PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937350

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937350

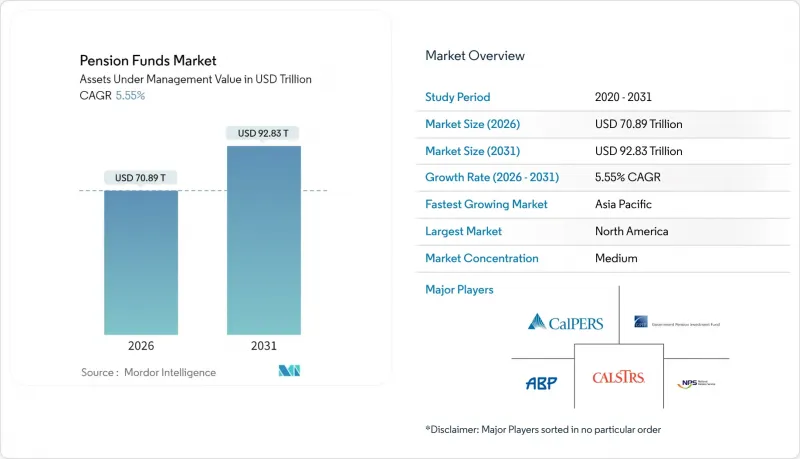

Pension Funds - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Pension funds market size in 2026 is estimated at USD 70.89 trillion, growing from 2025 value of USD 67.16 trillion with 2031 projections showing USD 92.83 trillion, growing at 5.55% CAGR over 2026-2031.

Gains rest on the decisive global swing from defined benefit (DB) to defined contribution (DC) plans, intensifying regulatory nudges that raise participation and contributions, and steady inflows from ageing workforces seeking secure post-retirement income. Asset-allocation patterns continue to migrate toward equities, infrastructure, and other private-market classes as funds search for yield while contending with low-rate backdrops. Meanwhile, digital tools that automate administration, enable member self-service, and lower back-office costs are allowing even mid-sized plans to replicate the scale advantages once enjoyed only by the largest sponsors. Competitive positioning is shifting from pure asset heft to a blend of cyber-secure operations, data-rich risk management, and credible climate strategies that help trustees meet fiduciary and societal expectations.

Global Pension Funds Market Trends and Insights

Shift from DB to DC Schemes

Defined contribution plans already hold the majority of global pension savings, and their 6.45% growth rate underscores the systemic reallocation of investment risk from employers to employees. The United Kingdom, the Netherlands, and Germany all enacted pivotal reforms that accelerate DC take-up, compelling sponsors to modernize member portals and adopt robo-advice so individuals can manage personalized glide paths. Asset managers benefit from rising flows into target-date funds, while administrators deploy cloud processing to cut record-keeping costs and enable same-day investment of contributions. Collectively, these moves recalibrate fee structures, shorten settlement cycles, and heighten demand for real-time analytics that guide participants toward adequate retirement outcomes.

Ageing Population & Longevity Risk

Longer life expectancy lifts pension liabilities, prompting funds to recalibrate strategic asset mixes away from low-yield government bonds toward global equities, real estate, and infrastructure. Japan's allocation pivot amplified listed-equity exposure and added nearly USD 280 billion of net gains in fiscal 2024. South Korea and China now study similar equity weightings as buffers against future benefit obligations. Longevity-linked securities, annuity buy-ins, and bespoke reinsurance solutions are rising as sponsors seek cost-effective hedges against payouts that stretch well beyond actuarial projections. These innovations spur demand for granular mortality data and analytics that can refine liability duration and hedge effectiveness.

Prolonged Low-Yield Environment

Real yields that remain below assumed returns compress funding ratios and intensify the need for risk assets. U.S. public plans that previously experienced significant returns later faced notable declines, exposing volatility that challenges board risk tolerance. Trustees respond by lengthening duration through private credit, yet must reconcile liquidity constraints with unpredictable benefit-payment schedules. Liability-driven investing mandates expand, and overlays that hedge interest-rate risk receive renewed attention. The environment elevates pressure on fee budgets and underlines the importance of integrated asset-liability modeling tools capable of stress-testing dozens of economic scenarios.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Auto-Enrolment & Higher Contributions

- Diversification into Alternative Assets

- DB Plan Under-Funding Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Defined contribution structures captured 56.85% of the global pension funds market in 2025 and are projected to widen their lead at 6.32% CAGR to 2031. Mandatory auto-enrollment rules in major economies funnel fresh payroll inflows, lifting the pension funds market size for DC accounts to more than USD 52.4 trillion by 2031 . Member-directed investment platforms integrate gamified retirement calculators and ESG filters, enhancing engagement while supplying administrators with anonymized behavioral data that bolsters predictive deferral models.

The legacy DB segment still commands sizable pools, but recurring under-funding and volatility accelerate de-risking. Hybrid formats ranging from collective DC in the United Kingdom to wage-linked plans in Germany seek a middle ground, while India's civil-service hybrid illustrates global experimentation. For insurers, a vibrant market for buy-ins and longevity swaps emerges, supporting scalable hedging products linked to standardized mortality tables.

Active mandates accounted for 54.35% of the global pension funds market in 2025, though fee compression and transparency demands are expected to lift passive uptake at 6.02% CAGR. Index-tracking products now embed ESG screens and fractionally integrate smart-beta tilts, allowing trustees to satisfy stewardship codes without incurring full-service active fees. The pension funds market size allocated to passive equity is expected to grow significantly in the coming years, yet boards still reserve carve-outs for high-conviction active approaches in less-liquid arenas such as global small caps and emerging-market debt.

Blended or "hyper-managed" solutions gain traction, fusing passive building blocks with dynamic overlays that harvest factor-based alpha within tightly controlled tracking-error budgets. Artificial-intelligence tools that mine unstructured data for macro sentiment support real-time rebalancing, cutting decision cycles from weeks to hours. Custodians and middleware vendors expand data pipes to feed these engines, creating fertile revenue niches well beyond traditional safekeeping.

The Global Pension Funds Market is Segmented by Plan Type (Defined Contribution (DC), Defined Benefit (DB), and Hybrid and Others), by Investment Strategy (Active, and Passive), by Sponsor Type (Public-Sector Plans, and Private-Sector Plans), by Geography of Investment (Onshore and Offshore), and by Region (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 70.65% share mirrors deep capital markets, tax-advantaged account frameworks, and widely adopted auto-enrolment. Yet public-plan liabilities press sponsors to explore risk-transfer packages, while technology-driven robo-advice reshapes member engagement. The SECURE 2.0 Act broadens coverage through mandatory enrollment and bigger catch-up ceilings, and Canadian funds sustain peer-leading returns via in-house asset teams that pursue direct private deals.

Asia-Pacific remains the fastest-growing region: GPIF's governance model influences peers, India's universal-pension initiatives extend coverage, and China's phased retirement-age uplift places structural support under funded assets. South Korea's National Pension Service continues to weigh parametric contributions, and Australia's superannuation rate rises to 12% in 2025.

Europe balances demographic headwinds with reform zeal. Germany's new EUR 200 billion equity-focused fund underpins its push toward market-based financing, the Netherlands implements its landmark DC shift, and the United Kingdom's megafund consolidation aims to unlock GBP 80 billion for infrastructure. France's public sector scheme ERAFP refines tactical asset allocation amid volatility while maintaining long-term ESG commitments.

List of Companies Covered in this Report:

- CalSTRS (US)

- Government Pension Investment Fund (Japan)

- National Pension Service (South Korea)

- ABP (Netherlands)

- California Public Employees' Retirement System (CalPERS)

- Canada Pension Plan Investment Board (CPPIB)

- AustralianSuper

- PFZW (Netherlands)

- USS (Universities Superannuation Scheme, UK)

- Afore XXI Banorte (Mexico)

- National Electrical Benefit Fund

- Caisse des Depots (France)

- ATP (Denmark)

- Federal Retirement Thrift Investment Board

- Ontario Teachers' Pension Plan

- Alecta (Sweden)

- UniSuper (Australia)

- APG (Netherlands)

- Public Institute for Social Security (Kuwait)

- General Organization for Social Insurance (GOSI, Saudi Arabia)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift from DB to DC schemes

- 4.2.2 Ageing population & longevity risk

- 4.2.3 Regulatory push for auto-enrolment & higher contributions

- 4.2.4 Diversification into alternative assets

- 4.2.5 Tokenization enabling fractional real-asset access

- 4.2.6 Climate-aligned infrastructure investment demand

- 4.3 Market Restraints

- 4.3.1 Prolonged low-yield environment

- 4.3.2 DB plan under-funding gaps

- 4.3.3 Domestic investment mandates politicising capital

- 4.3.4 Rising cyber-security & data-breach exposures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Plan Type

- 5.1.1 Defined Contribution (DC)

- 5.1.2 Defined Benefit (DB)

- 5.1.3 Hybrid and Others

- 5.2 By Investment Strategy

- 5.2.1 Active

- 5.2.2 Passive

- 5.3 By Sponsor Type

- 5.3.1 Public-Sector Plans

- 5.3.2 Private-Sector Plans

- 5.4 By Geography of Investment

- 5.4.1 Onshore

- 5.4.2 Offshore

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 CalSTRS (US)

- 6.4.2 Government Pension Investment Fund (Japan)

- 6.4.3 National Pension Service (South Korea)

- 6.4.4 ABP (Netherlands)

- 6.4.5 California Public Employees' Retirement System (CalPERS)

- 6.4.6 Canada Pension Plan Investment Board (CPPIB)

- 6.4.7 AustralianSuper

- 6.4.8 PFZW (Netherlands)

- 6.4.9 USS (Universities Superannuation Scheme, UK)

- 6.4.10 Afore XXI Banorte (Mexico)

- 6.4.11 National Electrical Benefit Fund

- 6.4.12 Caisse des Depots (France)

- 6.4.13 ATP (Denmark)

- 6.4.14 Federal Retirement Thrift Investment Board

- 6.4.15 Ontario Teachers' Pension Plan

- 6.4.16 Alecta (Sweden)

- 6.4.17 UniSuper (Australia)

- 6.4.18 APG (Netherlands)

- 6.4.19 Public Institute for Social Security (Kuwait)

- 6.4.20 General Organization for Social Insurance (GOSI, Saudi Arabia)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment