PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939052

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939052

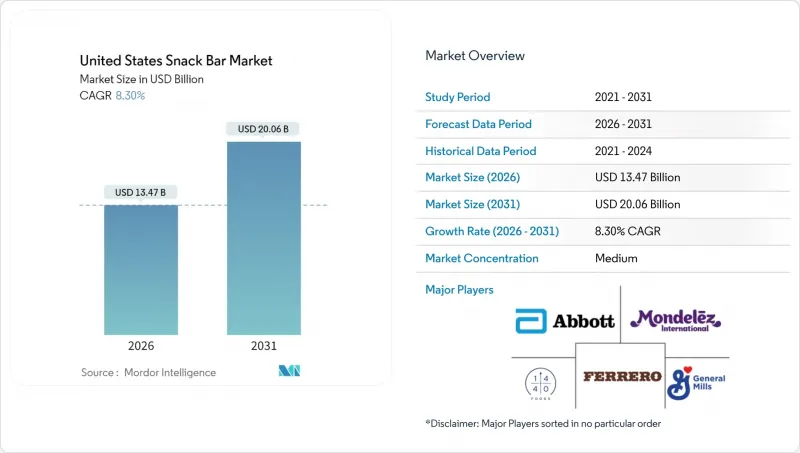

United States Snack Bar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States snack bar market was valued at USD 12.44 billion in 2025 and estimated to grow from USD 13.47 billion in 2026 to reach USD 20.06 billion by 2031, at a CAGR of 8.30% during the forecast period (2026-2031).

The increasing frequency of snacking among consumers is a key driver of this growth, with 88% of United States consumers consuming at least one snack daily and 37% of main meals now including a snack component. This trend highlights the evolving role of snacks in daily diets. The market is further shaped by the rising demand for snack bars that are high in protein and low in sugar, alongside a growing preference for minimally processed formulations based on fruits and nuts. Additionally, premiumization through smaller, more convenient pack sizes is influencing consumer purchasing behavior. Acquisition-driven consolidation, exemplified by Mars's USD 35.9 billion acquisition of Kellanova, is intensifying competition within the market. However, regulatory costs linked to the United States Food and Drug Administration's (FDA) 2028 front-of-package labeling mandate may pose challenges by compressing profit margins for brands that fail to comply. Furthermore, the expansion of online retail subscriptions, direct-to-consumer product bundles, and the functional positioning of snack bars-offering benefits such as energy enhancement, cognitive support, and digestive health-are unlocking new consumption occasions that extend beyond traditional breakfast and sports-nutrition scenarios.

United States Snack Bar Market Trends and Insights

Rising Health and Wellness Trends Emphasizing Nutritious Ingredients

American consumers are redefining snacking as a means of nutrient delivery rather than indulgence, with energy cited as a primary motivation and mood enhancement increasingly sought through food choices. This evolving perspective has elevated snack bars from simple convenience items to essential platforms for functional nutrition. Active adults aged 18 to 45, who prioritize health-conscious decisions, are leading this trend by choosing better-for-you options at significantly higher rates compared to older demographics. Brands that incorporate whole grains, seeds, and ancient grains-such as quinoa, amaranth, and chia-are successfully capturing shelf space that was once dominated by traditional candy bars and cookies. The United States Food and Drug Administration (FDA) finalized its updated "healthy" nutrient-content claim in 2024, allowing snack bars with higher levels of unsaturated fats to qualify as long as they include nutrient-dense ingredients . This regulatory change opens new pathways for reformulation, enabling manufacturers to align their products with both compliance requirements and evolving consumer expectations. Companies that take proactive steps to reformulate their products ahead of the 2028 front-of-package labeling deadline can avoid the reputational risks associated with "high in" warnings for saturated fat, sodium, or added sugars, which could discourage health-conscious shoppers from purchasing their products.

Increasing Demand for High-Protein, Low-Sugar, and Clean-Label Products

Protein bars maintained a significant market share in 2024, reflecting a growing consumer focus on transparency and macronutrient optimization. While 56% of Americans seek to increase protein intake, 67% also prioritize portion control, driving demand for compact products that provide 15 to 20 grams of protein within a 200-calorie limit. Clean-label claims, such as the absence of artificial colors, flavors, and preservatives, have become standard expectations. Certifications like Non-GMO (Non-Genetically Modified Organism) Project verification and USDA (United States Department of Agriculture) Organic certification act as trust indicators, often allowing brands to command higher price points. Abbott's Ensure Max Protein line, reformulated in 2024 to include 30 grams of protein and zero added sugar, highlights how established nutrition brands are adapting to snack-bar formats to meet the needs of on-the-go consumers. Alternative sweeteners, including allulose, monk fruit, and stevia, are increasingly replacing high-fructose corn syrup and cane sugar. This shift enables brands to reduce added sugars to below 5 grams per serving while maintaining taste, addressing a formulation challenge that has previously hindered broader adoption among casual snackers.

Regulatory Pressure on Labeling and Health Claims

The United States Food and Drug Administration (FDA)'s proposed front-of-package labeling rule, published in 2024, introduces a requirement for packaged foods to display "high in" warnings for saturated fat, sodium, or added sugars if these nutrients exceed specified thresholds. This regulation is expected to impose an annual cost of approximately USD 333 million on the snack-bar industry, covering expenses related to compliance, reformulation of products, and packaging redesign. Brands that fail to reformulate their products by the 2028 implementation deadline face significant risks, including potential backlash from consumers and the possibility of being de-listed by retailers. Supermarkets are increasingly curating their shelves to feature products that align with public health guidelines, further pressuring manufacturers to comply. Additionally, the updated "healthy" nutrient-content claim, finalized in 2024, permits snack bars to contain higher levels of unsaturated fats if they include nutrient-dense ingredients. However, meeting the stringent criteria-such as limits on saturated fat, sodium, and added sugars while ensuring the inclusion of meaningful amounts of food-group components-poses significant challenges. These requirements necessitate extensive research and development (R&D) efforts, leading to delays in product launches and increased costs. Smaller brands, often lacking dedicated regulatory affairs teams, bear a disproportionate burden, which widens the competitive gap in favor of multinational corporations like General Mills, Nestle, and PepsiCo. These larger companies are better positioned to absorb compliance costs across their extensive product portfolios, giving them a distinct advantage in navigating the evolving regulatory landscape.

Other drivers and restraints analyzed in the detailed report include:

- Popularity of Fitness Culture Driving Demand for Energy and Protein Bars

- Growing Interest in Organic and Clean-Label Snack Bars

- Concerns About High Sugar, Unhealthy Fats, and Artificial Ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Protein bars accounted for 47.02% of the market share in 2025, driven by consistent demand from fitness enthusiasts, weight-management consumers, and meal-replacement users. These consumers prioritize macronutrient density over ingredient simplicity, making protein bars a preferred choice for their dietary needs. The segment's dominance reflects its ability to cater to individuals seeking convenient, high-protein options that align with their active lifestyles and nutritional goals. However, fruit and nut bars are emerging as a strong contender, projected to grow at a compound annual growth rate (CAGR) of 9.29% from 2026 to 2031, the highest growth rate among all product types. This growth is fueled by a shift in consumer preferences toward minimally processed products that utilize natural ingredients such as dates, figs, and cashews as binders and sweeteners. These bars appeal to health-conscious individuals looking to avoid synthetic isolates and sugar alcohols commonly found in protein-focused products.

Energy bars, enriched with caffeine and B vitamins, continue to serve specific needs such as pre-workout energy boosts and mid-afternoon pick-me-ups. These products are designed to provide a quick and efficient source of energy for busy consumers. On the other hand, cereal bars, often positioned as convenient breakfast alternatives, are facing challenges. Declining cold-cereal consumption and increasing competition from portable breakfast options like oatmeal cups and Greek yogurt pouches have created headwinds for this segment. In response to evolving consumer demands, companies are innovating to retain market share. For instance, Quest Nutrition's 2024 launch of Hero bars, which combine 15 grams of protein with candy-bar-inspired flavors, demonstrates how established players are addressing the taste preferences of consumers while maintaining the nutritional benefits of protein bars. This strategy highlights the ongoing efforts to balance indulgence with health-focused attributes in the competitive snack market.

Nut-based bars accounted for 32.88% of the ingredient-based segment in 2025, driven by the inclusion of almonds, cashews, and peanuts. These ingredients are valued for their ability to provide healthy fats, plant-based protein, and a satisfying texture, making them a popular choice among health-conscious consumers. Dairy and protein-based formulations are expected to grow at the fastest rate, with a compound annual growth rate (CAGR) of 9.44% through 2031. This growth is fueled by manufacturers incorporating whey protein isolates, casein, and milk protein concentrates into date-sweetened or oat-based formulations. These products cater to the increasing demand for clean-label and high-protein options while avoiding soy or pea protein, which some consumers perceive as less favorable due to concerns about taste and bioavailability. This trend highlights the evolving preferences of consumers who seek both nutritional benefits and superior taste profiles in their snack choices.

Granola and oat-based bars, a traditional subcategory, are facing stagnation as private-label products from brands such as Costco's Kirkland and Trader Joe's offer prices that are 20% to 30% lower than branded alternatives. This pricing pressure has compelled established players like Nature Valley and Quaker to differentiate their offerings by emphasizing organic certifications or incorporating functional ingredients such as chia seeds, flaxseed, and hemp hearts to justify their premium positioning. Meanwhile, date-based bars, popularized by brands like RXBAR and Larabar, occupy a premium niche but are constrained by the limited availability and price volatility of dates. Hybrid blends, which combine nuts, oats, dates, and dairy proteins, are emerging as a promising formulation that balances taste, texture, and nutritional profiles. However, these blends require advanced extrusion and baking technologies, leading to higher capital expenditures and creating significant barriers to entry for smaller brands. This dynamic underscores the importance of innovation and operational efficiency in maintaining competitiveness within the market.

The United States Snack Bar Market Report is Segmented by Product Type (Cereal Bar, Energy Bar, and More), Ingredient Base (Nut-Based Bars, Granola/Oat-based, Date-Based and More), Price Tier (Mass and Premium) and Distribution Channels (Supermarket/Hypermarket, Online Retail Store and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (tonnes).

List of Companies Covered in this Report:

- 1440 Foods Company

- Abbott Laboratories

- Mondelez International Inc.

- Ferrero International SA

- General Mills Inc.

- GoMacro LLC

- Kellanova

- KIND LLC

- Mars Incorporated

- Nestle SA

- Caveman Foods LLC

- PepsiCo Inc.

- Power Crunch Pty Ltd

- Premier Nutrition Company LLC

- Probar Inc.

- Quest Nutrition LLC

- Conagra Brands Inc.

- Simply Good Foods Co.

- The Hershey Company

- Nature's Bakery LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health and wellness trends emphasizing nutritious ingredients

- 4.2.2 Increasing demand for high-protein, low-sugar, and clean-label products

- 4.2.3 Popularity of fitness culture driving demand for energy and protein bars

- 4.2.4 Growing interest in organic and clean-label snack bars

- 4.2.5 Consumers' preference for sustainable and ethically sourced ingredients

- 4.2.6 Development of functional snack bars targeting cognitive and digestive health

- 4.3 Market Restraints

- 4.3.1 Regulatory pressure on labeling and health claims

- 4.3.2 Concerns about high sugar, unhealthy fats, and artificial ingredients

- 4.3.3 High competition from traditional snacks and alternative snack options

- 4.3.4 Difficulty in balancing taste with health and nutritional value

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Cereal Bar

- 5.1.2 Energy Bar

- 5.1.3 Protein Bar

- 5.1.4 Fruit and Nut Bar

- 5.2 By Ingredient Base

- 5.2.1 Nut-based bars

- 5.2.2 Granola/Oat-based

- 5.2.3 Date-based

- 5.2.4 Dairy/Protein-based

- 5.2.5 Hybrid blends

- 5.2.6 Other Forms

- 5.3 By Price Tier

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Supermarket/Hypermarket

- 5.4.2 Online Retail Store

- 5.4.3 Convenience Store

- 5.4.4 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 1440 Foods Company

- 6.4.2 Abbott Laboratories

- 6.4.3 Mondelez International Inc.

- 6.4.4 Ferrero International SA

- 6.4.5 General Mills Inc.

- 6.4.6 GoMacro LLC

- 6.4.7 Kellanova

- 6.4.8 KIND LLC

- 6.4.9 Mars Incorporated

- 6.4.10 Nestle SA

- 6.4.11 Caveman Foods LLC

- 6.4.12 PepsiCo Inc.

- 6.4.13 Power Crunch Pty Ltd

- 6.4.14 Premier Nutrition Company LLC

- 6.4.15 Probar Inc.

- 6.4.16 Quest Nutrition LLC

- 6.4.17 Conagra Brands Inc.

- 6.4.18 Simply Good Foods Co.

- 6.4.19 The Hershey Company

- 6.4.20 Nature's Bakery LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK