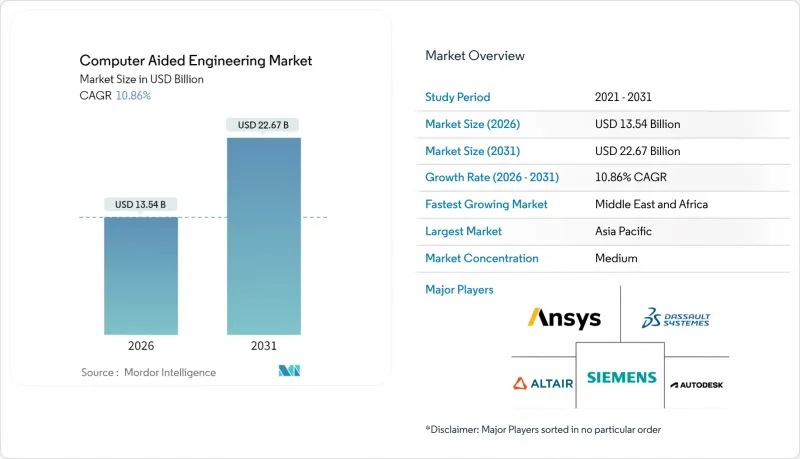

Computer Aided Engineering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The computer aided engineering market was valued at USD 12.21 billion in 2025 and estimated to grow from USD 13.54 billion in 2026 to reach USD 22.67 billion by 2031, at a CAGR of 10.86% during the forecast period (2026-2031).

High-performance cloud infrastructure, AI-assisted solvers, and stricter regulatory expectations for virtual prototyping are accelerating adoption across product-development lifecycles. Companies are replacing late-stage physical testing with early-stage multiphysics simulation to meet tighter launch windows and embedded sustainability targets. Asia's leadership, sustained by large-scale semiconductor investments and rising automotive electrification, underpins global momentum. Software licences remain the principal revenue generator, yet advisory and integration services are surging as enterprises struggle to keep pace with the skills required for increasingly complex digital-twin environments.

Global Computer Aided Engineering Market Trends and Insights

AI/ML-Driven Generative Design for EV Lightweighting in EU & China

Automakers are coupling generative algorithms with finite-element solvers to reduce curb weight without sacrificing crashworthiness. MeshWorks shows development-time cuts of up to 70% for battery modules, letting engineers test previously impractical topologies.Studies demonstrate 10% mass reductions translating into 6-8% energy-consumption improvements-vital in markets pushing aggressive zero-emission mandates. The impact is magnified in Europe and China, where subsidy structures and fleet-average CO2 targets make lightweight architectures a competitive requirement. Suppliers integrating AI-ready simulation templates expect shorter homologation cycles and better utilisation of multi-disciplinary teams.

Regulatory Push for Virtual Prototyping in Aerospace (FAA/EASA)

The FAA's 2024 powered-lift aircraft rule recognises simulation data for certification evidence, shrinking costly full-scale tests. Parallel initiatives at EASA encourage digital engineering to accelerate propulsion and structure approvals. Hardware-software platforms such as the Millennium M1 CFD Supercomputer compress multi-week aero-thermal studies into hours, aligning engineering throughput with tighter programme timetables. The result is lower non-recurring expenditure and faster entry into service across both commercial and defence segments.

Pay-per-Use Cloud Licensing Uncertainty for Tier-2 Auto Suppliers

Variable billing creates planning risk for parts makers whose simulation demand peaks late in OEM programme cycles. Academic reviews show SMEs lag larger peers in predictive-analytics uptake because of resource constraints and cost opacity. Until vendors standardise subscription tiers or introduce consumption caps, smaller firms may delay full migration, tempering overall computer aided engineering market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native HPC Access Fuelling SME Adoption in Asia

- Sub-5 nm Semiconductor Thermal Challenges Requiring Multiphysics CFD

- Validation Gaps in Bio-mechanical Models Limiting Surgical Device Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment contributed 72.85% of 2025 revenue, reflecting its centrality to solver innovation and interface upgrades that underpin the computer-aided engineering market. Ansys' 2024 R1 release rolled out modular workspaces and AI-ready data pipelines, illustrating steady investment in workflow productivity. Expanded physics libraries and GPU acceleration lock in entrenched licence renewals, even as newer entrants chip away in specialist niches. Services, though smaller, are scaling faster at 12.46% CAGR as enterprises confront knowledge gaps in multiphysics, cloud orchestration, and AI model training.

Rising complexity is widening the divide between standard out-of-the-box deployment and best-practice adoption. Advisory firms now bundle domain-specific templates-such as battery thermal run-away analyses-streamlining project kick-offs. This consultative layer is particularly valuable to organisations transitioning from legacy finite-element tools to integrated digital-twin platforms. Consequently, services revenue is capturing a larger portion of total computer aided engineering market size, especially within emerging economies where in-house expertise remains scarce.

Finite element analysis accounted for 35.22% of the 2025 computer-aided engineering market share, sustained by broad applicability across structural, thermal, and electromagnetic problems. Continuous improvements in mesh automation and material models enable faster convergence for high-fidelity assemblies. Generative design overlays now exploit topology-optimised lattices to reduce metal volumes in aircraft brackets, achieving double-digit weight savings.

Computational fluid dynamics is the fastest-growing category at 11.74% CAGR as electronics thermal bottlenecks and aerodynamic optimisation converge. Cadence's GPU-based Millennium M1 supercomputer demonstrates order-of-magnitude speed-ups for unsteady flow simulations, unlocking high-resolution studies within design-cycle windows. As AI frameworks predict flowfields with sparse CFD training sets, vendors anticipate broader uptake in process industries and renewable-energy design.

The Computer Aided Engineering Market is Segmented by Component (Software, Services), Software Type (Finite Element Analysis, Computational Fluid Dynamics, and More), Deployment (On-Premise, Cloud Based), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Vertical (Automotive, Aerospace and Defense, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia led with 38.12% of 2025 revenue, buoyed by semiconductor expansion and state-backed manufacturing digitalisation. China's drive for self-reliance spurred breakthroughs such as LICOMK++ ocean modelling, underscoring domestic HPC capability growth scmp.com. India's National Supercomputing Mission and South Korea's fab investments further support a double-digit regional CAGR. The region's outsized electronics supply chain keeps multiphysics CFD licences in sustained demand.

North America ranked second, dominated by the United States' activity in defence modernisation and aerospace digital twins. Federal incentives for clean-energy infrastructure amplify demand for structural and thermal simulation in wind-turbine and grid-storage projects. Cloud-hyperscaler proximity affords users elastic compute headroom, accelerating AI integration within day-to-day workflows.

Europe retains strong footholds in automotive and commercial aviation simulation. Clean-Aviation funding for hydrogen propulsion and ultra-efficient airframes steers budgets toward next-generation CFD and composite-model solvers. Regulations mandating lifecycle carbon accounting motivate digital-twin rollouts for predictive maintenance and fuel-burn optimisation. Meanwhile, the Middle East posts the highest regional CAGR at 12.17% as refiners deploy energy-optimisation twins that cut unplanned downtime by 35%.

- ANSYS Inc.

- Dassault Systemes SE

- Siemens Digital Industries Software

- Altair Engineering Inc.

- Hexagon AB (MSC Software)

- Autodesk Inc.

- ESI Group

- PTC Inc.

- COMSOL AB

- Bentley Systems Inc.

- SimScale GmbH

- NUMECA International

- EnginSoft SpA

- BETA CAE Systems (Cadence)

- Alibre LLC

- Flow Science Inc.

- AVEVA Group plc

- CD-adapco (Siemens)

- Ceetron AS (Tech Soft 3D)

- Rescale Inc.

- Materialise

- NVIDIA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of AI/ML-Driven Generative Design for EV Lightweighting in EU and China

- 4.2.2 Regulatory Push for Virtual Prototyping in Aerospace (FAA/EASA)

- 4.2.3 Cloud-Native HPC Access Fuelling SME Adoption in Asia

- 4.2.4 Sub-5 nm Semiconductor Thermal Challenges Requiring Multiphysics CFD

- 4.2.5 Sustainability-Led Digital Twins for Energy Optimisation in Middle East Refineries

- 4.2.6 Defence Modernisation (Hypersonics) Driving FSI Simulations in US and Australia

- 4.3 Market Restraints

- 4.3.1 Pay-per-Use Cloud Licensing Uncertainty for Tier-2 Auto Suppliers

- 4.3.2 Validation Gaps in Bio-mechanical Models Limiting Surgical Device Uptake

- 4.3.3 Export-Control Curbs on HPC Chips Capping Simulation Scale in China

- 4.3.4 Steep Learning Curve for Multiphysics Coupling in India

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Investment Analysis

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Software Type

- 5.2.1 Finite Element Analysis

- 5.2.2 Computational Fluid Dynamics

- 5.2.3 Multibody Dynamics

- 5.2.4 Optimisation and Simulation

- 5.3 By Deployment

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Vertical

- 5.5.1 Automotive

- 5.5.2 Aerospace and Defence

- 5.5.3 Electronics and Electrical

- 5.5.4 Industrial Equipment

- 5.5.5 Healthcare

- 5.5.6 Energy and Utilities

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 APAC

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 South-East Asia

- 5.6.4.6 Australia and New Zealand

- 5.6.4.7 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ANSYS Inc.

- 6.4.2 Dassault Systemes SE

- 6.4.3 Siemens Digital Industries Software

- 6.4.4 Altair Engineering Inc.

- 6.4.5 Hexagon AB (MSC Software)

- 6.4.6 Autodesk Inc.

- 6.4.7 ESI Group

- 6.4.8 PTC Inc.

- 6.4.9 COMSOL AB

- 6.4.10 Bentley Systems Inc.

- 6.4.11 SimScale GmbH

- 6.4.12 NUMECA International

- 6.4.13 EnginSoft SpA

- 6.4.14 BETA CAE Systems (Cadence)

- 6.4.15 Alibre LLC

- 6.4.16 Flow Science Inc.

- 6.4.17 AVEVA Group plc

- 6.4.18 CD-adapco (Siemens)

- 6.4.19 Ceetron AS (Tech Soft 3D)

- 6.4.20 Rescale Inc.

- 6.4.21 Materialise

- 6.4.22 NVIDIA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment