PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937318

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937318

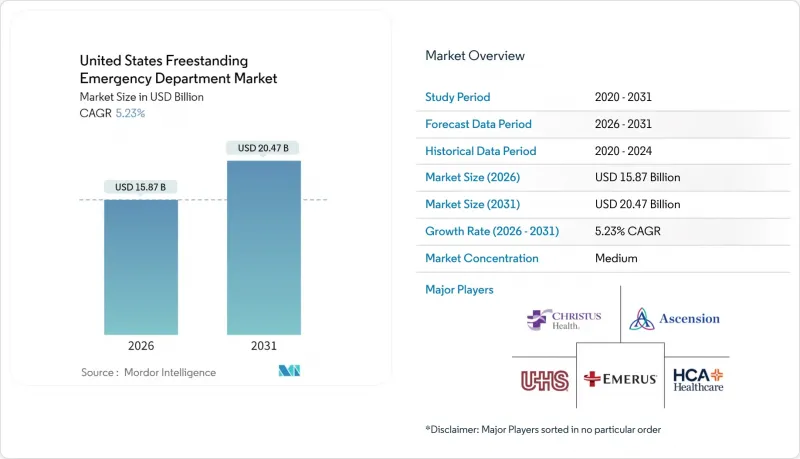

United States Freestanding Emergency Department - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Freestanding Emergency Department Market size in 2026 is estimated at USD 15.87 billion, growing from 2025 value of USD 15.08 billion with 2031 projections showing USD 20.47 billion, growing at 5.23% CAGR over 2026-2031.

This steady expansion reflects a structural shift in how emergency care is delivered, driven by migration into high-growth suburbs, state-level deregulation, and hospital strategies that favor capital-light outpatient footprints. Hospital systems deploy AI-enabled triage tools that shorten door-to-provider times, while independent operators move quickly into rural pockets where critical-access hospitals have closed. Population aging, the spread of high-deductible health plans, and federal New Access Points grants together deepen demand for proximate, lower-wait-time emergency services. Competitive positioning increasingly hinges on the ability to combine diagnostic imaging and laboratory services with emergency medicine staffing in facilities located near busy retail corridors.

United States Freestanding Emergency Department Market Trends and Insights

Consumer-Driven Health Plans & Federal Funding

Federal grant programs lower capital barriers and offset workforce shortages through loan-repayment incentives tied to medically underserved areas. The FY 2025 budget doubles community-health-center financing, positioning freestanding emergency departments as referral anchors that can absorb emergency demand for 37 million Americans. High-deductible plan enrollment pushes cost-conscious patients toward alternatives that promise shorter stays and transparent billing, reinforcing the role of these facilities as an intermediate choice between urgent care clinics and full-service hospital EDs. The Medicare Rural Hospital Flexibility Program further encourages development in counties that have lost critical-access hospitals, accelerating site approvals and stabilizing operator cash flow through supplemental payments.

Rising Preference for Convenience Care

Patient surveys show that door-to-provider times under 15 minutes strongly influence facility choice; freestanding emergency departments routinely meet this threshold, whereas hospital EDs average 45 minutes or more. Health-system acquisitions of urgent-care chains illustrate strategic alignment around convenience: HCA Healthcare acquired 41 Texas centers in 2025 to create feeder networks for nearby freestanding EDs. Facilities situated along commuter routes capture after-work traffic and divert non-life-threatening cases from congested hospital campuses. Hybrid facilities that combine urgent-care and emergency licensure allow on-site physicians to direct nearly 70% of visits to lower-acuity billing, improving patient affordability while preserving emergency capabilities.

High Overall Expenditure Per Visit

Commercial claims data show emergency-department encounters cost 4-5 times more than urgent-care visits, prompting insurers to steer non-emergent cases away from freestanding settings. Medicare's 2024 conversion-factor cut pushes marginal reimbursement down by 3.4%, forcing operators to optimize payer mix around privately insured patients. Hybrid centers mitigate the headwind by billing lower-acuity cases at urgent-care rates; nevertheless, price-sensitive self-pay patients remain cautious.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hospital Outpatient Strategies

- State-Level Regulatory Easing (CON Exemptions)

- Reimbursement & CMS Billing Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Off-campus emergency departments held a 58.02% United States freestanding emergency department market share in 2025, leveraging integrated electronic health records, favorable Medicare Part B billing, and hospital referral streams. Independent centers, though smaller in aggregate footprint, are projected to outpace at a 5.87% CAGR through 2031 as entrepreneurial groups exploit regulatory gaps in counties underserved by hospitals.

Hospital systems continue to treat off-campus units as strategic beachheads that deter competitors. HCA Florida's USD 70 million plan to open three new sites across Pasco, Hernando, and Citrus Counties exemplifies an asset-light expansion play that places branded emergency access within 10 miles of growing subdivisions. Independent operators counter by specializing in pediatric trauma or geriatric-friendly environments, differentiating on shorter triage queues and concierge-style amenities.

The United States Freestanding Emergency Department Market Report is Segmented by Ownership Type (Off-Campus Emergency Department, Independent), Service (Laboratory Service, Imaging Service, Emergency Care & Other Services), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AdventHealth

- Ardent Health

- Ascension

- Baptist Health South Florida

- Baylor Scott & White Health

- CHRISTUS Health

- CommonSpirit Health

- Community Health Systems

- Community Hospital Corp.

- Emerus Hospital Partners, LLC.

- Envision Healthcare

- HCA Healthcare

- Intuitive Health

- Lifepoint Health

- Northwell Health

- Sutter Health

- TeamHealth

- Tenet Healthcare

- Universal Health Services

- US Acute Care Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Consumer-Driven Health Plans & Federal Funding

- 4.2.2 Rising Preference for Convenience Care

- 4.2.3 Expansion of Hospital Outpatient Strategies

- 4.2.4 State-Level Regulatory Easing (CON Exemptions)

- 4.2.5 Hybrid ED/Urgent-Care Model Adoption

- 4.2.6 AI-Enabled Triage & Remote Monitoring Integration

- 4.3 Market Restraints

- 4.3.1 High Overall Expenditure Per Visit

- 4.3.2 Reimbursement & CMS Billing Uncertainty

- 4.3.3 Staffing Shortages & Wage Inflation

- 4.3.4 Price-Transparency Pressure on Facility Fees

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers / Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Ownership Type

- 5.1.1 Off-campus Emergency Department (OCED)

- 5.1.2 Independent

- 5.2 By Service

- 5.2.1 Laboratory Service

- 5.2.2 Imaging Service

- 5.2.3 Emergency Care & Other Services

- 5.3 By U.S. Census Region

- 5.3.1 Northeast

- 5.3.2 Midwest

- 5.3.3 South

- 5.3.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AdventHealth

- 6.3.2 Ardent Health

- 6.3.3 Ascension

- 6.3.4 Baptist Health South Florida

- 6.3.5 Baylor Scott & White Health

- 6.3.6 CHRISTUS Health

- 6.3.7 CommonSpirit Health

- 6.3.8 Community Health Systems

- 6.3.9 Community Hospital Corp.

- 6.3.10 Emerus Hospital Partners, LLC.

- 6.3.11 Envision Healthcare

- 6.3.12 HCA Healthcare

- 6.3.13 Intuitive Health

- 6.3.14 Lifepoint Health

- 6.3.15 Northwell Health

- 6.3.16 Sutter Health

- 6.3.17 TeamHealth

- 6.3.18 Tenet Healthcare

- 6.3.19 Universal Health Services, Inc.

- 6.3.20 US Acute Care Solutions

7 Market Opportunities & Future Outlook