PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939067

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939067

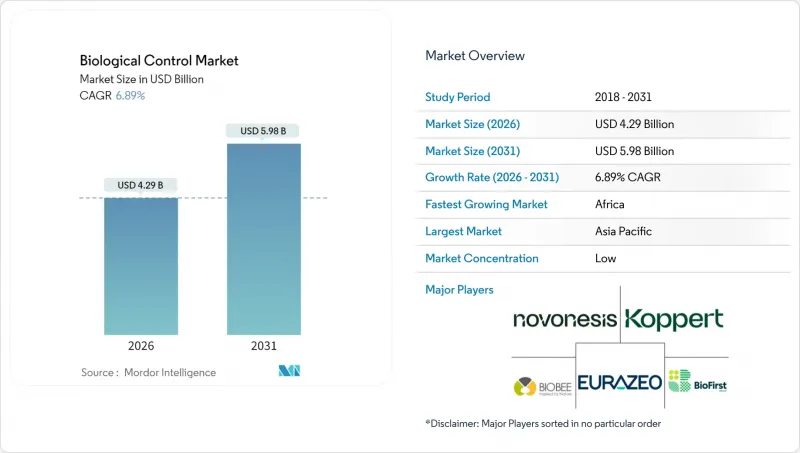

Biological Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The biological control market was valued at USD 4.01 billion in 2025 and estimated to grow from USD 4.29 billion in 2026 to reach USD 5.98 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031).

Cost-effective microbial platforms, automation in insect rearing, and mounting regulatory pressure against conventional pesticides are accelerating adoption across major crop systems. Asia-Pacific drives global demand through expansive government subsidy programs, while Africa's aggressive food-security initiatives anchor the fastest growth outlook. Rapid pest resistance to synthetic chemistries and rising consumer preference for certified-organic produce continue to expand addressable acreage. Meanwhile, fermentation innovation and longer shelf-life formulations are narrowing historical performance gaps with chemical alternatives, strengthening the competitive position of biological inputs.

Global Biological Control Market Trends and Insights

Stringent bans on high-toxicity synthetic pesticides

Regulators continue to phase out high-risk chemistries, catalyzing immediate substitution opportunities for biological solutions. The European Union Farm-to-Fork Strategy mandates a 50% cut in chemical pesticide use by 2030, and the United States Environmental Protection Agency (EPA) has canceled more than 40 active ingredients since 2024. Brazil and India issued parallel restrictions in 2024, increasing near-term acreage available for biocontrol adoption. These policy moves encourage manufacturers to accelerate product launches and spur farmers to recalibrate crop-protection programs toward IPM frameworks.

Rising global demand for certified-organic produce

Global organic food sales climbed to USD 134 billion in 2024, with annual growth above 8% in the United States, Germany, and China. Supermarkets enforce residue-free supplier policies, pushing growers to adopt biological inputs that preserve certification. Premium farm-gate prices, typically 20-40% above conventional produce, offset higher biological agent costs and facilitate deeper penetration in high-value horticulture.

Short commercial shelf-life for many living products

Most macrobial biocontrol agents maintain viability for only 2-4 weeks even under refrigerated conditions, necessitating expensive cold-chain logistics systems and significantly restricting market penetration in regions experiencing unreliable electricity supply. While recent technological advances in encapsulation methods and cryoprotectant formulations have demonstrated the potential to double product shelf-life in pilot studies, these improvements still fall considerably short of matching the multi-year stability achieved by synthetic chemical alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating pest resistance to conventional chemistries

- Government subsidies for IPM adoption and biological inputs

- Protracted multi-agency registration timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Macrobials maintained their commanding 97.25% market share of the biological control market in 2025, reflecting decades of commercial development in beneficial insect production and established distribution networks that serve agricultural markets worldwide. The segment's dominance stems from proven efficacy in field applications and farmer familiarity with release protocols for predatory insects and parasitoids. Entomopathogenic nematodes represent the largest macrobial category, particularly effective against soil-dwelling pests in row crop systems. At the same time, predators and parasitoids excel in greenhouse environments where environmental conditions can be controlled.

Microbials are emerging as the growth engine with an 8.59% forecast CAGR through 2031. The shift toward microbials reflects technological advances in fermentation processes and formulation stability that are addressing historical limitations of bacterial and fungal biocontrol agents. Recent regulatory approvals for multi-strain microbial products are expanding application possibilities, particularly in high-value horticultural crops, where precision application justifies premium pricing. Other microbials, including viral and protozoan agents, remain niche applications but show promise for specific pest complexes where conventional approaches have failed. The form segmentation evolution indicates how different biological mechanisms are finding optimal commercial applications based on target pest biology and crop production systems.

The Biological Control Market Report is Segmented by Form (Macrobials, Microbials), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia-Pacific commanded 66.80% of the biological control market in 2025, reflecting 165 million hectares under mandatory pesticide-reduction mandates in China and generous subsidies in India. China's National Action Plan for Pesticide Reduction targets a 40% cut in chemical use by 2030 and funds provincial training centers that demonstrate field-scale parasitoid releases. India's National Mission for Sustainable Agriculture finances 30 regional production hubs supplying microbials to smallholder cooperatives.

Africa posts the fastest 10.44% CAGR to 2031 as governments combine food-security goals with donor-funded sustainability programs. Nigeria's public-private initiative plans to serve 2 million smallholders by 2027, while Egypt builds 15 local production sites to lessen import dependence. Local capacity enables fresher products and circumvents cold-chain gaps.

Europe and North America register steady gains supported by the European Union Farm-to-Fork Strategy and premium organic sectors. The biological control market size for Europe benefits from CAP reimbursements that cover up to 70% of product costs. North America leans on a USD 134 billion organic retail channel that secures premiums of 20-40% above conventional produce, reinforcing demand for biological crop protection.

- Koppert Biological Systems B.V.

- BASF SE

- Bayer AG

- Syngenta Group

- BioFirst Group

- Valent BioSciences (Sumitomo Chemical Co., Ltd.)

- Certis Biologicals (Mitsui and Co.)

- Andermatt Group AG

- Novonesis

- Pro Farm (Bioceres Crop Solutions)

- Bioline AgroSciences Ltd (InVivo Group)

- De Sangosse

- T Stanes and Company Limited (Amalgamations Group)

- Biobee Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 Brazil

- 4.3.3 Canada

- 4.3.4 China

- 4.3.5 France

- 4.3.6 Germany

- 4.3.7 India

- 4.3.8 Indonesia

- 4.3.9 Italy

- 4.3.10 Japan

- 4.3.11 Mexico

- 4.3.12 Netherlands

- 4.3.13 Philippines

- 4.3.14 Russia

- 4.3.15 Spain

- 4.3.16 Thailand

- 4.3.17 Turkey

- 4.3.18 United Kingdom

- 4.3.19 United States

- 4.3.20 Vietnam

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Stringent bans on high-toxicity synthetic pesticides

- 4.5.2 Rising global demand for certified-organic produce

- 4.5.3 Accelerating pest resistance to conventional chemistries

- 4.5.4 Government subsidies for IPM adoption and biological inputs

- 4.5.5 Insect-rearing automation slashing cost of macrobials

- 4.5.6 Breakthrough predatory bacterial platforms targeting phytopathogens

- 4.6 Market Restraints

- 4.6.1 Short commercial shelf-life for many living products

- 4.6.2 Protracted multi-agency registration timelines

- 4.6.3 Limited sterile fermentation capacity for next-gen microbials

- 4.6.4 Micro-climate-driven efficacy variability undermining farmer confidence

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Macrobials

- 5.1.1.1 By Organism

- 5.1.1.1.1 Entamopathogenic Nematodes

- 5.1.1.1.2 Parasitoids

- 5.1.1.1.3 Predators

- 5.1.1.1 By Organism

- 5.1.2 Microbials

- 5.1.2.1 By Organism

- 5.1.2.1.1 Bacterial Biocontrol Agents

- 5.1.2.1.2 Fungal Biocontrol Agents

- 5.1.2.1.3 Other Microbials

- 5.1.2.1 By Organism

- 5.1.1 Macrobials

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Nigeria

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.1.1 By Country

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 Thailand

- 5.3.2.1.8 Vietnam

- 5.3.2.1.9 Rest of Asia-Pacific

- 5.3.2.1 By Country

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.3.1 By Country

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.4.1 By Country

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.5.1 By Country

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Rest of South America

- 5.3.6.1 By Country

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koppert Biological Systems B.V.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Syngenta Group

- 6.4.5 BioFirst Group

- 6.4.6 Valent BioSciences (Sumitomo Chemical Co., Ltd.)

- 6.4.7 Certis Biologicals (Mitsui and Co.)

- 6.4.8 Andermatt Group AG

- 6.4.9 Novonesis

- 6.4.10 Pro Farm (Bioceres Crop Solutions)

- 6.4.11 Bioline AgroSciences Ltd (InVivo Group)

- 6.4.12 De Sangosse

- 6.4.13 T Stanes and Company Limited (Amalgamations Group)

- 6.4.14 Biobee Ltd

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS