PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937283

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937283

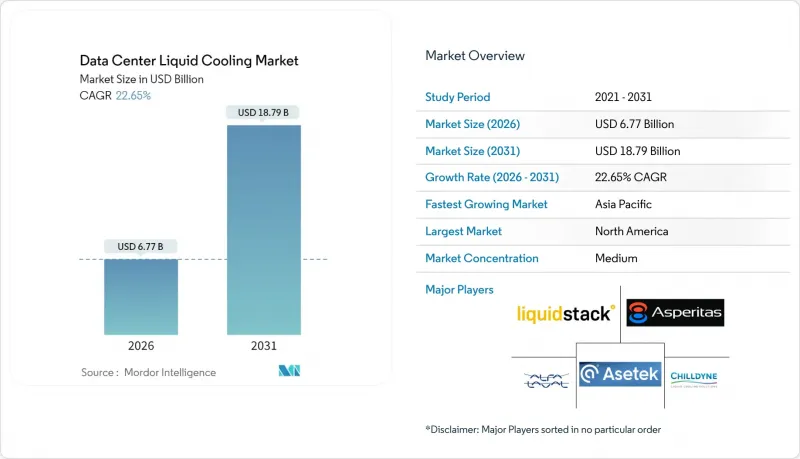

Data Center Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The data center liquid cooling market was valued at USD 5.52 billion in 2025 and estimated to grow from USD 6.77 billion in 2026 to reach USD 18.79 billion by 2031, at a CAGR of 22.65% during the forecast period (2026-2031).

Rising rack densities above 30 kW, the accelerating use of graphics processing units for AI models, and tighter sustainability mandates are converging to make liquid cooling a core architectural requirement for modern facilities. Direct-to-chip solutions continue to dominate because they retrofit into existing racks, while two-phase immersion systems are advancing fastest as operators pursue still higher thermal efficiencies. Hyperscale cloud providers are translating early pilots into fleet-wide rollouts, and their aggregated demand is lowering unit costs for enterprise and colocation buyers. Meanwhile, policy incentives that favour heat re-use and lower carbon intensity are reinforcing liquid adoption across North America, Europe, and selected Asia-Pacific (APAC) hubs.

Global Data Center Liquid Cooling Market Trends and Insights

Surging rack densities drive liquid cooling necessity

Data center operators deploying NVIDIA H200 GPUs face 700 W thermal loads per device, and air cooling cannot cost-effectively remove that heat at volume. With processors delivering up to 1.9 times prior-generation performance, operators can shrink server counts but must dissipate concentrated heat. Liquid cooling, therefore, shifts from an optional efficiency measure to indispensable infrastructure, enabling higher density without blowing past facility power-usage-effectiveness thresholds. The data center liquid cooling market benefits directly because every incremental kilowatt above 20 kW per rack pushes operators toward liquid solutions.

Hyperscale net-zero commitments accelerate adoption

Cloud giants have pledged fleet-wide net-zero emissions and see liquid cooling as a 20% energy-reduction lever compared with legacy air systems. European regulations further require heat recovery from data centers above 1 MW, intensifying uptake of liquid architectures that simplify thermal capture. These combined voluntary and regulatory forces turn liquid cooling into a compliance infrastructure as well as an operational efficiency strategy, expanding the data center liquid cooling market beyond early adopters.

Limited field expertise constrains deployment velocity

Liquid systems demand skills in pipe fitting, leak detection, and pump sizing that many legacy data center staff lack. Training programs are expanding, but until the talent pool deepens, roll-out schedules will remain lengthier than air-based projects.

Other drivers and restraints analyzed in the detailed report include:

- OEM warranty coverage reduces deployment risk

- Semiconductor reference designs standardize implementation

- Retrofit costs challenge brown-field adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-to-chip captured 42.85% of the 2025 data center liquid cooling market share and will continue to anchor short-term growth. Operators favour its drop-in nature for CPUs and moderate-power GPUs. The data center liquid cooling market size for immersion solutions will climb fastest at a 26.62% CAGR, helped by AI training clusters that need extreme heat flux removal. Facilities are increasingly hybrid, using rear-door heat exchangers for moderate racks and immersion baths for GPU islands. Patent filings by Invented and other Taiwanese firms underscore sustained engineering momentum.

A second-order effect is that component suppliers are redesigning pumps, valves, and quick-disconnects to tolerate higher flow rates and non-conductive fluids. As products standardize, procurement cycles shorten and total installed cost falls, reinforcing the technology shift.

Single-phase hydrocarbons accounted for the largest slice of the data center liquid cooling market size in 2025 due to mature supply chains. However, two-phase fluorocarbons deliver stronger heat-transfer coefficients and will post a 25.64% CAGR. 3M's scheduled phase-out of PFAS fluids is reshaping sourcing; Chinese specialty chemical makers are stepping in to backfill demand for semiconductor and server coolant buyers. Governments such as the United Kingdom are funding research into next-generation, low-global-warming-potential fluids, accelerating a broader shift to environmentally aligned chemistries. Operators are also exploring glycol mixes for facilities where water conservation is paramount. Nanofluids, infused with metal oxides or carbon nanotubes, remain at pilot stage, but test results suggest 10-15% conductivity gains that could unlock thinner cold plates in the coming decade.

The Data Center Liquid Cooling Market Report is Segmented by Cooling Technology (Immersion Cooling, Direct-To-Chip Liquid Cooling, and More), Coolant Type (Single-Phase Hydrocarbon Fluids, Two-Phase Fluorocarbon Fluids, and More), Data Center Type (Hyperscale, Colocation, Enterprise, and More), Application (HPC, AI/ML, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserves its lead position thanks to hyperscale capex and pro-investment tax regimes. Kansas grants 20-year sales-tax holidays on data center spending above USD 250 million, and Massachusetts offers similar exemptions for projects over USD 50 million. The Inflation Reduction Act further augments returns with clean-energy credits, tipping many new builds toward liquid-ready designs.

Europe is the second growth engine. The Energy Efficiency Directive obliges data centers above 1 MW to evaluate heat recovery, and Scandinavian district-heating grids provide an economic off-take route for captured thermal energy. France rewards facilities that prove superior power-usage effectiveness with reduced energy taxes. Collectively, these rules elevate liquid systems from an efficiency choice to a compliance requirement, especially where water-side economizers already exist.

APAC represents the fastest-growing regional slice of the data center liquid cooling market. China is bridging the coolant gap created by 3M's PFAS exit, while Japan's utilities incentivize energy-efficient compute nodes. India's rapid digitalization, supported by dedicated data-center-friendly policies in Telangana and Uttar Pradesh, provides greenfield opportunities to leapfrog directly into liquid architectures. Taiwanese manufacturers, headlined by Inventec, dominate global patent filings and are exporting integrated cold-plate assemblies worldwide.

Africa, Latin America, and the Middle East remain smaller but strategic. Their hot climates and costly power make air systems less attractive, opening niches where compact immersion baths can serve telecom and fintech workloads with minimal mechanical plant.

- Alfa Laval Corporate AB

- Asetek A/S

- Asperitas BV

- Chilldyne Inc.

- CoolIT Systems Inc.

- Fujitsu Ltd.

- Kaori Heat Treatment Co., Ltd.

- Lenovo Group Ltd.

- LiquidStack Inc.

- LiquidCool Solutions Inc.

- Iceotope Technologies Ltd.

- Rittal GmbH and Co. KG

- Schneider Electric SE

- Submer Technologies SL and Submer Inc.

- Vertiv Group Corp.

- Wiwynn Corporation

- 3M Company

- Engineered Fluids Inc.

- Green Revolution Cooling Inc.

- Solvay SA

- Mikros Technologies

- Midas Green Technologies LLC

- USystems Ltd. (Legrand Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging rack densities (>30 kW) in AI and HPC facilities

- 4.2.2 Hyperscale operators' net-zero roadmaps accelerating liquid adoption

- 4.2.3 OEM warranties now covering direct-to-chip loops

- 4.2.4 Nvidia and AMD liquid-ready reference designs driving ecosystem

- 4.2.5 Government incentives for green DCs (e.g., EU Taxonomy) underwrite CAPEX

- 4.2.6 Re-use of waste-heat for district heating monetises OPEX savings

- 4.3 Market Restraints

- 4.3.1 Limited field expertise among facility engineers

- 4.3.2 High upfront retrofit costs for brown-field sites

- 4.3.3 Fluid material-compatibility concerns (long-term seals, PCB)

- 4.3.4 Supply risk of specialty dielectric fluids

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes (advanced air, two-phase CO?)

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 Segmentation by Cooling Technology

- 5.1.1 Immersion Cooling

- 5.1.2 Direct-to-Chip Liquid Cooling

- 5.1.3 Rear-Door Heat Exchangers (RDHx)

- 5.1.4 Cold-Plate / In-row Liquid Systems

- 5.2 Segmentation by Coolant Type

- 5.2.1 Single-Phase Hydrocarbon Fluids

- 5.2.2 Two-Phase Fluorocarbon Fluids

- 5.2.3 Water / Glycol Solutions

- 5.2.4 Nanofluids and Other Specialty Liquids

- 5.3 Segmentation by Data Center Type

- 5.3.1 Hyperscale

- 5.3.2 Colocation

- 5.3.3 Enterprise / On-Premise

- 5.3.4 Edge and Micro DCs

- 5.4 Segmentation by Application / Workload

- 5.4.1 High-Performance Computing (HPC)

- 5.4.2 Artificial Intelligence / Machine Learning

- 5.4.3 Cryptocurrency Mining

- 5.4.4 Cloud and Virtualisation

- 5.5 Segmentation by Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of MEA

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Alfa Laval Corporate AB

- 6.4.2 Asetek A/S

- 6.4.3 Asperitas BV

- 6.4.4 Chilldyne Inc.

- 6.4.5 CoolIT Systems Inc.

- 6.4.6 Fujitsu Ltd.

- 6.4.7 Kaori Heat Treatment Co., Ltd.

- 6.4.8 Lenovo Group Ltd.

- 6.4.9 LiquidStack Inc.

- 6.4.10 LiquidCool Solutions Inc.

- 6.4.11 Iceotope Technologies Ltd.

- 6.4.12 Rittal GmbH and Co. KG

- 6.4.13 Schneider Electric SE

- 6.4.14 Submer Technologies SL and Submer Inc.

- 6.4.15 Vertiv Group Corp.

- 6.4.16 Wiwynn Corporation

- 6.4.17 3M Company

- 6.4.18 Engineered Fluids Inc.

- 6.4.19 Green Revolution Cooling Inc.

- 6.4.20 Solvay SA

- 6.4.21 Mikros Technologies

- 6.4.22 Midas Green Technologies LLC

- 6.4.23 USystems Ltd. (Legrand Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment