PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937419

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937419

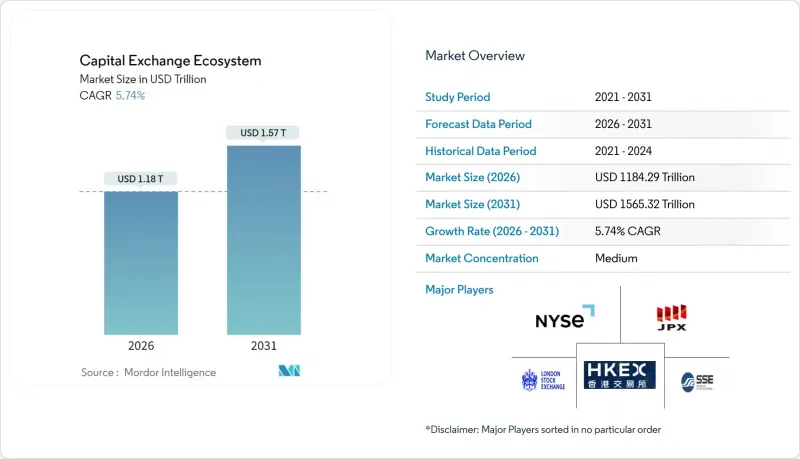

Capital Exchange Ecosystem - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Capital Exchange Ecosystem Market was valued at USD 1120 billion in 2025 and estimated to grow from USD 1184.29 billion in 2026 to reach USD 1565.32 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031).

That signals a structural re-engineering of global price-discovery infrastructure. Technology-enabled revenue sources such as market data feeds, regulatory compliance platforms, and cross-border settlement services now outpace traditional matched-order fees, reshaping value capture across every trading venue tier. Institutional investors continue to drive high-volume execution, yet rapid retail onboarding via mobile interfaces yields multi-stream monetization that reduces cyclicality. Growth in electronic bond trading, scalable ETF ecosystems, and ESG-centric listing frameworks secures defensible expansion levers while also raising the complexity bar for smaller venues. Rising cybersecurity outlays and asynchronous regulatory mandates temper margin expansion, but the overall opportunity remains underpinned by global demand for capital formation and liquidity optimization. Competitive intensity is migrating from pure volume scale toward differentiated cloud-native platforms that deliver micro-second execution, integrated analytics, and modular compliance toolkits, anchoring long-term resilience for operators able to fund sustained R&D.

Global Capital Exchange Ecosystem Market Trends and Insights

Rising Retail Investor Participation Through Digital Brokerage Platforms

Retail onboarding through zero-commission apps shifts revenue dependence from legacy seat-based tariffs toward high-frequency, low-ticket transactions that nonetheless carry elevated data-usage multipliers . Order-flow internalization supplies exchanges with consistent liquidity, and real-time best-execution audits mandated under MiFID III and similar regimes intensify demand for premium analytics feeds that exchanges uniquely curate. Smartphone penetration in India, Indonesia, and Vietnam is driving first-time capital market access, allowing venues to monetize scale without parallel branch-network costs. Fractional share functionality widens the addressable base by eliminating affordability barriers and simultaneously boosts trade counts, elevating core matching-engine cycling requirements. Retail cohorts also exhibit pronounced appetites for short-dated options and leveraged ETFs, broadening derivative revenue baskets. Collectively, the phenomenon underwrites a durable, volume-linked annuity that offsets lumpy institutional block trading cycles.

Growth in Index-Based Passive Investment Vehicles (ETFs)

Passive strategies channel flows toward instruments that demand deep secondary-market liquidity, compelling exchanges to invest in robust market-making incentive structures and intra-day creation-redemption rails. Nasdaq's experience shows per-trade economics in ETF books exceeding conventional equity lanes by 40%, proving the case for product-specific infrastructure outlays and proprietary index licensing. European Union UCITS frameworks facilitate multi-listing, enabling exchanges to lock in recurring listing and maintenance fees while extending reach to cross-border investors. Fixed-income ETF proliferation augments demand for transparent bond pricing, prompting exchanges to integrate composite benchmarks that aggregate fragmented dealer quotes into standardized ticks. These upgrades dampen earnings volatility by attaching fee schedules to assets under management rather than episodic trading bursts. Passive adoption also stimulates continuous data subscription growth, as asset managers require minute-by-minute indicative net-asset values and compliance dashboards to satisfy fiduciary obligations.

Regulatory Fragmentation Across Jurisdictions

Divergent disclosure rules and data-localization statutes compel exchanges to run duplicate systems and legal workflows, inflating overhead by an estimated 15-20% for cross-border operations. MiFID III and post-Brexit UK frameworks already diverge on trade-reporting granularity, forcing parallel compliance code bases. Asia-Pacific's staggered migration to T+1 adds further complexity, fragmenting intraday collateral mobility and weakening settlement netting efficiencies. Absent mutual recognition accords, issuers must duplicate prospectus reviews, elongating time-to-market and dulling exchange competitiveness. Data-sharing restrictions hamper integrated analytics offerings, limiting monetization of cross-venue order flow insights. Together, these frictions shave growth from the capital exchange ecosystem by siphoning resources into non-revenue-generating compliance maintenance.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Cross-Border Listings and Capital Flows

- Expansion of Electronic & Algorithmic Trading Infrastructure

- Cyber-Security Threats Escalating Exchange Operational Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary-market listings climbed at an 11.21% CAGR, illustrating issuer appetite for capital-raising pathways that bundle advisory, ESG disclosure, and investor-relations modules under one exchange roof. Exchanges capture 3-4 times more revenue per IPO relative to secondary trades because end-to-end services span prospectus vetting, post-listing analytics, and ongoing governance compliance. Direct listings and SPAC structures further enlarge fee pools by bypassing legacy underwriting layers while still centralizing in-venue liquidity development. Secondary markets nevertheless delivered 71.92% of 2025 transaction value, confirming that durable liquidity remains foundational to revenue predictability. Algorithmic routing, ETF basket adjustments, and interlisted arbitrage keep throughput high even when listing pipelines pause. Combined, the two streams create a defensible flywheel that anchors the capital exchange ecosystem against cyclical shocks.

Liquidity-rich secondary venues face fee compression as competitive dark pools and zero-commission retail brokers erode spreads, but technology-driven value-adds such as real-time analytics and smart-order-router licensing protect monetization headroom. Exchanges now cross-sell surveillance APIs and transaction cost analysis, embedding themselves deeper in buy-side workflow stacks. ESG-linked rebalancing events and corporate-action automation inject steady order flow that cushions seasonal volume dips. Interoperability with over-the-counter clearing systems expands the accessible addressable market while lowering counterparty risk. Consequently, holistic positioning across primary and secondary lanes secures balanced exposure to both high-margin episodic and low-margin continuous revenue.

Stocks commanded 66.79% of the capital exchange ecosystem share in 2025, reflecting entrenched retail familiarity and mature institutional pipelines. However, electronic bond-trading revenues are growing at 7.95% CAGR as price-discovery transparency gaps narrow via dealer-to-client protocols. Cloud-delivered order-management tools and auto-quote engines have lowered participation barriers, letting smaller asset managers internalize previously voice-based workflows. Exchanges monetize this shift through premium connectivity bundles and composite benchmark licensing. Further, data from ETF basket transactions feeds back into bond valuation models, reinforcing a virtuous analytics cycle.

Corporate-bond electronification is advancing faster than sovereign segments, evidenced by a 9.92% CAGR linked to mandatory best-execution audits and liquidity aggregation algorithms. Government-debt auctions remain volume-heavy but margin-light, prompting exchanges to layer value-added services such as collateral-eligibility scoring and automated repo matching. Hybrid equity-debt instruments like convertible notes blur asset-class boundaries and create cross-selling chances for multi-asset clearing solutions. Overall, integrated fixed-income and equity platforms reduce fragmentation, supporting unified risk dashboards that large asset owners increasingly demand.

The Capital Exchange Ecosystem Market Report is Segmented by Market Composition (Primary Market, Secondary Market), Capital Market (Stocks, Bonds), Stock Type (Common & Preferred Stock, Growth Stock, and More), Bond Type (Government Bonds, Corporate Bonds, Municipal Bonds, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 37.57% of the capital exchange ecosystem size in 2025, underpinned by deep liquidity, entrenched ETF ecosystems, and a unified regulatory backdrop that lowers cross-venue arbitrage frictions. Exchanges here lead the adoption of quantum-resistant encryption, enhancing trust among global asset owners concerned about cyber compromise. SEC stability encourages foreign issuers, particularly tech unicorns from emerging markets, to pursue dual listings that unlock broader investor bases. Cloud partnerships with hyperscalers reduce latency by up to 50%, sustaining algorithmic trader loyalty. Retail participation sustains elevated volumes as zero-fee brokers capitalize on real-time quote accuracy mandated for best execution compliance. Together, these factors preserve regional primacy while setting performance benchmarks for rivals.

Asia-Pacific posts the fastest growth at 9.45% CAGR, benefiting from smartphone-enabled retail access, expanding pension pools, and regulatory liberalization in China and India. Hong Kong leverages its position as a renminbi gateway, while Singapore's derivatives hub status attracts commodity and FX hedgers. Regional exchanges are deploying blockchain for real-time depository updates, trimming post-trade costs and enticing international capital. Cross-border ETF passporting between Japan, Australia, and ASEAN elevates multi-listing revenue. Government support for green-finance frameworks introduces sizable issuance pipelines for ESG-labeled instruments. Scaling digital-ID solutions streamlines KYC, accelerating account openings and trade activation.

Europe navigates MiFID III complexity, but single-market ambitions coupled with ESG leadership create differentiated revenue pools in sustainable finance. London remains attractive for global depository receipts, leveraging English-law familiarity despite Brexit. Continental platforms emphasize clearing-house interoperability, lowering margin duplication for asset-manager clients. Tokenized asset trials in Frankfurt and Paris seek to reclaim innovation leadership and shorten securities-lending cycles. Nordic exchanges capitalize on retail brokerage gamification trends without compromising investor protections. Collectively, these initiatives help the region offset structural fragmentation.

List of Companies Covered in this Report:

- CME Group Inc.

- Intercontinental Exchange Inc.

- Nasdaq Inc.

- London Stock Exchange Group plc

- Hong Kong Exchanges & Clearing Ltd.

- Deutsche Borse AG

- Japan Exchange Group Inc.

- Euronext N.V.

- Shanghai Stock Exchange

- Shenzhen Stock Exchange

- B3 S.A. - Brasil Bolsa Balcao

- TMX Group Ltd.

- Singapore Exchange Ltd.

- Australian Securities Exchange Ltd.

- SIX Group AG (SIX Swiss Exchange)

- Korea Exchange

- National Stock Exchange of India Ltd.

- Bolsa Mexicana de Valores

- Johannesburg Stock Exchange

- Saudi Tadawul Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising retail investor participation through digital brokerage platforms

- 4.2.2 Growth in index-based passive investment vehicles (ETFs)

- 4.2.3 Increasing cross-border listings and capital flows

- 4.2.4 Expansion of electronic & algorithmic trading infrastructure

- 4.2.5 Tokenization of real-world assets enabling fractional exchange trading

- 4.2.6 Integration of ESG data analytics enhancing exchange product differentiation

- 4.3 Market Restraints

- 4.3.1 Regulatory fragmentation across jurisdictions

- 4.3.2 Market volatility and systemic risk concerns

- 4.3.3 Cyber-security threats escalating exchange operational costs

- 4.3.4 Delayed settlement modernization limiting intraday liquidity utilization

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Market Composition

- 5.1.1 Primary Market

- 5.1.2 Secondary Market

- 5.2 By Capital Market

- 5.2.1 Stocks

- 5.2.2 Bonds

- 5.3 By Stock Type

- 5.3.1 Common & Preferred Stock

- 5.3.2 Growth Stock

- 5.3.3 Value Stock

- 5.3.4 Defensive Stock

- 5.4 By Bond Type

- 5.4.1 Government Bonds

- 5.4.2 Corporate Bonds

- 5.4.3 Municipal Bonds

- 5.4.4 Mortgage-backed Bonds

- 5.4.5 Other Bond Types

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia (SG, MY, TH, ID, VN, PH)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 CME Group Inc.

- 6.4.2 Intercontinental Exchange Inc.

- 6.4.3 Nasdaq Inc.

- 6.4.4 London Stock Exchange Group plc

- 6.4.5 Hong Kong Exchanges & Clearing Ltd.

- 6.4.6 Deutsche Borse AG

- 6.4.7 Japan Exchange Group Inc.

- 6.4.8 Euronext N.V.

- 6.4.9 Shanghai Stock Exchange

- 6.4.10 Shenzhen Stock Exchange

- 6.4.11 B3 S.A. - Brasil Bolsa Balcao

- 6.4.12 TMX Group Ltd.

- 6.4.13 Singapore Exchange Ltd.

- 6.4.14 Australian Securities Exchange Ltd.

- 6.4.15 SIX Group AG (SIX Swiss Exchange)

- 6.4.16 Korea Exchange

- 6.4.17 National Stock Exchange of India Ltd.

- 6.4.18 Bolsa Mexicana de Valores

- 6.4.19 Johannesburg Stock Exchange

- 6.4.20 Saudi Tadawul Group

7 Market Opportunities & Future Outlook

- 7.1 Growth of carbon-credit & sustainability-linked securities listings

- 7.2 Monetising AI-driven compliance & surveillance services for issuers