PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939017

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939017

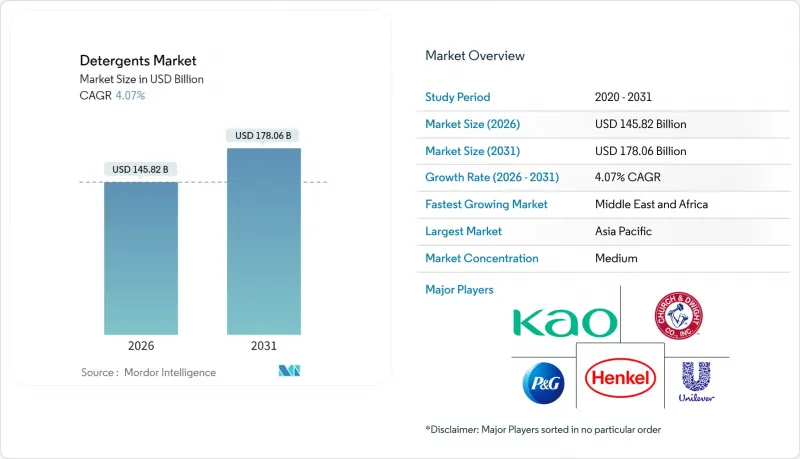

Detergents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Detergents Market was valued at USD 140.12 billion in 2025 and estimated to grow from USD 145.82 billion in 2026 to reach USD 178.06 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031).

Structural shifts stem from cold-water enzymes that reduce household energy use, carbon-pricing policies favoring ultra-concentrated formats, and regulatory mandates that accelerate the adoption of biodegradable surfactants. The Asia-Pacific region continues to drive demand, largely due to the rapid adoption of washing machines, while direct-to-consumer (D2C) subscription services are redefining last-mile economics in North America and China. Competitive intensity remains high: Procter & Gamble, Unilever, and Henkel leverage enzyme technology and concentrated pods to command premium pricing, whereas regional specialists gain share with sachet distribution that meets tight household budgets. Input-cost volatility in palm-kernel oil and enzymes compresses margins for mid-tier brands yet hastens investment in algae-derived and fermentation-based surfactants that bypass constrained supply chains.

Global Detergents Market Trends and Insights

Rising Washing-Machine Penetration in Emerging Economies

Automatic washer ownership in India increased from 14% in 2020 to 28% in 2024, resulting in a rise in per-capita detergent usage, as drum cycles require 30%-40% more product than hand-washing. Smaller 250ml liquid packs and 10-wash sachets help keep entry prices low while sustaining margins above 40%. Similar adoption curves in Indonesia and Vietnam benefit from appliance subsidies and installment-payment schemes. Formulators now specify enzymes optimized for 30-minute, 20°C cycles, with BASF's Lavergy protease delivering equivalent stain removal at 35% lower energy consumption.

Boom in E-Commerce and D2C Channels for Detergents

Direct-to-consumer subscriptions generated USD 4.2 billion in 2024, representing a 38% year-over-year growth as brands bypass retailers' 25%-35% markup. Lower acquisition costs (USD 18 per subscriber) and churn below 15% after the third delivery underpin profitability. Online sales reached 32% in North America and 41% in China, driven by same-day logistics and influencer marketing that emphasize ingredient transparency. Concentrated pods and strips, 70% lighter than equivalent liquids, shave USD 0.12 from last-mile freight while reducing packaging waste by 60%.

Stringent Global and Regional Chemical Regulations

In October 2023, the European Chemicals Agency, under REACH Annex XVII, restricted microplastics, banning their intentional use in rinse-off detergents with transition periods of 4 to 12 years. In April 2024, the US Environmental Protection Agency expanded PFAS restrictions, requiring manufacturers to certify that surfactants and processing aids contain no per- and polyfluoroalkyl substances above 1 part per billion, effectively banning legacy fluorosurfactants in industrial and institutional cleaning products. These regulations disproportionately affect smaller regional brands, which lack the R&D budgets for rapid reformulation, while multinationals spread compliance costs over global volumes exceeding 500,000 metric tons annually.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Shift to Eco-Friendly and Biodegradable Formulations

- Cold-Water Enzyme Breakthroughs Cut Energy Use

- Raw-Material Price Volatility (Surfactants, Enzymes)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anionic surfactants held 45.84% of the Detergents market share in 2025, supported by low-cost linear alkylbenzene sulfonates that anchor powder and liquid staples in South Asia and Africa. Non-ionic alcohol ethoxylates and alkyl polyglucosides, prized for rapid ultimate biodegradation, are forecast to grow at a 4.95% CAGR, lifted by EU rules requiring aerobic breakdown within 28 days. Henkel reformulated Persil Sensitive in 2024 by substituting 40% of LAS with corn-starch-derived alkyl polyglucosides, thereby lowering aquatic toxicity by 35% while retaining the product's performance.

Cationic quaternary ammonium surfactants remain niche outside fabric softeners because their positive charge limits co-formulation with anionics. EPA scrutiny of quats is prompting pilots of faster-biodegrading ester-quat alternatives. Zwitterionic cocamidopropyl betaine, 6% of 2024 volume, stabilizes foam in hard-water markets across the Middle East and North Africa, and its broad pH stability suits cold-water pods that avoid mineral chelators.

The Detergents Market Report is Segmented by Type (Anionic, Cationic, Non-Ionic, and Zwitterionic), Application (Laundry, Household Cleaning, Dishwashing, Fuel Additives, Biological Reagents, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region accounted for 44.10% of the global 2025 volume, driven by a doubling of washing-machine ownership in India and Indonesia, robust e-commerce in China, and a shift toward premiumization of enzyme-rich liquids. Local champions such as Blue Moon and Liby hold a 38% share of China's liquid category through direct online engagement and tailored fragrances. India's market expanded by 7.2% in 2024, driven by affordable 250 ml packs targeting first-time machine users. Mature Japan and South Korea focus on bio-based isethionate surfactants that accelerate soil release by 30%.

The Middle East & Africa are forecast to deliver the fastest growth, with a 4.78% CAGR, as urbanization lifts per-capita consumption above 3 kg. Saudi Arabia's Vision 2030 infrastructure push raises washer penetration toward 65%, spurring demand for hard-water-tolerant pods. South Africa's market increased by 5.8% in volume in 2024, driven by enzyme-fortified powders that perform well in cold cycles, a necessity amid intermittent electricity supply. Sachet-priced powders dominate rural Sub-Saharan Africa, but liquid formats are gaining traction in Lagos and Nairobi as front-load adoption increases.

Europe and North America register slower growth but lead sustainability innovation. Germany's eco-labeled segment reached 42% of 2024 detergent sales. US pods and strips command 32% of laundry volume, and refill stations in Canadian and UK grocers reduce packaging by 40%. South America grew by 4.2% in 2024; powders still hold a 68% share, but liquids are rising in urban Brazil and Argentina, alongside washer ownership above 55%.

- Blue Moon Group

- Church & Dwight Co., Inc.

- Guangzhou Liby Group Co. Ltd

- Henkel AG & Co. KGaA

- Johnson & Johnson Private Limited

- Kao Corporation

- Lion Corporation

- Nice Group

- Procter & Gamble

- Reckitt Benckiser Group plc

- RSPL Group

- SC Johnson

- Seventh Generation Inc.

- Unilever

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising washing-machine penetration in emerging economies

- 4.2.2 Boom in e-commerce and D2C channels for detergents

- 4.2.3 Consumer shift to eco-friendly/biodegradable formulations

- 4.2.4 Cold-water enzyme breakthroughs cut energy use

- 4.2.5 Carbon-tax driven demand for ultra-concentrates

- 4.3 Market Restraints

- 4.3.1 Stringent global and regional chemical regulations

- 4.3.2 Raw-material price volatility (surfactants, enzymes)

- 4.3.3 Micro-plastic filtration mandates raise reformulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anionic Detergents

- 5.1.2 Cationic Detergents

- 5.1.3 Non-ionic Detergents

- 5.1.4 Zwitterionic (Amphoteric) Detergents

- 5.2 By Application

- 5.2.1 Laundry Cleaning Products

- 5.2.2 Household Cleaning Products

- 5.2.3 Dishwashing Products

- 5.2.4 Fuel Additives

- 5.2.5 Biological Reagents

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Blue Moon Group

- 6.4.2 Church & Dwight Co., Inc.

- 6.4.3 Guangzhou Liby Group Co. Ltd

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Johnson & Johnson Private Limited

- 6.4.6 Kao Corporation

- 6.4.7 Lion Corporation

- 6.4.8 Nice Group

- 6.4.9 Procter & Gamble

- 6.4.10 Reckitt Benckiser Group plc

- 6.4.11 RSPL Group

- 6.4.12 SC Johnson

- 6.4.13 Seventh Generation Inc.

- 6.4.14 Unilever

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment