PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937438

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937438

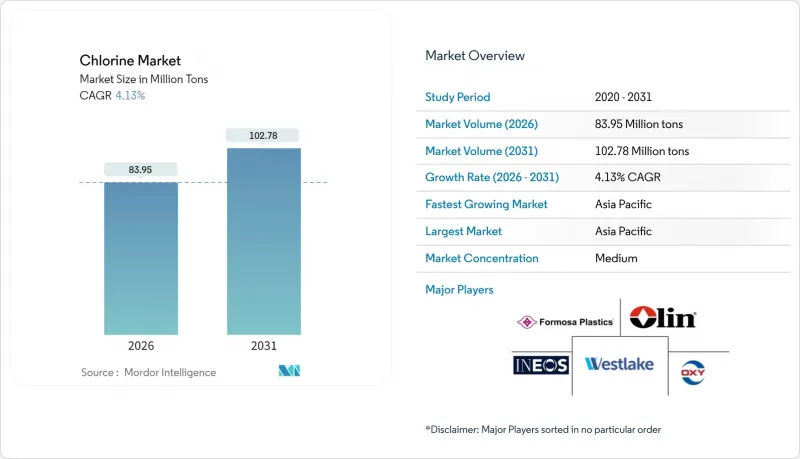

Chlorine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Chlorine market is expected to grow from 80.62 million tons in 2025 to 83.95 million tons in 2026 and is forecast to reach 102.78 million tons by 2031 at 4.13% CAGR over 2026-2031.

Strong infrastructure spending, expanding municipal water treatment programs, and rising pharmaceutical intermediate output maintain the commodity's indispensable status in the worldwide process chain. Membrane-cell technology has overtaken legacy production methods in every leading region, encouraged by lower energy use and tightening environmental rules. A continued uplift in polyvinyl chloride demand for pipes, cable insulation, and flexible films keeps basic feedstock consumption robust, while solid-state battery research, semiconductor etchants, and high-purity intermediates broaden the addressable opportunity for chlorine suppliers. Asia-Pacific dominates volume growth and will remain the principal export base as integrated petrochemical hubs exploit lower logistics costs and access to captive power.

Global Chlorine Market Trends and Insights

Surging PVC Demand in Infrastructure and Packaging

PVC pipe networks for potable water and wastewater drive multi-year chlorine offtake, especially across China, India, Indonesia, and Vietnam where government-backed housing and transportation corridors are underway. The packaging of fast-moving goods favors PVC's toughness and sealing properties, supporting incremental demand from e-commerce distribution centers. Large-scale projects seldom pause during economic slowdowns because they are funded within national stimulus packages, giving the chlorine market a predictable baseline. Integrated chlor-alkali producers are retrofitting plants with energy-efficient membranes to supply vinyl chloride monomer competitively, solidifying their share in coastal industrial parks. The steady course of new extrusion capacity additions in Southeast Asia underlines the structural dependence of builders and converters on affordable chlorine-derived resins.

Rapid Urban Wastewater Investments

Population density in megacities across the Asia-Pacific corridor necessitates larger centralized plants as well as modular systems for peri-urban districts. Chlorination remains the most economical last-step barrier against pathogens, sustaining procurement of on-site electrolyzers and packaged hypochlorite. Regulations in Brazil, South Africa, and the Philippines now specify tertiary disinfection for reclaimed water, lifting future intake beyond historic peak levels. Industrial parks adopt zero-liquid-discharge policies, pushing dual-loop reuse that relies on repeated chlorine contact times. Equipment suppliers note a pivot toward low-salt-input membrane cells that minimize brine disposal, aligning with citywide sustainability charters and fostering repeat chemical consumption contracts.

Tightened Mercury-Cell Plant Phase-Outs in Developing Regions

Mandatory compliance with the Minamata Convention forces remaining mercury facilities in Southeast Asia, Eastern Europe, and parts of Africa offline or into costly conversions. Transitional shutdowns temporarily constrain chlorine availability for local PVC converters and textile bleach plants, while cross-border import flows lift freight rates. Smaller firms unable to finance membrane retrofits exit the industry, nudging regional consolidation. Environmental remediation of legacy sludge ponds absorbs working capital that might otherwise support expansion programs. Operators completing conversions hedge short-term supply gaps with higher-priced imports, contributing to volatility in contract negotiations.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Off-Patent Boom Boosting Chlorination Intermediates

- Battery-Grade Lithium-Metal Chloride for Solid-State EV Batteries

- Escalating Renewable-Power-Driven Caustic Soda Oversupply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EDC/PVC retained 33.29% of the chlorine market share in 2025, mirroring the polymer's ubiquity across pipe, profile, and film categories. Demand concentration allows integrated players to run brine circuits at steady baseload, facilitating high-utilization rates and predictable cash flow. Meanwhile, the chlorine market size attributed to isocyanates and oxygenates is on track to rise at a 4.41% CAGR between 2026 and 2031 as polyurethane foam insulates energy-efficient buildings and lightweight vehicle interiors. Higher margin exposure incentivizes producers to carve out dedicated purity loops or modular reactors, adding flexibility beyond bulk VCM contracts.

Chloromethanes and solvents offer stable demand in refrigeration, silicon wafer cleaning, and herbicide synthesis, shielding volumes from construction cycles. Epichlorohydrin sees incremental lift from water-borne epoxy resins used in corrosion-resistant coatings for offshore wind structures. Inorganic chemicals carved from chlorine underpin coagulant blends for potable water and flue-gas treatment, anchoring non-cyclical intake, especially inside emerging Asian municipalities.

The Chlorine Market Report is Segmented by Application (EDC/PVC, Isocyanates and Oxygenates, Chloromethanes, Solvents and Epichlorohydrin, Inorganic Chemicals, and Other Applications), End-User Industry (Water Treatment, Pharmaceutical, Chemicals, Paper and Pulp, Plastic, Pesticides, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific captured 64.13% of global demand in 2025, underscoring its function as the epicenter of the chlorine market. The combination of integrated refinery-to-PVC value chains, proximity to coal-based power in China, and a robust domestic pipe replacement agenda keeps regional utilization high. The chlorine market size enjoyed by Asia-Pacific will rise further at a 4.72% CAGR to 2031, supported by renewable-powered membrane installations located within emerging industrial parks.

North America remains a mature but technologically advanced arena. Investments focus on process automation, electrode-coating upgrades, and captive chlorine loops for specialty intermediates. PCC Group's 340,000-ton project at Chemours' Mississippi site typifies moves to colocate capacity with downstream titanium dioxide and MDI plants, shortening supply chains and lowering transport risk.

Europe prioritizes sustainable operations and energy efficiency, reflecting high electricity tariffs and ambitious climate rules. Operators benefit from an established customer base in pharmaceuticals and high-end coatings, justifying premium-grade offerings. Concurrently, energy-intensive plants weigh relocation or green-power purchase agreements to offset cost pressures.

- Anwil (Orlen)

- Arkema

- Covestro AG

- DOW

- Ercros S.A

- Formosa Plastics Group

- Hanwha Solutions

- INEOS

- Kem One

- Kuhlmann Europe

- Nobian

- Occidental Petroleum Corporation

- Olin Corporation

- Shivtek Spechemi Industries Ltd

- Spolchemie (KAPRAIN a.s.)

- Tata Chemicals Limited

- Tosoh Corporation

- Vencorex

- Vynova Group (ICIG HOLDING SE)

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PVC demand in infrastructure and packaging

- 4.2.2 Rapid urban wastewater investments

- 4.2.3 Pharmaceutical off-patent boom boosting chlorination intermediates

- 4.2.4 Battery-grade Li-metal chloride for solid-state EV batteries

- 4.2.5 Semiconductor etchant expansion in Asia fabs

- 4.3 Market Restraints

- 4.3.1 Tightened mercury-cell plant phase-outs in developing regions

- 4.3.2 Escalating renewable-power-driven caustic soda oversupply (price squeeze)

- 4.3.3 Growing bromine-based biocide substitution in cooling towers

- 4.4 Value Chain Analysis

- 4.5 Technological Snapshot

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

- 4.7 Pricing Analysis

- 4.8 Import and Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 EDC/PVC

- 5.1.2 Isocyanates and Oxygenates

- 5.1.3 Chloromethanes

- 5.1.4 Solvents and Epichlorohydrin

- 5.1.5 Inorganic Chemicals

- 5.1.6 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceutical

- 5.2.3 Chemicals

- 5.2.4 Paper and Pulp

- 5.2.5 Plastic

- 5.2.6 Pesticides

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anwil (Orlen)

- 6.4.2 Arkema

- 6.4.3 Covestro AG

- 6.4.4 DOW

- 6.4.5 Ercros S.A

- 6.4.6 Formosa Plastics Group

- 6.4.7 Hanwha Solutions

- 6.4.8 INEOS

- 6.4.9 Kem One

- 6.4.10 Kuhlmann Europe

- 6.4.11 Nobian

- 6.4.12 Occidental Petroleum Corporation

- 6.4.13 Olin Corporation

- 6.4.14 Shivtek Spechemi Industries Ltd

- 6.4.15 Spolchemie (KAPRAIN a.s.)

- 6.4.16 Tata Chemicals Limited

- 6.4.17 Tosoh Corporation

- 6.4.18 Vencorex

- 6.4.19 Vynova Group (ICIG HOLDING SE)

- 6.4.20 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment