PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937328

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937328

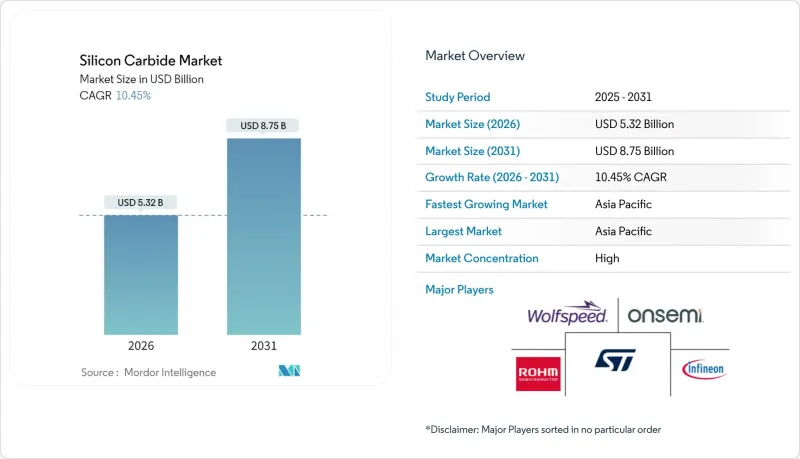

Silicon Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Silicon Carbide Market size in 2026 is estimated at USD 5.32 billion, growing from 2025 value of USD 4.82 billion with 2031 projections showing USD 8.75 billion, growing at 10.45% CAGR over 2026-2031.

Momentum originates from the shift to 200 mm wafers, first realized by Infineon in February 2025, which nearly doubles chip output per substrate and lowers unit costs. Demand gains are sharpened by electric-vehicle (EV) makers migrating to 800 V architectures, renewable-energy inverters seeking 98% efficiency, and data-center operators targeting 25-40% cooling cost cuts. Government incentives amplify growth: the U.S. CHIPS Act granted USD 750 million to Wolfspeed's North Carolina plant, while the European Chips Act allocated EUR 5 billion to STMicroelectronics' Italian fab, bolstering regional supply security. Asia-Pacific retains scale advantages, yet Western sovereignty initiatives are redrawing supply-chain maps even as quantum-photonic research opens new, non-power electronics horizons for the silicon carbide market.

Global Silicon Carbide Market Trends and Insights

Surging Demand from Power Electronics

Automotive OEMs transitioning to 800 V drivetrains now specify SiC MOSFETs capable of switching above 100 kHz, as shown by onsemi's EliteSiC M3e family that halves turn-off losses versus prior nodes. Infineon's 1200 V CoolSiC devices enable chargers operating beyond 900 V without extra insulation, accelerating EV platform adoption. Data-center operators report 25-40% cooling savings when SiC-based rectifiers lift conversion efficiency to 98%. Together, these use cases push wafer demand toward parity with silicon substrates by 2050. The silicon carbide market continues to broaden as industrial motor drives, rail traction, and server power supplies migrate to wide-band-gap solutions that outclass silicon IGBTs at high frequencies.

Increasing Utilization in Renewable Energy

Fraunhofer ISE's 3.3 kV SiC transistors deliver 98.4% efficient solar inverters that connect directly to medium-voltage grids, eliminating bulky transformers. Solar installations achieve 2% additional system efficiency and 70% lower energy losses versus silicon diodes, while wind turbines use SiC's thermal conductivity to handle 200 °C rotor-side temperatures without extra cooling. Bidirectional converters built on SiC underpin vehicle-to-grid schemes that stabilize networks during peak demand. European policy frameworks mandating distributed generation intensify pull for high-performance inverters, sustaining long-term momentum for the silicon carbide market.

Fluctuating Cost of Raw Materials

Wafer inputs form 55-70% of the SiC device cost. The energy-intensive Acheson route runs above 2,000 °C and consumes 10.5-13 kWh per kg, so power-price spikes feed straight into cash costs. Russian-Ukrainian supply disruptions tightened feedstock availability in 2024, while Chinese environmental curbs periodically idle 70% of global silicon metal output. Upsizing to 200 mm crystals demands fresh furnaces and CVD reactors, adding capital strain. Pilot recycling flows from Susteon promise 75% CO2 cuts and USD 10-20 per kg feedstock via methane pyrolysis, though commercialization sits years away.

Other drivers and restraints analyzed in the detailed report include:

- Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment

- Government Incentives for Wide-Bandgap fabs

- Availability of Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black SiC retained 41.56% of 2025 revenue due to its lower manufacturing costs and suitability for abrasives, refractories, and metallurgical additives. The silicon carbide market size for black grades benefits from large Acheson furnaces that achieve economies of scale. Green SiC, though smaller in volume, embodies the highest 13.05% CAGR as high-purity demand rises from power-device and quantum-photonic fabs. STMicroelectronics' switch to 200 mm green-SiC wafers in Norrkoping nearly doubles die output per slice, illustrating scale-up benefits.

Device makers pay premiums for green SiC because lower defect densities translate to higher chip yields and longer mean-time-to-failure in field service. As EV and renewable inverters proliferate, production learning curves are forecast to narrow the price gap versus black SiC, enlarging addressable revenue pools inside the silicon carbide market. Specialized metallurgical and ceramic variants serve petrochemical, aerospace, and defense niches that value oxidation resistance and thermal shock stability, supporting a robust product spectrum that cushions suppliers against single-segment volatility.

The Silicon Carbide Report is Segmented by Product Type (Black Silicon Carbide, Green Silicon Carbide, and Other Products), Application (Steel Manufacturing, Energy, Automotive, Aerospace and Defense, Electronics and Semiconductors, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 52.12% of global revenue in 2025 and expands at a 11.96% CAGR, sustained by 28 active Chinese wafer projects spanning Guangdong Tianyu Semiconductor and Hantian Technology. South Korean IDMs add SiC process nodes to serve Hyundai and Kia, while Taiwan's foundry cluster offers flexible capacity to fabless chipmakers. India entered the silicon carbide market when RIR Power Electronics invested USD 620 million in Odisha, building the country's first dedicated line.

North America benefits from USD 52.7 billion in CHIPS Act incentives that cover everything from crystal growth to module assembly. Wolfspeed's North Carolina site will be the world's largest SiC materials facility, and Bosch's California fab readies 200 mm wafers for 2026 automotive programs. Tesla and GM anchor regional demand while Canada supplies high-purity quartz feedstock and Mexico evolves assembly clusters.

Europe advances through a EUR 43 billion (~USD 50.23 billion) Chips Act aimed at doubling the continental semiconductor share by 2030. Infineon augments Austrian front-end output with Malaysian back-end lines for cost efficiency, while Volkswagen, BMW, and Stellantis lock multi-year offtake contracts. Smaller Middle East and African markets import SiC devices for utility-scale solar farms and petrochemical heaters, relying on European and Asian OEMs for supply.

- Blasch Precision Ceramics, Inc.

- Christy Refactories

- CoorsTek Inc.

- CUMI EMD.

- Elkem ASA

- ESD-SIC

- Imerys

- Infineon Technologies AG

- Kymera International

- Morgan Advanced Materials

- Navarro SiC

- NGK INSULATORS, LTD.

- ROHM Co., Ltd.

- Saint-Gobain

- Schunk Ingenieurkeramik

- Semiconductor Components Industries, LLC

- Semiconductor Components Industries, LLC (onsemi)

- STMicroelectronics

- Tateho Chemical

- Washington Mills

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand from Power-Electronics

- 4.2.2 Incresing Utilization in Renewable Energy

- 4.2.3 Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment

- 4.2.4 Government incentives for wide-band-gap fabs

- 4.2.5 Growing Usage in Aerospace and Defence Industry

- 4.3 Market Restraints

- 4.3.1 Fluctuating Cost of Raw Materials

- 4.3.2 Availability of Substitues

- 4.3.3 Tight particulate-emission norms for SiC grinding plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Black Silicon Carbide

- 5.1.2 Green Silicon Carbide

- 5.1.3 Other Products (Metallurgical-grade SiC, etc.)

- 5.2 By Application

- 5.2.1 Steel Manufacturing

- 5.2.2 Energy

- 5.2.3 Automotive

- 5.2.4 Aerospace and Defense

- 5.2.5 Electronics and Semiconductors

- 5.2.6 Other Applications (Industrial Manufacturing, Abrasives and Ceramics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Indonesia

- 5.3.1.7 Vietnam

- 5.3.1.8 Malaysia

- 5.3.1.9 Philippines

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Blasch Precision Ceramics, Inc.

- 6.4.2 Christy Refactories

- 6.4.3 CoorsTek Inc.

- 6.4.4 CUMI EMD.

- 6.4.5 Elkem ASA

- 6.4.6 ESD-SIC

- 6.4.7 Imerys

- 6.4.8 Infineon Technologies AG

- 6.4.9 Kymera International

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Navarro SiC

- 6.4.12 NGK INSULATORS, LTD.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Saint-Gobain

- 6.4.15 Schunk Ingenieurkeramik

- 6.4.16 Semiconductor Components Industries, LLC

- 6.4.17 Semiconductor Components Industries, LLC (onsemi)

- 6.4.18 STMicroelectronics

- 6.4.19 Tateho Chemical

- 6.4.20 Washington Mills

- 6.4.21 Wolfspeed, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growing Innovation in High Frequency and Quantum Tech Applications