PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939064

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939064

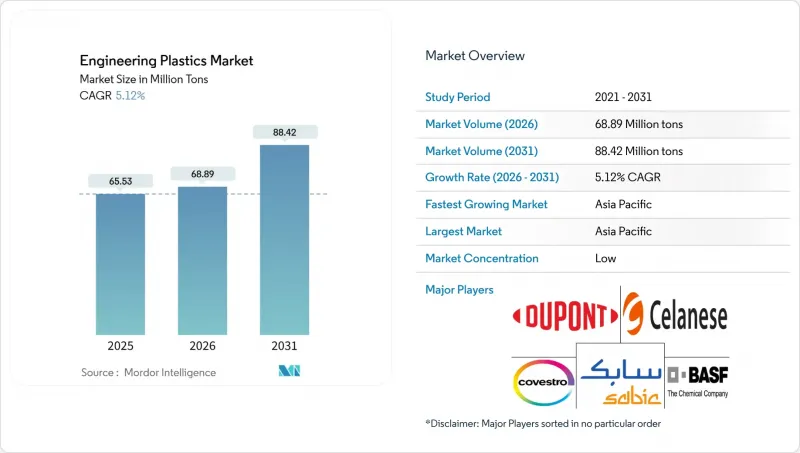

Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Engineering Plastics Market was valued at 62.25 million tons in 2025 and estimated to grow from 65.38 million tons in 2026 to reach 83.54 million tons by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

Demand stems from lightweighting programs across the mobility and aerospace sectors, the electrification of vehicles and industrial equipment, and the growing adoption of semiconductor fabrication, all of which reward materials that offer high strength-to-weight ratios and geometric freedom. Sustained capital spending on Asia-Pacific capacity, the emergence of chemical recycling at a commercial scale, and regulatory pushes for fuel economy and carbon reduction further reinforce growth momentum.

Global Engineering Plastics Market Trends and Insights

Lightweighting Push in Mobility and Aerospace

Automotive fuel-economy mandates, such as the US CAFE target of 54.5 mpg by 2025, intensify OEM (original equipment manufacturer) focus on weight reduction, and every 10% mass cut yields 6-8% efficiency gains. Aircraft programs illustrate parallel dynamics: the Boeing 787 achieved 22% fuel savings with 50% composite content, while the Airbus A350 utilizes 53% composites to achieve a similar effect. Carbon-fiber-reinforced thermoplastics gain share because they can be reheated and recycled, unlike thermosets, and automated fiber placement lowers cycle times. Wind-turbine blades now consume larger volumes of carbon fiber than the aerospace industry, with 100-meter blades trimming mass by 38% compared to glass-fiber designs. These successes raise confidence among OEMs evaluating polymer-based structures for wheels, seating, and secondary aircraft structures.

Electrification-Led Demand Spike

High-voltage electric vehicles require enclosures that offer robust flame retardancy and dielectric strength, pushing polyphenylene sulfide, polyether ether ketone, and glass-filled polyamide consumption upward. Robotics lines such as Tesla's Optimus prototype highlight PEEK's longevity under continuous duty, validating higher-end grades for actuators. Semiconductor fabs scaling for AI chips adopt liquid-crystal polymers for fine-pitch connectors that remain dimensionally stable above 260 °C, preserving signal integrity during lead-free reflow. The migration from 400-V to 800-V EV (electric vehicle) architectures amplifies dielectric stress, prompting OEMs to specify insulation with comparative tracking index (CTI) values above 600. Meanwhile, thermal-runaway barriers increasingly incorporate polycarbonate-siloxane blends to prevent heat propagation without resorting to heavy metallic shields.

Monomer Price Volatility

Propylene and ethylene prices track crude swings because Asian crackers rely heavily on naphtha; a USD 10/bbl oil jump can increase propylene costs by USD 90/ton, compressing converters' margins when selling into fixed-price OEM contracts. China's styrene monomer capacity reached 21.51 million tons in H1 2025, accounting for 49% of the global supply and triggering spot price collapses below cash costs for high-cost producers. Tariff escalations between major economies further distort trade flows, forcing rapid output cuts at styrene-based ABS and polycarbonate plants. Volatility particularly stings high-performance resins such as polyimide, whose specialized dianhydride monomers command 4-5X commodity feedstock prices, limiting the ability to pass on surges in tight downstream markets.

Other drivers and restraints analyzed in the detailed report include:

- APAC Manufacturing Migration

- EV Battery Module Housings Adoption

- Packaging Regulations Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene terephthalate (PET) maintained a commanding 50.05% engineering plastics market share in 2025, driven by ubiquitous demand for beverages and rigid packaging. Yet the segment contends with plateauing single-use volumes and mounting recycled-content targets that require process investments. Polyamide blends are gaining renewed traction as automakers opt for bio-based PA11 to reduce scope 3 emissions without compromising tensile strength. Fluoropolymers, although comprising only a mid-single-digit slice of the engineering plastics market, post the fastest 7.34% CAGR because their unrivaled chemical and thermal resistance support aerospace wire coatings and sub-7 nm chip making.

Polysulfones, PEEK (Polyetheretherketone or Polyether Ether Ketone), and liquid-crystal polymers are suitable for niche applications where melting points exceed 280°C and continuous-use temperatures surpass 240°C. Polycarbonate endures scrutiny for BPA (Bisphenol A) in foodware but retains dominance in glazing and consumer electronics housings due to its impact resilience. Polyoxymethylene offers machining ease for gears and window lifters, while styrene copolymers bridge the gap between commodity ABS (Acrylonitrile Butadiene Styrene) and specialty blends, making them a go-to for appliance frames that require balanced toughness and cost.

The Engineering Plastics Market Report is Segmented by Resin Type (Fluoropolymer, Liquid Crystal Polymer, Polyamide, Polybutylene Terephthalate, Polycarbonate, and More), End-User Industry (Aerospace, Automotive, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

The Asia-Pacific region led with a 55.10% engineering plastics market share in 2025 and is expected to expand at a 5.38% CAGR through 2031, driven by the build-out of Chinese and Indian capacities, accelerating EV adoption, and sustained electronics export demand. Chinese styrene production, already 49% of global output, reinforces regional price leadership, while state policies encourage high-value polymer self-sufficiency. India leverages tax credits and import duty relief to draw multinational molders eyeing southern automotive hubs. Japan focuses on ultra-high-purity polymers for semiconductor photomasks, demonstrating the region's spectrum from volume to value.

North America enjoys robust demand from the commercial aerospace sector and an expanding battery-manufacturing corridor that stretches from Michigan to Georgia. Legislative support for advanced recycling, including the US Internal Revenue Code S 45Z clean-fuel credits applicable to chemical recycling outputs, incentivizes innovation in the circular economy. Europe champions sustainability leadership through the Green Deal, spurring R&D in bio-based PA and chemically recycled polycarbonate, although high power costs and PFAS debates weigh on fluoropolymer capacity additions.

South America sees incremental growth tied to automotive localization in Brazil and Argentina, yet remains net-import-reliant for high-performance grades. Middle East & Africa emerge as investment destinations following ADNOC's vertical integration move, which positions the region as a potential net exporter of specialty engineering resins once Covestro capacity synergies materialize. Across all regions, the globalization of supply chains means that engineering plastics market size evolves in lock-step with downstream manufacturing shifts rather than mere resin production footprints.

- Alfa S.A.B. de C.V.

- Arkema

- Asahi Kasei Corporation

- BASF

- Celanese Corporation

- CHIMEI

- Covestro AG

- Dongyue Group

- Envalior

- DuPont

- Evonik Industries AG

- Far Eastern New Century Co., Ltd.

- Indorama Ventures Public Company Limited.

- Lanxess AG

- LG Chem

- Mitsubishi Chemical Group Corporation

- SABIC

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweighting Push in Mobility and Aerospace

- 4.2.2 Electrification-led and Demand Spike

- 4.2.3 Asia-Pacific Manufacturing Migration

- 4.2.4 EV Battery Module Housings Adoption

- 4.2.5 Chemical-recycling Supply Boosts

- 4.2.6 OEM switch to bio-based PA/PTT

- 4.3 Market Restraints

- 4.3.1 Monomer Price Volatility

- 4.3.2 Packaging Regulations Tightening

- 4.3.3 Fluorspar-linked Fluoropolymer Shortage

- 4.3.4 Metal AM substitution threat

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Import And Export Trends

- 4.6.1 Fluoropolymer Trade

- 4.6.2 Polyamide (PA) Trade

- 4.6.3 Polyethylene Terephthalate (PET) Trade

- 4.6.4 Polymethyl Methacrylate (PMMA) Trade

- 4.6.5 Polyoxymethylene (POM) Trade

- 4.6.6 Styrene Copolymers (ABS and SAN) Trade

- 4.6.7 Polycarbonate (PC) Trade

- 4.7 Price Trends

- 4.7.1 Fluoropolymer

- 4.7.2 Polycarbonate (PC)

- 4.7.3 Polyethylene Terephthalate (PET)

- 4.7.4 Polyoxymethylene (POM)

- 4.7.5 Polymethyl Methacrylate (PMMA)

- 4.7.6 Styrene Copolymers (ABS and SAN)

- 4.7.7 Polyamide (PA)

- 4.8 Recycling Overview

- 4.8.1 Polyamide (PA) Recycling Trends

- 4.8.2 Polycarbonate (PC) Recycling Trends

- 4.8.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.8.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.9 Regulatory Framework

- 4.10 Licensors Overview

- 4.11 Production Overview

- 4.12 End-use Sector Trends

- 4.12.1 Aerospace (Aerospace Component Production Revenue)

- 4.12.2 Automotive (Automobile Production)

- 4.12.3 Building and Construction (New Construction Floor Area)

- 4.12.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.12.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume and Value)

- 5.1 By Resin Type

- 5.1.1 Fluoropolymer

- 5.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.1.1.4 Polyvinylfluoride (PVF)

- 5.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.1.1.6 Other Sub Resin Types

- 5.1.2 Liquid Crystal Polymer (LCP)

- 5.1.3 Polyamide (PA)

- 5.1.3.1 Aramid

- 5.1.3.2 Polyamide (PA) 6

- 5.1.3.3 Polyamide (PA) 66

- 5.1.3.4 Polyphthalamide

- 5.1.4 Polybutylene Terephthalate (PBT)

- 5.1.5 Polycarbonate (PC)

- 5.1.6 Polyether Ether Ketone (PEEK)

- 5.1.7 Polyethylene Terephthalate (PET)

- 5.1.8 Polyimide (PI)

- 5.1.9 Polymethyl Methacrylate (PMMA)

- 5.1.10 Polyoxymethylene (POM)

- 5.1.11 Styrene Copolymers (ABS, SAN)

- 5.1.1 Fluoropolymer

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial and Machinery

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 CHIMEI

- 6.4.7 Covestro AG

- 6.4.8 Dongyue Group

- 6.4.9 Envalior

- 6.4.10 DuPont

- 6.4.11 Evonik Industries AG

- 6.4.12 Far Eastern New Century Co., Ltd.

- 6.4.13 Indorama Ventures Public Company Limited.

- 6.4.14 Lanxess AG

- 6.4.15 LG Chem

- 6.4.16 Mitsubishi Chemical Group Corporation

- 6.4.17 SABIC

- 6.4.18 Syensqo

- 6.4.19 Teijin Limited

- 6.4.20 Toray Industries Inc.

- 6.4.21 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Self-Healing Plastics

8 Key Strategic Questions for CEOs