PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939055

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939055

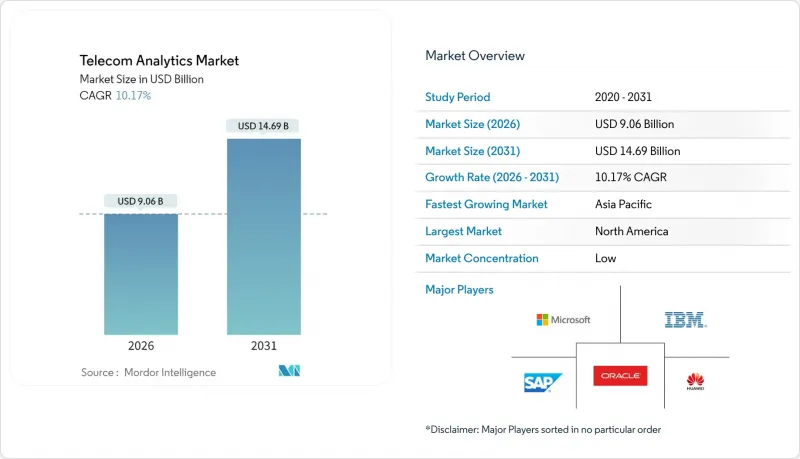

Telecom Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The telecom analytics market was valued at USD 8.22 billion in 2025 and estimated to grow from USD 9.06 billion in 2026 to reach USD 14.69 billion by 2031, at a CAGR of 10.17% during the forecast period (2026-2031).

This robust trajectory is propelled by relentless 5G roll-outs, fast-maturing AI toolkits, and the rising cost of fraud, each of which is nudging operators toward predictive, real-time analytics. Cloud-native architectures now underpin most large deployments, while edge nodes are assuming a pivotal role in latency-sensitive use cases such as private 5G and massive IoT. Competition is intensifying as network vendors, hyperscalers, and niche specialists race to embed generative AI, automated model lifecycle management, and slice-aware dashboards into their offers. At the same time, operators are shifting focus from capital-intensive software investments to outcome-based analytics services that guarantee measurable churn reduction and revenue assurance

Global Telecom Analytics Market Trends and Insights

Rapid 5G Deployment Spurring Network Analytics Adoption

Standalone 5G roll-outs are magnifying data volumes and performance variables, compelling operators to adopt real-time slice-aware analytics engines that optimize spectrum, power, and quality of service. China is on track for 88% 5G penetration by 2028, turning the region into the largest single source of network telemetry. Slice-specific dashboards unlock a USD 200 billion monetization pool by guaranteeing deterministic latency and throughput for enterprise use cases. Edge compute nodes add fresh complexity because telemetry now arrives from multiple hierarchy layers, each demanding millisecond-level insight. In Asia-Pacific, these requirements underpin a 13.26% CAGR in Telecom Analytics market adoption as state-owned carriers race to deliver ultra-reliable services for Industry 4.0.

Increasing Vulnerability to Fraudulent Activities

Telecom fraud losses ballooned to USD 39.89 billion in 2024, equivalent to 2.22% of global operator revenue . Fraud rings now weaponize AI to automate SIM-swap, subscription, and roaming exploits, exhausting the cAsia Pacificity of legacy rule engines. Operators therefore pivot to graph-based analytics and self-learning anomaly detectors that fuse CDRs, signaling data, and customer profiles in near real time. Emerging markets bear the brunt because rapid subscriber growth outpaces fraud-mitigation investment, pushing fraud-centric analytics to the top of procurement roadmaps. A recent industry poll shows 83% of fraud teams intend to deploy generative AI by 2025, even though poor data labeling remains a hurdle.

Data Privacy and Cross-Border Transfer Restrictions

A tightening web of data-protection rules is splintering global analytics footprints. GDPR, India's Digital Personal Data Protection Act, and China's PIPL each impose local-processing mandates that force operators to duplicate infrastructure and embed privacy-by-design controls. Multinational CSPs must encrypt, tokenize, or anonymize subscriber records before moving them across borders, adding latency and diluting model accuracy. The compliance burden is most acute in Asia Pacific, where divergent national laws require bespoke security blueprints for every market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Zero-Touch Operations Creating Closed-Loop Analytics Demand

- Accelerated Adoption of Cloud-Native Analytics by Telcos

- Scarcity of Telco-Specific Labeled Datasets for AI Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fraud Management Analytics has become the fastest-expanding segment, growing at a 16.90% CAGR on the back of industry losses that exceeded USD 39.89 billion in 2024. These platforms blend graph analytics and deep-learning engines to pinpoint suspicious call-detail records and roaming patterns within seconds, enabling operators to freeze illicit traffic before revenue leakage occurs. Customer Analytics nevertheless retains leadership with 36.24% of the Telecom Analytics market in 2025 as carriers intensify personalized retention campaigns, churn-prediction models, and lifetime-value scoring.

Network Analytics underpins autonomous slice orchestration, feeding closed-loop controllers with KPI forecasts that avert congestion and improve 5G experience consistency. Service-Quality and Experience Analytics is gaining ground as operators publish real-time experience scores to enterprise dashboards, a prerequisite for monetizing SLAs in manufacturing, mining, and healthcare. Marketing and Sales Analytics applies propensity modeling to boost campaign ROI, while Pricing and Revenue-Management Analytics optimizes tariff bundling and dynamic discounting. Collectively, application-layer tools propel cross-domain visibility, a prerequisite for zero-touch operations.

Edge and hybrid configurations are registering a 21.92% CAGR due to mission-critical verticals ports, factories, and utilities demanding sub-10 millisecond insight loops. Operators now embed lightweight inference engines at base-band units and on-prem edge nodes to enforce latency budgets and data-sovereignty rules. The cloud model still controlled 65.45% of the Telecom Analytics market in 2025 by hosting CPU-hungry training jobs and long-cycle batch analytics.

Hybrid blueprints marry the two worlds: cloud bursting handles volatile workloads, while edge sites execute deterministic tasks like anomaly alarms. On-prem deployments persist in heavily regulated jurisdictions or where legacy BSS/OSS systems resist migration. As 5G Advanced and 6G roadmaps unfold, vendors are baking multi-cluster observability, federated identity, and automated policy rollout into deployment templates, making it easier to pivot between compute domains.

The Telecom Analytics Market Report is Segmented by Application (Customer, Network Analytics, and More), Deployment (Cloud and More), Component (Software, Services), End-User Enterprise Size (Small and Medium Enterprises, Large Enterprises), Telecom Operator Type (Mobile Network Operators, Fixed-Line Operators, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated the Telecom Analytics market with 34.55% share in 2025, buoyed by early 5G monetization and enterprise-grade private-network demand. The U.S. carriers are leveraging analytics to orchestrate network-as-a-service offers for manufacturing, healthcare, and defense, capitalizing on a private-5G spend that will surpass USD 3.7 billion by 2027. Consolidation moves such as T-Mobile's fiber acquisitions are also stoking analytics investment to integrate fixed and mobile quality metrics.

Asia-Pacific is the fastest-growing region at 13.06% CAGR, led by China's aggressive deployment roadmap and India's rapid digitalization. The region's mobile-services revenue could climb from USD 321.9 billion in 2023 to USD 388.7 billion in 2028, and analytics is crucial for converting that traffic into profit. Governments are championing indigenous AI frameworks, prompting operators to adopt federated-learning models that keep raw data local while sharing model weights globally.

Europe maintains steady expansion as GDPR drives demand for privacy-enhancing technologies and hybrid deployments. Operators must demonstrate auditability and real-time breach detection, pushing analytics vendors to incorporate consent management and lineage tracking.

Middle East and Africa and South America trail in absolute size but show upside as green-field 5G launches bypass legacy OSS and leapfrog directly to cloud-native analytics stacks.

- Accenture plc

- Amdocs Inc.

- Cisco Systems, Inc.

- Dell Inc.

- Ericsson AB

- Guavus, Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- InfoFaces, Inc.

- Microsoft Corporation

- Nokia Corporation

- Oracle Corporation

- SAS Institute Inc.

- SAP SE

- Subex Limited

- TEOCO Corporation

- Teradata Corporation

- Wipro Limited

- ZTE Corporation

- Mu Sigma, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in need for churn reduction

- 4.2.2 Increasing vulnerability to fraudulent activities

- 4.2.3 Rapid 5G deployment spurring network analytics adoption

- 4.2.4 Accelerated adoption of cloud-native analytics by telcos

- 4.2.5 Emergence of network slicing analytics for private 5G networks

- 4.2.6 AI-driven zero-touch operations creating closed-loop analytics demand

- 4.3 Market Restraints

- 4.3.1 Lack of awareness among telecom operators

- 4.3.2 Data privacy and cross-border transfer restrictions

- 4.3.3 OPEX strain from spectrum auctions curbing on-prem investments

- 4.3.4 Scarcity of telco-specific labelled datasets for AI models

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pandemic Impact Review

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Customer Analytics

- 5.1.2 Network Analytics

- 5.1.3 Marketing and Sales Analytics

- 5.1.4 Pricing and Revenue-Management Analytics

- 5.1.5 Service Quality and Experience Analytics

- 5.1.6 Fraud Management Analytics

- 5.1.7 Other Application

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Edge / Hybrid

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.3.2.1 Professional Services

- 5.3.2.2 Managed Services

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Telecom Operator Type

- 5.5.1 Mobile Network Operators (MNOs)

- 5.5.2 Fixed-line Operators

- 5.5.3 Internet Service Providers (ISPs)

- 5.5.4 Mobile Virtual Network Operators (MVNOs)

- 5.5.5 Converged Operators

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Colombia

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Accenture plc

- 6.4.2 Amdocs Inc.

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Dell Inc.

- 6.4.5 Ericsson AB

- 6.4.6 Guavus, Inc.

- 6.4.7 Huawei Technologies Co., Ltd.

- 6.4.8 IBM Corporation

- 6.4.9 InfoFaces, Inc.

- 6.4.10 Microsoft Corporation

- 6.4.11 Nokia Corporation

- 6.4.12 Oracle Corporation

- 6.4.13 SAS Institute Inc.

- 6.4.14 SAP SE

- 6.4.15 Subex Limited

- 6.4.16 TEOCO Corporation

- 6.4.17 Teradata Corporation

- 6.4.18 Wipro Limited

- 6.4.19 ZTE Corporation

- 6.4.20 Mu Sigma, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment