PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939125

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939125

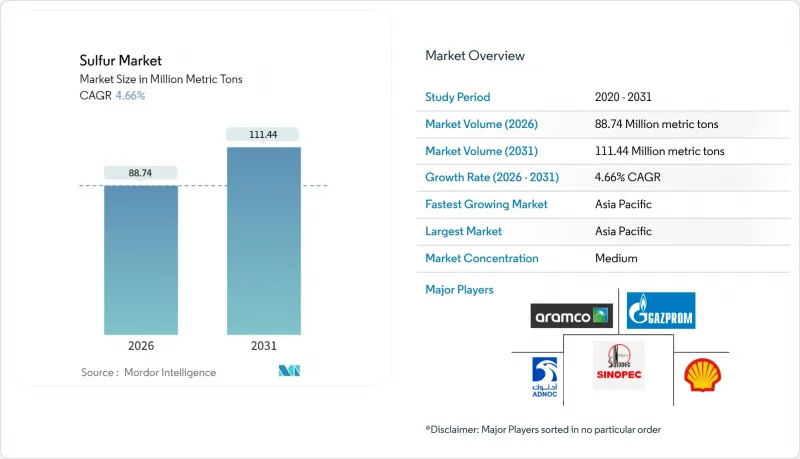

Sulfur - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Sulfur Market was valued at 84.79 Million metric tons in 2025 and estimated to grow from 88.74 Million metric tons in 2026 to reach 111.44 Million metric tons by 2031, at a CAGR of 4.66% during the forecast period (2026-2031).

Ongoing fertilizer consumption, refinery output tied to ultra-low-sulfur diesel (ULSD) mandates, and early-stage battery innovation keep the sulfur market on a steady expansion path even as environmental rules tighten. Asia-Pacific remains the geographic anchor, supplying and consuming the largest volumes thanks to population-driven food demand, refinery capacity, and industrial diversification. Solid-form material dominates logistics because it avoids the costly heating, specialized tanks, and safety controls required for molten handling. Competitive behavior skews toward integrated oil and gas conglomerates that treat sulfur recovery as a cost-offsetting by-product, yet premium outlets in lithium-sulfur batteries and sulfur-modified construction materials are motivating smaller specialists to build high-purity capacity. Persistent SOx-emission caps and high-cost molten logistics pose near-term hurdles, but they do not dilute the five-year growth outlook for the sulfur market.

Global Sulfur Market Trends and Insights

Rising Demand from Fertilizer Manufacturing

Global food-security targets keep fertilizer output high, anchoring 88.96% of sulfur market demand in 2025. India earmarked USD 68 billion to subsidize phosphate and potash nutrients in 2024, a policy that pulled large sulfur volumes into controlled-release blends. China's modernization drive supports sulfur supplementation to upgrade depleted soils, while palm-oil acreage in Indonesia and Malaysia lifts regional nutrient intensity. Precision agriculture systems require sulfur-rich micronutrient formulations, which raise the sulfur content per fertilizer unit and create a dispersed demand base that shields the sulfur market from regional shocks.

Expansion of Ultra-Low-Sulfur Diesel Refining Capacity

ULSD legislation forces refiners to extract sulfur from fuel, generating a supply that flows back into the sulfur market. New desulfurization units in Saudi Arabia's Jazan refinery added 650,000 metric tons in 2024, and Marathon Petroleum's Galveston Bay expansion supplied another 420,000 metric tons. North American and European refiners continue to invest, ensuring steady by-product output through 2030 and improving downstream access in regions that once struggled with limited sulfur availability.

Stringent SOx-Emission Regulations Across Regions

The EU Industrial Emissions Directive mandates 95% SOx abatement in sulfuric-acid plants by 2030. The U.S. National Ambient Air Quality Standards add USD 2-4 per metric ton in monitoring and scrubber costs, nudging small processors toward consolidation. China's tighter stack-emission limits introduce fines at 10% of revenue for non-compliance. These rules raise capital barriers that slow capacity additions, trimming growth momentum for the sulfur market in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Sulfur Usage in Rubber Vulcanization

- Commercialization of Lithium-Sulfur Batteries for E-Mobility

- High Logistics and Handling Cost for Molten Sulfur

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid products represented 80.62% of the sulfur market share in 2025 and are tracking a 5.08% CAGR to 2031. Handling ease, lower insurance premiums and the absence of heated storage explain the preference among fertilizer producers lacking specialized infrastructure. The sulfur market size for solid material is poised to rise further as automated loading and dust-suppression upgrades lower operational risks.

Granular and prilled formats also improve product integrity during transport, align with ISO 14001 management systems and reduce environmental exposure. Liquid sulfur stays limited to large sulfuric-acid complexes where molten feed integrates directly into process lines, but its high logistics bill caps broad adoption. Solid sulfur therefore keeps its leadership as emerging battery and construction users also specify granulated inputs.

The Sulfur Market Report is Segmented by Form (Solid and Liquid), Finishing-Process Technology (Granules, Pastilles, and Prilling), End-User Industry (Fertilizer, Chemical Processing, Metal Manufacturing, Rubber Processing, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Metric Tons).

Geography Analysis

Asia-Pacific held 39.40% of global volume in 2025 and is pacing a 5.55% CAGR to 2031. China consumed 28.5 million metric tons, driven by phosphate fertilizer targets aligned with grain self-sufficiency goals. India's farm-support schemes and Southeast Asian plantation crops push fertilizer tonnage upward, making the region the core growth engine of the sulfur market.

North America is propelled by ULSD investments and lithium-sulfur battery plants in Nevada and Texas, placing incremental pull on regional supply, anchoring a balanced demand-supply position. Europe advances on precision farming and regulatory shifts that favor sulfur-based soil additives over synthetic chemicals. Middle East and Africa expand refinery recovery and promote agriculture programs that enlarge fertilizer use, widening geographic diversification for the sulfur market.

- ADNOC

- China Petroleum & Chemical Corporation (Sinopec)

- Flexsys America L.P.

- Gazprom International Limited

- Indian Oil Corporation Ltd

- Marathon Petroleum Corporation

- QatarEnergy LNG

- Saudi Arabian Oil Co.

- Shell plc

- Suncor Energy Inc.

- Tengizchevroil LLP

- Valero

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from fertilizer manufacturing

- 4.2.2 Expansion of ultra-low-sulfur diesel (ULSD) refining capacity

- 4.2.3 Increasing sulfur usage in rubber vulcanization

- 4.2.4 Commercialization of lithium-sulfur batteries for e-mobility

- 4.2.5 Growing adoption of sulfur-modified asphalt and concrete in circular construction

- 4.3 Market Restraints

- 4.3.1 Stringent SOx-emission regulations across regions

- 4.3.2 High logistics and handling cost for molten sulfur

- 4.3.3 Declining sulfur recovery as refineries decarbonize and desulfurize less crude

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Solid

- 5.1.2 Liquid

- 5.2 By Finishing-Process Technology

- 5.2.1 Granules

- 5.2.2 Pastilles

- 5.2.3 Prilling

- 5.3 By End-User Industry

- 5.3.1 Fertilizer

- 5.3.2 Chemical Processing

- 5.3.3 Metal Manufacturing

- 5.3.4 Rubber Processing

- 5.3.5 Other End-User Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ADNOC

- 6.4.2 China Petroleum & Chemical Corporation (Sinopec)

- 6.4.3 Flexsys America L.P.

- 6.4.4 Gazprom International Limited

- 6.4.5 Indian Oil Corporation Ltd

- 6.4.6 Marathon Petroleum Corporation

- 6.4.7 QatarEnergy LNG

- 6.4.8 Saudi Arabian Oil Co.

- 6.4.9 Shell plc

- 6.4.10 Suncor Energy Inc.

- 6.4.11 Tengizchevroil LLP

- 6.4.12 Valero

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment