PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937313

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937313

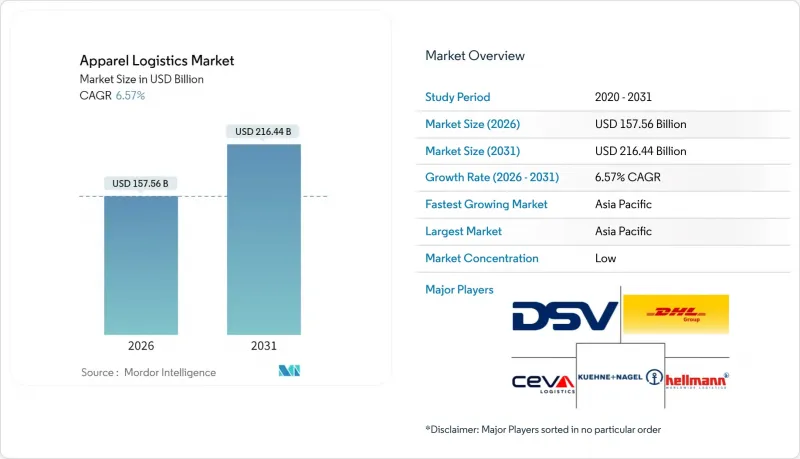

Apparel Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Apparel Logistics Market was valued at USD 147.85 billion in 2025 and estimated to grow from USD 157.56 billion in 2026 to reach USD 216.44 billion by 2031, at a CAGR of 6.57% during the forecast period (2026-2031).

As digitalization, circular-economy models, and stricter environmental rules reshape global fashion supply chains. Sustained e-commerce growth, on-demand delivery expectations, and SKU proliferation are compelling providers to invest in real-time inventory visibility tools and last-mile optimization. Asia-Pacific retains supremacy owing to its extensive production base, yet nearshoring in the Americas and Europe is gradually redirecting trade flows. Transportation services remain indispensable, accounting for 68% of 2024 revenue, while value-added services such as AI-enabled forecasting and resale support are expanding fastest at 4.10%. Competitive intensity is rising as 3PLs broaden offerings into reverse logistics to counter a 20.8% apparel return rate in the United States. Regulatory scrutiny of Scope-3 emissions and volatile freight rates further complicate cost structures, spurring accelerated investment in low-carbon fuels and automation.

Global Apparel Logistics Market Trends and Insights

2025+ Surge in On-Demand Apparel and Instant Delivery Expectations

Quick-commerce platforms are set to grow 75-85% annually in India, hitting USD 6 billion GMV by FY 2025, and similar momentum is visible across Southeast Asia. Logistics providers are re-engineering last-mile networks, with JD Logistics pledging 2-3-day cross-border delivery to dozens of markets in 2025. Peer-to-peer rental players such as By Rotation now run physical pick-up points to satisfy same-day demand. Municipal rules on delivery-vehicle emissions accelerate the shift to electric vans in dense cities. As brands test micro-fulfillment centers, real-time routing software becomes decisive in meeting two-hour delivery windows. Providers integrating predictive analytics have trimmed last-mile costs by 12% during 2024 pilots.

E-Commerce-Driven SKU Proliferation Requiring Sophisticated Inventory Visibility

Fashion brands juggle thousands of SKUs across multiple channels, rendering legacy systems obsolete. Walmart's AI trend-to-product engine converts social signals into purchase orders within weeks, slashing buffer stock. Retailers deploying AI-assisted demand planning report 30% faster inventory velocity. Excess stock remains acute, magnifying markdown pressure. EU Digital Product Passport requirements mandate granular item tracking by 2026, further tightening data needs. In response, 3PLs bundle control-tower platforms that synchronize ordering, fulfillment, and returns, positioning themselves as tech partners rather than freight brokers.

High Returns Rate Inflating Reverse-Logistics Costs

US retail returns totaled USD 890 billion in 2024, with apparel averaging a 20.8% rate and carrying costs 2.5X greater than outbound fulfillment. Serial returners in the United Kingdom create USD 8.6 billion equivalent in annual costs. AI-driven sortation systems from Happy Returns reduce processing time 70%. However, return fraud climbed to 15.14% in 2024, forcing the adoption of RFID and computer-vision authentication. Brands are piloting "keep-it" refunds for low-value items to minimize transport emissions and handling overhead, while resale partnerships convert returns into secondary-market inventory.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Regulations Pushing Green Logistics Investments

- AI-Driven Warehouse Automation Lowering Per-Unit Handling Costs

- Volatile Freight Rates and Capacity Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation generated 67.32% of 2025 revenue and anchors the apparel logistics market size at USD 99.52 billion. Road remains the backbone for intra-regional moves, while sea freight handles bulk international volumes; air retains a niche for high-value or time-critical stock. Adoption of alternative fuels is reshaping contract structures as shippers seek lower Scope-3 emissions. Despite its scale, transportation faces intensifying margin pressure from capacity volatility and carbon levies.

Value-added services posted the strongest 4.05% CAGR outlook, expanding the apparel logistics market by enabling kitting, labeling, repair, and recommerce tasks that once sat with brands. Providers like Ryder now bundle unpacking, sewing, and quality inspection within omnichannel fulfillment nodes. These functions embed logistics deeper into brand operations, driving stickier contracts and higher yields. Integration of point-of-sale data with warehouse management systems supports demand-driven packaging, while sustainability scoring modules attach carbon data to each parcel.

The Apparel Logistics Market Report is Segmented by Service (Transportation (Road, Rail, Air, Sea and Inland Waterways), Warehousing & Distribution Services, Value-Added Services), Product Type (Clothing, Footwear, Accessories), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 40.58% of 2025 revenue and anchors the apparel logistics market size at USD 59.99 billion, rising at 5.03% CAGR through 2031. China, Vietnam, Bangladesh, and India dominate exports, yet intra-Asian consumer spending strengthens regional distribution networks. RCEP trade preferences and port infrastructure upgrades in Indonesia and the Philippines shorten lead times. Sustainability regulations, such as China's dual-control energy targets, push factories to near ports, altering drayage patterns.

North America combines mature e-commerce operations with on-going automation investments. Labor shortages in California's Inland Empire and Pennsylvania's Lehigh Valley accelerate adoption of robotics, lowering per-unit handling costs. Mexico's nearshoring boom, especially along the Bajio corridor, re-positions cross-border trucking lanes and supports bi-national distribution centers. U.S. state incentives for hydrogen trucking complement federal IRA credits.

Europe emphasizes regulatory compliance, with CSRD and CBAM guiding modal shifts toward rail and inland waterways. Eastern European 3PLs expand capacity to serve rising fast-fashion production in Turkey and Morocco. Carbon pricing in the EU Emissions Trading System raises ocean-freight surcharges, prompting more consolidation at port warehouses to optimize container loads. E-commerce penetration in Germany, France, and the Nordics supports micro-fulfillment deployment inside urban low-emission zones.

List of Companies Covered in this Report:

- Ceva Logistics

- DSV

- Deutsche Post DHL Group

- Kuehne + Nagel

- Hellmann Worldwide Logistics

- Apparel Logistics Group Inc.

- PVS Fulfillment-Service GmbH

- Logwin AG

- GAC Group

- Nippon Express

- Genex Logistics

- Expeditors International of Washington Inc.

- BGROUP SRL

- FedEx Supply Chain

- GXO Logistics

- Bleckmann Logistics

- OIA Global

- XPO Logistics

- Lalamove

- JD Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 2025+ surge in on-demand apparel and instant delivery expectations

- 4.2.2 E-commerce-driven SKU proliferation requiring sophisticated inventory visibility

- 4.2.3 Sustainability regulations pushing green logistics investments

- 4.2.4 Expansion of near-market manufacturing in Americas and Europe

- 4.2.5 AI-driven warehouse automation lowering per-unit handling costs

- 4.2.6 Rise of apparel rental and recommerce models boosting reverse logistics

- 4.3 Market Restraints

- 4.3.1 High returns rate inflating reverse-logistics costs

- 4.3.2 Volatile freight rates and capacity constraints

- 4.3.3 Labor shortages in warehousing hotspots

- 4.3.4 Regulatory scrutiny of Scope-3 transport emissions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Government Regulations and Initiatives

- 4.9 Spotlight-Effect of E-commerce on Traditional Apparel Logistics Supply Chain

- 4.10 Review and Commentary on Reverse Logistics

- 4.11 Impact of COVID-19 and Geo-Political Events on the Market

5 Market Size and Growth Forecasts

- 5.1 By Service (Value)

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea and Inland Waterways

- 5.1.2 Warehousing and Distribution Services

- 5.1.3 Value-added Services

- 5.1.1 Transportation

- 5.2 By Product Type

- 5.2.1 Clothing

- 5.2.2 Footwear

- 5.2.3 Accessories

- 5.3 By Geography (Value)

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ceva Logistics

- 6.4.2 DSV

- 6.4.3 Deutsche Post DHL Group

- 6.4.4 Kuehne + Nagel

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Apparel Logistics Group Inc.

- 6.4.7 PVS Fulfillment-Service GmbH

- 6.4.8 Logwin AG

- 6.4.9 GAC Group

- 6.4.10 Nippon Express

- 6.4.11 Genex Logistics

- 6.4.12 Expeditors International of Washington Inc.

- 6.4.13 BGROUP SRL

- 6.4.14 FedEx Supply Chain

- 6.4.15 GXO Logistics

- 6.4.16 Bleckmann Logistics

- 6.4.17 OIA Global

- 6.4.18 XPO Logistics

- 6.4.19 Lalamove

- 6.4.20 JD Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment