PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937278

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937278

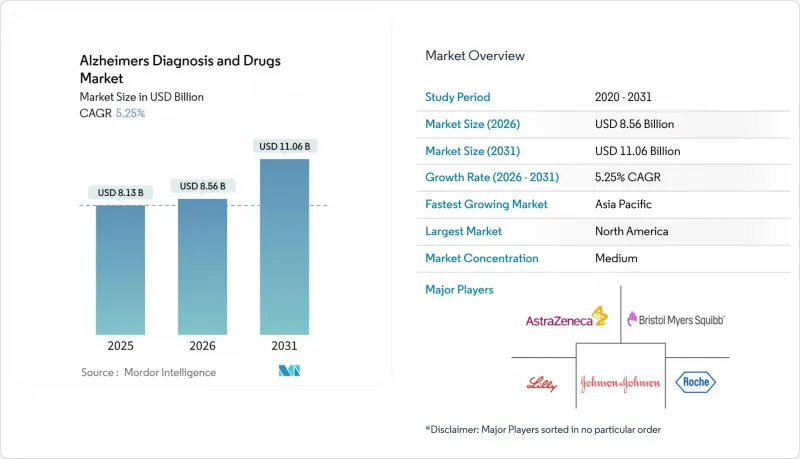

Alzheimers Diagnosis And Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Alzheimers diagnosis and drugs market is expected to grow from USD 8.13 billion in 2025 to USD 8.56 billion in 2026 and is forecast to reach USD 11.06 billion by 2031 at 5.25% CAGR over 2026-2031.

Growth stems from the first wave of disease-modifying antibodies, widening biomarker reimbursement, and AI-enabled imaging platforms that shorten diagnostic time lines. Anti-amyloid monoclonal antibodies have re-energized investor sentiment, while blood-based tests are solving capacity bottlenecks created by limited PET scanners and cerebrospinal fluid labs. Governments in North America and parts of Europe are adding value-based payment rules that link reimbursement to real-world outcomes, a step that should reduce payer push-back on expensive biologics. Asia-Pacific health systems are spending heavily on neurology training and telehealth, positioning the region for double-digit gains. Meanwhile, venture funding is gravitating toward AI-driven diagnostic start-ups and combination-therapy programs that hedge the historically high Phase III failure rate.

Global Alzheimers Diagnosis And Drugs Market Trends and Insights

Accelerating Approvals of Anti-Amyloid Monoclonal Antibodies

Full FDA approval of lecanemab in July 2024 and conditional EMA authorization two months later established a commercial pathway for disease-modifying therapy, prompting Medicare to relax access rules through Coverage with Evidence Development. Donanemab's FDA nod in August 2024 intensified competition, forcing manufacturers into value-based pricing talks earlier in the product life cycle. Hospital networks are already expanding infusion suites, while specialty pharmacies negotiate risk-sharing agreements that tie discounts to cognitive-score maintenance. The approvals have also raised the regulatory bar, with future candidates expected to demonstrate plaque removal plus clinically meaningful slowing of decline. Asia-Pacific agencies are mirroring Western regulators, with Japan granting priority review to lecanemab within six months of the U.S. decision, reinforcing the global momentum behind disease-modifying biologics.

Rising Biomarker-Based Early Diagnosis Uptake

The FDA's 2024 breakthrough-device designations for plasma phospho-tau assays capped a decade-long quest for minimally invasive screening, shrinking dependence on PET and lumbar puncture. Updated clinical guidelines now recommend blood biomarkers as first-line tests, which has multiplied testing volumes at Quest Diagnostics and LabCorp. Primary-care physicians are adopting screening workflows that add just five minutes to routine visits, enabling earlier therapeutic intervention. Health-plan actuaries are recalculating cost-offsets, noting that each year of delay in institutional care saves USD 17,000 per patient in U.S. Medicaid outlays. Emerging economies are piloting mobile phlebotomy vans that collect samples in rural areas, broadening diagnostic reach without major bricks-and-mortar investment.

Late-Stage Drug Failure Rates & Sunk R&D Costs

Phase III attrition above 90% continues to discourage big-ticket bets, underscored by Roche's 2024 exit from gantenerumab after USD 2 billion in spend. Investors price higher risk, upping demanded equity stakes and milestone contingencies. Mid-cap biotech is turning to platform approaches, aiming to recycle failed assets into combination regimens rather than scrapping them outright. Policy makers fear innovation droughts and are experimenting with tax credits that trigger only on successful proofs of concept, thereby sharing downside risk. Academic consortia are lobbying for dedicated NIH lines that cover "bridge-to-pivot" studies, extending the life of promising molecules that miss single-endpoint trials.

Other drivers and restraints analyzed in the detailed report include:

- Growing Geriatric Population & Disease Prevalence

- AI-Enabled Neuro-Imaging Workflow Efficiencies

- Payer Hesitancy on High-Cost Biologics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics held 58.90% of Alzheimers diagnosis and drugs market share in 2025, anchored by cholinesterase inhibitors and newly approved anti-amyloid antibodies. Yet diagnostics generated the momentum, growing at 11.95% CAGR as payers embraced blood-based assays. The Alzheimers diagnosis and drugs market size attributable to anti-amyloid biologics is projected to climb from USD 2.3 billion in 2025 to USD 5.47 billion in 2031, a 15%-plus CAGR that outpaces the overall market trajectory. Blood biomarkers from C2N Diagnostics and Quanterix saw Medicare coverage in late 2024, propelling U.S. test volumes beyond 1 million annually. AI-infused imaging maintains clinical relevance for therapy monitoring but cedes first-line screening to plasma assays that cost one-tenth as much. CSF testing declines as patients and physicians favor less invasive options, while pharmacogenomic kits experience a modest rebound due to APOE4-linked treatment personalization.

Competition intensifies within diagnostics, where intellectual-property moats rely on proprietary antibodies and machine-learning classifiers. New entrants bundle blood tests with digital-cognitive assessments, offering integrated care pathways to accountable-care organizations. Reagent makers negotiate volume-based discount clauses to lock in lab clients before large-scale commoditization sets in. On the therapeutic side, pipeline diversity broadens to include tau vaccines, small-molecule inflammasome inhibitors, and gene-editing constructs aimed at APOE4 modulation. Regulatory agencies encourage adaptive-trial designs that recycle placebo arms across candidates, trimming timelines by nine months on average. Collectively, these trends keep diagnostics as the innovation bellwether even as therapeutics deliver the bulk of short-term revenue.

The Alzheimers Diagnosis and Drugs Market Report is Segmented by Product (Therapeutics [Cholinesterase Inhibitors, Anti-Amyloid MAbs, and More] and Diagnostics [Brain Imaging, CSF Biomarker Tests, and More]), End User (Hospitals & Specialty Clinics, Diagnostic Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 45.10% revenue in 2025, propelled by early access to FDA-cleared biologics and CMS reimbursement for blood biomarkers. The region's Alzheimers diagnosis and drugs market size is predicted to swell to USD 5.05 billion by 2031, aided by Medicare rules that embed value-tracking requirements. Canadian provinces align benefits, though Quebec negotiates independent price caps that shave average antibody prices by 12%. Mexico leverages medical tourism, drawing Latin American patients for PET scans and tapping cross-border insurance partnerships that package lodging with diagnostic bundles.

Asia-Pacific is the fastest-growing bloc, charting a 10.55% CAGR. China's dementia plan mandates amyloid-PET and blood-biomarker availability in every prefecture-level hospital by 2028. The Alzheimers diagnosis and drugs market share of APAC could hit 28.60% by 2031 as Japan accelerates reimbursement for AI imaging and South Korea rolls out nationwide cognitive-screening programs at community clinics. Australia's expedited-review pathway shaves six months off regulatory timelines, making the country a beachhead for Western firms entering Asia. India pilots public-private elder-care hubs that combine day-care, telehealth, and diagnostics under a single roof, financed by municipal bonds.

Europe offers a mature yet fragmented landscape. Germany's sickness funds cover blood-biomarker tests ahead of most EU peers, but France still ties reimbursement to PET confirmation, slowing routine uptake. The Alzheimers diagnosis and drugs market size in the EU will inch from USD 2.7 billion in 2025 to USD 3.52 billion in 2031, a restrained 4.55% CAGR given payer cost controls. The Horizon Europe program injects USD 350 million into dementia consortia, widening the R&D pool for mid-sized biotech. Eastern European members lag on therapeutic adoption due to constrained specialty-care budgets, though they gain from EU structural funds that upgrade imaging infrastructure.

- Abbvie

- AC Immune SA

- AstraZeneca

- Biogen

- Bristol-Myers Squibb

- C2N Diagnostics

- Cognition Therapeutics

- Eisai

- Eli Lilly and Company

- Roche

- GE Healthcare

- Johnson & Johnson

- Lundbeck A/S

- Novartis

- Pfizer

- Siemens Healthineers

- Sun Pharmaceuticals Industries

- TauRx Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biomarker-Based Early Diagnosis Uptake

- 4.2.2 Accelerating Approvals of Anti-Amyloid Monoclonal Antibodies

- 4.2.3 Growing Geriatric Population & Disease Prevalence

- 4.2.4 Expansion of Blood-Based Diagnostic Test Reimbursement

- 4.2.5 AI-Enabled Neuro-Imaging Workflow Efficiencies

- 4.2.6 Regional Public-Private Consortia for Dementia R&D

- 4.3 Market Restraints

- 4.3.1 Late-Stage Drug Failure Rates & Sunk R&D Costs

- 4.3.2 Limited Specialist Workforce for Disease-Modifying Therapy Monitoring

- 4.3.3 Diagnostic Biomarker Performance Variability Across Ethnicities

- 4.3.4 Payer Hesitancy on High-Cost Biologics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Therapeutics

- 5.1.1.1 Cholinesterase Inhibitors

- 5.1.1.2 NMDA Receptor Antagonists

- 5.1.1.3 Anti-amyloid mAbs

- 5.1.1.4 Anti-tau & other DMTs

- 5.1.2 Diagnostics

- 5.1.2.1 Brain Imaging

- 5.1.2.2 CSF Biomarker Tests

- 5.1.2.3 Blood-based Biomarker Tests

- 5.1.2.4 Genetic Testing

- 5.1.1 Therapeutics

- 5.2 By End User

- 5.2.1 Hospitals & Specialty Clinics

- 5.2.2 Diagnostic Laboratories

- 5.2.3 Research & Academic Institutes

- 5.2.4 Home-care / Remote Testing Providers

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 AC Immune SA

- 6.3.3 AstraZeneca PLC

- 6.3.4 Biogen Inc.

- 6.3.5 Bristol-Myers Squibb

- 6.3.6 C2N Diagnostics

- 6.3.7 Cognition Therapeutics

- 6.3.8 Eisai Co., Ltd.

- 6.3.9 Eli Lilly and Company

- 6.3.10 F. Hoffmann-La Roche AG

- 6.3.11 GE HealthCare

- 6.3.12 Johnson & Johnson

- 6.3.13 Lundbeck A/S

- 6.3.14 Novartis AG

- 6.3.15 Pfizer Inc.

- 6.3.16 Siemens Healthineers

- 6.3.17 Sun Pharma

- 6.3.18 TauRx Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment