PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937329

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937329

Decorative Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

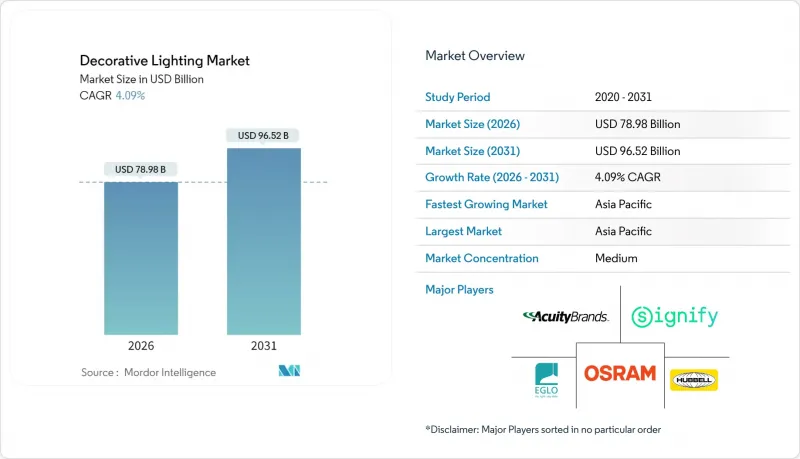

The decorative lighting market was valued at USD 75.88 billion in 2025 and estimated to grow from USD 78.98 billion in 2026 to reach USD 96.52 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

LED cost erosion, rising smart-home adoption, and a sustained renovation boom jointly underpin this steady expansion. As voice-enabled ecosystems normalize, manufacturers pivot from isolated aesthetic pieces toward fixtures that natively support Matter and Thread, thereby converting lighting into a functional node within a larger residential or commercial IoT stack. Production networks are re-balancing after 104% U.S. tariffs on Chinese imports; firms that lock in multi-country sourcing and copper hedges buffer cost shocks while maintaining delivery reliability. Cordless rechargeable lamps, uniform-emission OLED panels, and solar-hybrid garden lanterns broaden consumer choice, while designers rely on human-centric light profiles that shift hue to boost wellness in workplaces and hospitality venues. Sustainability imperatives-especially Europe's circular-economy mandates-favor brands that document recyclability, publish Environmental Product Declarations, and engineer fixtures for disassembly.

Global Decorative Lighting Market Trends and Insights

Rapid LED Price Erosion & Efficiency Gains

LED component prices slid below USD 0.12 per watt in 2025, letting decorative fixtures deliver 75% energy savings and 50,000-hour lifespans that recast total ownership calculations. As CRI values exceed 90, hospitality brands no longer trade color warmth for efficiency, accelerating replacement cycles across lobbies, restaurants, and guest rooms. Residential adopters migrate from incandescent ambience toward filament-style LEDs that keep vintage aesthetics yet halve power draw. Simultaneously, miniaturized heat sinks unlock sculptural designs once infeasible with bulkier lamp bodies. These economics redirect R&D toward optics that modulate beam spread, empowering designers to layer accent and task lighting without perceptible hotspots.

Smart-Home Platform Integration (Matter, Thread)

Matter certification now ensures a single decorative pendant can sync with Amazon, Google, and Apple hubs, sparing retailers from SKU proliferation. The thread's low-power mesh solves coverage gaps in masonry-heavy dwellings, enabling cordless bedside sconces to respond reliably to voice commands. Facility managers insist on Matter-ready chandeliers so maintenance staff can troubleshoot remotely rather than accessing high-ceiling installations. Hotels deploy centralized dashboards that change lobby ambience from daylight to evening warmth at a touch, fortifying brand experience consistently chain-wide. As integrators standardize open protocols, procurement teams weigh longevity and cybersecurity certifications alongside style.

Supply-Chain Volatility for Decorative Glass & Metals

The imposition of tariffs on Chinese fixtures has substantially increased landed costs, compelling niche brands with limited supplier networks to explore alternative sourcing options. While Vietnam and Mexico have absorbed some of the demand, the availability of furnaces designed for thick artisan glass remains limited, leading to extended lead times that conflict with the fast-evolving decor market. Additionally, copper prices, which have been fluctuating above USD 5.00 per pound, are exacerbating cost pressures for pendant manufacturers reliant on spun brass housings. Larger, diversified players are mitigating these challenges by employing hedging strategies and adopting modular designs that facilitate material substitution, such as replacing brass with steel, without requiring significant retooling. Conversely, smaller ateliers are deferring product launches or reducing collection sizes to preserve cash flow. These dynamics highlight the operational and financial pressures faced by industry participants amid shifting market conditions.

Other drivers and restraints analyzed in the detailed report include:

- DIY Interior-Upgrade Boom Post-COVID

- E-commerce Visualization Tools (AR/VR)

- Counterfeit Low-Quality Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling lights and chandeliers accounted for USD 26.58 billion of 2025 revenue, representing 35.02% of the decorative lighting market size. Their dominance stems from new-build construction and renovation priorities that allocate budget to a central "statement" piece anchoring living or lobby spaces. Project designers exploit LED filament bulbs and translucent acrylic diffusers to craft voluminous forms that weigh less than legacy crystal models, easing installation on gypsum ceilings. At the same time, manufacturers integrate Matter-ready drivers so owners can adjust color temperature from warm-white dinners to cool-white task settings via voice assistants. Entry-level builders adopt pre-wired canopies that accelerate fit-out schedules, reducing job-site labor. Luxury homeowners commission bespoke chandeliers from Czech and Murano studios that ship modular sections for on-site assembly, demonstrating how artisan glass survives by aligning with smart drivers and precision-cut aluminum frames.

Table and floor lamps, valued at USD 11.93 billion in 2025, deliver the fastest 5.21% CAGR through 2031, catalyzed by lithium-battery density improvements that enable 15-hour cordless operation. As flexible working blurs room functions, consumers reposition lamps between desks, sofas, and terraces without trailing cords. Brands emphasize USB-C charging and Qi wireless pads in bases, converting lamps into multi-utility hubs that power phones and earbuds. Retail assortments skew toward mid-century silhouettes in matte-brass finishes, verified by AR app analytics that flag user placement preferences for sideboards and bedside tables. Meanwhile, wall sconces integrate PIR sensors to automate hallways and powder rooms, seeding cross-sales of matching mirrors with embedded perimeter lighting. Track lighting rounds out the product hierarchy with modular magnetic heads that snap onto ceiling rails, letting retailers market starter kits bundled with accent spot modules and wash lenses for gallery-style residential displays.

LED technology secured 70.12% of the decorative lighting market share in 2025 as filament-style bulbs replicate the incandescent glow while delivering 110 lm/W efficiencies. Manufacturers pursue segmented optics that combine narrow beam accent modules with diffuse backlights inside a single chandelier, showcasing LED versatility. Utility rebate sunsets after 2026 shift conversation from payback to wellness, positioning tunable-white LEDs at premium price points. Simultaneously, OLED panels and solar-hybrid engines together logged USD 2.53 billion in 2025 revenue, advancing at a 4.88% CAGR. Paper-thin OLED sheets enable wall art that doubles as mood lighting, selling through design-forward boutiques in Tokyo and Berlin. Solar garden lanterns leap to 1,800 lumen outputs courtesy of higher-efficiency mono-crystalline panels and LiFePO4 batteries that cycle 3,000+ times.

Incandescent and halogen categories shrink below 5% of the decorative lighting market size as regulatory bans tighten. Yet boutique hospitality designers still specify 2,400 K filament bulbs in speakeasy bars, citing warm nostalgia unsatisfied by some LED replicas. Fluorescent and CFL units fade under harsh color critique, redirecting retrofit demand squarely into LED tubes or integrated drivers. Looking forward, R&D invests in micro-LED arrays that promise OLED-like surface emission but longer lifespans, foreshadowing another leap in design freedom.

The Global Decorative Lighting Market Report is Segmented by Product Type (Ceiling Lights & Chandeliers, Pendants, Wall Sconces, and More), Light Source (LED, Incandescent, Fluorescent & CFL, Halogen, Others), End-User (Residential, Commercial), Distribution Channel (B2C/Retail Channels, B2B/Direct Sales & Projects), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated USD 27.09 billion in 2025, translating to 35.70% of global value and the fastest 5.98% CAGR through 2031. China's export clusters in Guangdong continue to dominate glass shade and die-cast housing output even as domestic consumption climbs with urban condominium completions. India's modular switch segment, growing at 7.99% CAGR, signals broader electrification that dovetails with decorative fixture upgrades. Singapore, Malaysia, and Thailand incentivize smart LED retrofits in hospitality corridors to hit energy-intensity targets, sustaining demand for networkable sconces. Japan tilts toward premium OLED wall art addressing space constraints in micro-apartments, while Australia's home-renovation wave fuels sales of coastal-proof outdoor pendants powder-coated against salt spray.

North America displays replacement-driven dynamics underpinned by robust housing equity and wide smart-speaker penetration. Matter interoperability gains particular traction as homeowners declutter apps, preferring one voice command to operate chandeliers, recessed cans, and accent lanterns. Commercial retrofits install human-centric lobby lighting aimed at enticing employees back in hybrid work patterns, while supply-chain reshoring steers retailers toward Mexican metallic housing suppliers that skirt tariffs.

Europe foregrounds sustainability, requiring EPD documentation for public tenders and favoring fixtures engineered for disassembly. Germany's Bauhaus-inspired armature lamps in recycled aluminum resonate with eco-savvy consumers, whereas Italy merges heritage Murano glass with dim-to-warm LED filaments. The Netherlands pilots circular-leasing contracts where hotels return pendants after five years for refurbish-and-reuse cycles, embedding circularity into brand narratives. Brexit complexities continue to challenge U.K. import flows, prompting local warehouses to buffer lead times.

Latin America and the Middle East, though smaller in revenue share, record above-average growth courtesy of hospitality megaprojects. Saudi Arabia's entertainment districts specify large-scale kinetic chandeliers with programmable RGBW nodes, pushing local integrators to upskill in DMX programming. Brazilian resort operators favor solar-hybrid garden lanterns that cut trenching costs in remote beach properties.

- Acuity Brands Lighting

- Artemide S.p.A.

- Cree Lighting

- Eglo Leuchten GmbH

- FLOS S.p.A.

- Foscarini S.r.l.

- General Electric Co.

- Havells India Ltd

- Hubbell Incorporated

- Jaquar Lighting

- Kichler Lighting LLC

- Lamps Plus

- Lutron Electronics Co., Inc.

- Nora Lighting

- Opple Lighting

- Osram Licht AG

- Signify (Philips Lighting)

- Vibia Lighting

- WAC Lighting

- Xiaomi (Yeelight)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED price erosion & efficiency gains

- 4.2.2 Smart-home platform integration (Matter, Thread)

- 4.2.3 DIY interior-upgrade boom post-COVID

- 4.2.4 E-commerce visualisation tools (AR/VR)

- 4.2.5 Government incentives for energy-efficient lighting

- 4.2.6 Rising disposable income driving premium decor spend

- 4.3 Market Restraints

- 4.3.1 Supply-chain volatility for decorative glass & metals

- 4.3.2 Price sensitivity in mass-market residential buyers

- 4.3.3 High upfront cost of connected/smart luminaires

- 4.3.4 Proliferation of counterfeit low-quality products

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Ceiling Lights & Chandeliers

- 5.1.2 Pendants

- 5.1.3 Wall Sconces

- 5.1.4 Table & Floor Lamps

- 5.1.5 Track Lights

- 5.1.6 Other Product Types

- 5.2 By Light Source

- 5.2.1 LED

- 5.2.2 Incandescent

- 5.2.3 Fluorescent & CFL

- 5.2.4 Halogen

- 5.2.5 Others (OLED, Solar, etc.)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Hypermarkets and Supermarkets

- 5.4.1.2 Home Centers

- 5.4.1.3 Specialty Lighting Stores

- 5.4.1.4 Online

- 5.4.1.5 Other Distribution Channels

- 5.4.2 B2B/Direct Sales & Projects

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Acuity Brands Lighting

- 6.4.2 Artemide S.p.A.

- 6.4.3 Cree Lighting

- 6.4.4 Eglo Leuchten GmbH

- 6.4.5 FLOS S.p.A.

- 6.4.6 Foscarini S.r.l.

- 6.4.7 General Electric Co.

- 6.4.8 Havells India Ltd

- 6.4.9 Hubbell Incorporated

- 6.4.10 Jaquar Lighting

- 6.4.11 Kichler Lighting LLC

- 6.4.12 Lamps Plus

- 6.4.13 Lutron Electronics Co., Inc.

- 6.4.14 Nora Lighting

- 6.4.15 Opple Lighting

- 6.4.16 Osram Licht AG

- 6.4.17 Signify (Philips Lighting)

- 6.4.18 Vibia Lighting

- 6.4.19 WAC Lighting

- 6.4.20 Xiaomi (Yeelight)

7 Market Opportunities & Future Outlook

- 7.1 LED Innovation Enhancing Energy Efficiency Appeal

- 7.2 Customizable Fixtures Catering to Personal Lifestyles

- 7.3 Premium Aesthetics Influencing High-End Adoption