PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937339

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937339

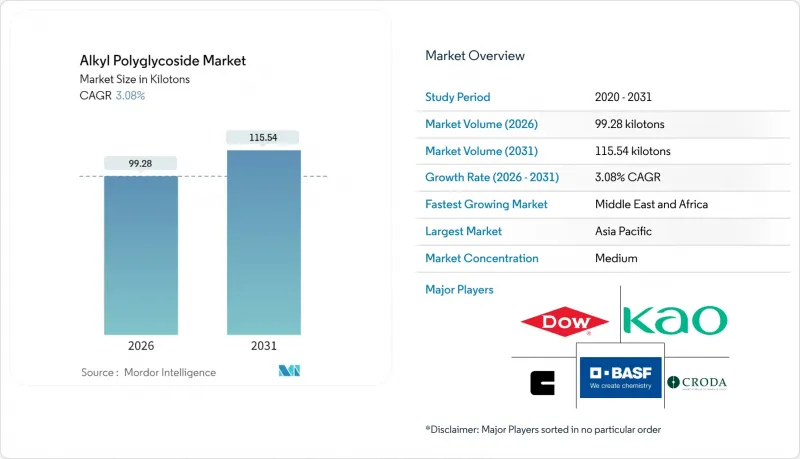

Alkyl Polyglycoside - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Alkyl Polyglycoside market size in 2026 is estimated at 99.28 kilotons, growing from 2025 value of 96.31 kilotons with 2031 projections showing 115.54 kilotons, growing at 3.08% CAGR over 2026-2031.

Demand is driven by regulatory phase-outs of hazardous non-ionic surfactants, rapid shifts in formulation toward bio-based ingredients, and steady capacity additions that stabilize the raw-material supply. Home-care and personal-care producers increasingly specify Alkyl polyglucoside surfactants to align with ecolabel criteria, while oil-field service companies adopt APG hydrotropes to meet environmental discharge limits. Asian manufacturers capitalize on their proximity to palm- and coconut-based fatty alcohols to secure export contracts, whereas European suppliers leverage sustainability branding to achieve premium positioning. Despite feedstock price fluctuations and competition from betaines and amino oxides, cost curves continue to improve as integrated chemical majors scale up production and share process expertise.

Global Alkyl Polyglycoside Market Trends and Insights

Growing Demand for Bio-Based Surfactants in Home and Personal-Care Formulations

Brand owners reposition product portfolios around non-sulfate, plant-derived ingredients to secure ecolabel certifications and capture premium shelf space. Volume commitments from multinational fast-moving consumer goods companies create forward visibility, encouraging suppliers to expand capacity and refine grades tailored to rinse-off and leave-on products. Formulators favor Alkyl polyglucoside surfactants for mildness, low irritation, and synergy with enzymes, enabling sulfate-free laundry detergents that still deliver high soil removal. Digital-savvy consumers scrutinize ingredient lists, pushing retailers to stock finished goods containing recognizable sugar-based surfactants. Asian contract manufacturers respond with turnkey offerings that integrate APGs, shortening innovation lead times for global private-label retailers.

Regulatory Phase-Out of Nonyl-Phenol Ethoxylates and Other Hazardous Surfactants

The European Chemicals Agency banned NPEs in most applications, triggering accelerated substitution programs that ripple across global supply chains. US TSCA risk evaluations and state-level initiatives mirror Europe's stance, compressing customer timelines to validate alternatives. Alkyl polyglucoside surfactants fulfill performance specifications without secondary alcohol ethoxylate residues, easing dossier preparation and reducing downstream disposal liabilities. Procurement teams cite lower compliance costs when transitioning to APGs versus maintaining NPE-based inventories under derogation clauses. The clear direction of policy lowers perceived technology risk, making APGs the default non-ionic replacement in institutional cleaning and textile processing.

Volatility in Natural Fatty-Alcohol and Starch Feedstock Prices

Fatty-alcohol costs represent roughly 65% of Alkyl polyglucoside variable expenses, leaving producers vulnerable to commodity swings tied to bio-diesel mandates and weather-linked harvest cycles. After dropping to USD 1,467 per ton in 2023, C12-C14 alcohols rebounded by more than 30% in 2024 due to El Nino-related palm-oil yield reductions. Spot spikes force quarterly price resets that unsettle detergent formulators operating under fixed retail contracts. Some APG suppliers hedge their risks with long-term plantation agreements; however, drought, labor shortages, and phytosanitary restrictions can still curtail deliveries. Investors weigh these uncertainties when allocating capital to greenfield APG plants, which can occasionally result in lengthened project gestation periods.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions and Backward Integration of Fatty-Alcohol Suppliers

- Rising Adoption of APG Hydrotropes in Alkaline Industrial Cleaning and Oil-Field Fluids

- Availability of Alternative Mild Surfactants (e.g., Betaines, Amino-Oxides)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fatty alcohol-based grades captured 42.10% of 2025 volume, underscoring decades of scale efficiencies and readily available lauryl alcohol streams from detergent-alcohol crackers. Their process familiarity assures consistent color, odor, and degree of polymerization, features critical to mass-market detergent concentrates. Vegetable-oil-derived variants exhibit the highest 3.55% CAGR, as continuous transesterification and enzymatic synthesis technologies enable shorter cycle times and lower carbon intensity. The Alkyl polyglucoside market size associated with vegetable-oil pathways is projected to expand from 27.54 kilotons in 2025 to 33.92 kilotons by 2031, reflecting rapid feedstock diversification among ASEAN and South American biodiesel clusters.

Up-and-coming sugar- and corn-starch-based APGs service niche personal-care lines that command double-digit gross margins, compensating for immature supply chains and higher unit costs. Meanwhile, fatty-alcohol producers refine impinging-stream reactors that reduce the alcohol-to-glucose molar ratio below 3:1, slicing raw-material inputs by 5% and enhancing yield. Suppliers pair these process strides with blockchain-enabled traceability modules that map the origins of plantations, satisfying traceability mandates from European retailers. As vegetable-oil technologies scale, price differentials versus fatty-alcohol routes narrow, inviting co-investment strategies that blur traditional segment boundaries.

The Alkyl Polyglucoside Market Report is Segmented by Product Type (Fatty Alcohol, Sugar, Corn-Starch, Vegetable Oil, and Other Product Type), Application (Personal Care and Cosmetics, Home-Care Products, Industrial Cleaners, Agricultural Chemicals, and Other Application), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region retained 45.90% of the global volume in 2025, driven by integrated petrochemical complexes in China and the proximity of palm oil in Southeast Asia. Provincial tax incentives encourage investment in sulfosuccinate, APG, and betaine lines, fostering a competitive manufacturing cluster around Ningbo and Shanghai. India's beauty and personal care sector, valued at USD 20 billion for 2025, amplifies domestic APG pull-through as sulfate-free shampoos penetrate Tier-II cities. Thailand and Malaysia consolidate their role as fatty-alcohol feedstock hubs, supplying Bangpakong and Kuantan sites that dispatch bulk APG to Japanese OEMs.

The Middle East and Africa are projected to post the fastest 3.52% CAGR through 2031, albeit from a smaller base, as national oil companies seek environmentally compatible additives for enhanced-oil-recovery pilot wells. Saudi downstream initiatives in Jubail include pilot APG units adjacent to ethoxylate trains, enabling surfactant blending within a single logistical zone. South African formulators of institutional cleaners adopt locally blended APG concentrates to meet supermarket private-label sustainability scorecards. Regional governments use green-procurement policies to prioritize bio-based surfactants for municipal cleaning contracts, building steady baseline demand.

North American and European volumes grow at modest single-digit rates underpinned by aggressive NPE withdrawal schedules and voluntary retailer chemical watch lists. Pilot Chemical's exclusive license to manufacture Bio IOS technology in Ohio from 2026 signals fresh capital injection into U.S. bio-based surfactants. European premium segments feature APG blends with amino-oxides to balance cost and foaming, while California formulators lean on APG to comply with Safer Consumer Products regulations. South America trails in absolute volume but registers momentum in crop-protection adjuvants, leveraging APG's low phytotoxicity to penetrate glyphosate replacement formulations.

- BASF

- Brillachem

- Clariant

- Croda International plc

- Dow

- Evonik Industries

- FENCHEM

- Galaxy Surfactants

- Kao Corporation

- Pilot Chemical Corp.

- Seppic (Arkema Group)

- Shanghai Chenhua International Trade Co., Ltd.

- Shanghai Fine Chemical Co., Ltd.

- Shanghai Sunwise Chemical Co., Ltd

- Silver Fern Chemical LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for bio-based surfactants in home and personal-care formulations

- 4.2.2 Regulatory phase-out of nonyl-phenol ethoxylates (NPEs) and other hazardous surfactants

- 4.2.3 Capacity additions and backward integration of fatty-alcohol suppliers

- 4.2.4 Rising adoption of APG hydrotropes in alkaline industrial cleaning and oil-field fluids

- 4.2.5 Cost-cutting high-gravity impinging-stream reactors enabling <3:1 alcohol-to-glucose ratios

- 4.3 Market Restraints

- 4.3.1 Volatility in natural fatty-alcohol and starch feedstock prices

- 4.3.2 Availability of alternative mild surfactants (e.g., betaines, amino-oxides)

- 4.3.3 Stringent RSPO/deforestation-free palm supply audits tightening raw-material access

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Fatty Alcohol

- 5.1.2 Sugar

- 5.1.3 Corn-starch

- 5.1.4 Vegetable Oil

- 5.1.5 Other Product Type

- 5.2 By Application

- 5.2.1 Personal Care and Cosmetics

- 5.2.2 Home-care Products

- 5.2.3 Industrial Cleaners

- 5.2.4 Agricultural Chemicals

- 5.2.5 Other Application

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Brillachem

- 6.4.3 Clariant

- 6.4.4 Croda International plc

- 6.4.5 Dow

- 6.4.6 Evonik Industries

- 6.4.7 FENCHEM

- 6.4.8 Galaxy Surfactants

- 6.4.9 Kao Corporation

- 6.4.10 Pilot Chemical Corp.

- 6.4.11 Seppic (Arkema Group)

- 6.4.12 Shanghai Chenhua International Trade Co., Ltd.

- 6.4.13 Shanghai Fine Chemical Co., Ltd.

- 6.4.14 Shanghai Sunwise Chemical Co., Ltd

- 6.4.15 Silver Fern Chemical LLC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment