PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939643

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939643

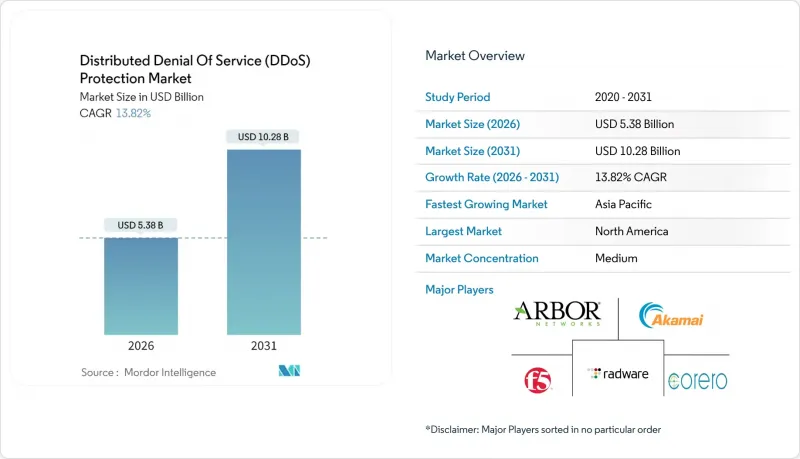

Distributed Denial Of Service (DDoS) Protection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

DDoS protection market size in 2026 is estimated at USD 5.38 billion, growing from 2025 value of USD 4.73 billion with 2031 projections showing USD 10.28 billion, growing at 13.82% CAGR over 2026-2031.

This expansion is fueled by the mounting frequency of multi-vector, terabit-scale incidents, strengthened regulatory mandates, and the widespread embrace of hybrid and cloud-based mitigation models. Solution-centric offerings maintained dominance with 61.23% share in 2024, underscoring enterprise demand for integrated, programmable defenses. Cloud-first deployments accounted for nearly half the addressable opportunity, yet hybrid architectures are gaining ground as organizations balance latency, control, and compliance. Regional dynamics remain pivotal: North America led with 39.34% revenue share in 2024, while Asia Pacific is advancing at a 14.89% CAGR, driven by rapid 5G rollouts and surging IoT adoption.

Global Distributed Denial Of Service (DDoS) Protection Market Trends and Insights

Escalating frequency of multi-vector attacks

A record 6.3 Tbps event in 2025 highlighted the jump from volumetric floods to blended protocol and application-layer campaigns, overwhelming legacy rule-based appliances and escalating procurement of adaptive, AI-driven platforms. Communication service providers and financial institutions remain high-value targets, and global regulators now require demonstrated resilience for critical infrastructure operators.

Rapid migration to cloud and hybrid mitigation models

Elastic, always-on cloud scrubbing has become indispensable as short-burst attacks spike; however, latency-sensitive workloads keep on-premises defenses relevant, accelerating hybrid demand. Partnerships between hyperscale clouds and security specialists are bridging skills gaps for SMEs while meeting emerging compliance obligations.

High TCO of on-prem appliances for SMEs

Capex-heavy hardware plus ongoing signature updates remain prohibitive for smaller enterprises, steering demand toward subscription-based cloud scrubbing paired with managed SOC services.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of IoT-, 5G-, and edge-connected devices

- AI-powered "DDoS-as-a-Service" marketplaces lowering entry barriers

- Shortage of skilled cybersecurity professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions commanded 60.65% revenue in 2025 as enterprises sought unified, programmable defenses capable of spanning L3/4 volumetric floods and L7 application abuses. Within this umbrella, network-layer protection retained the largest slice, yet advanced bot mitigation is forecast to rise at a 15.05% CAGR, driven by AI-enabled bots that mimic legitimate user behavior. Vendors are embedding machine-learning classifiers, device fingerprinting, and real-time challenge mechanisms to blunt credential-stuffing and inventory hoarding. Services-managed and professional-continue to gain relevance as organizations consolidate suppliers for compliance reporting and 24X7 monitoring. The interplay of solutions and services underscores a shift toward outcome-based contracting across the DDoS protection market.

Growing adoption of hybrid topologies demands orchestration between on-premises hardware, cloud scrubbing centers, and containerized network functions. As offerings converge, differentiation pivots on API-centric integration, attack-forensics depth, and zero-trust alignment. Solution vendors that blend behavioral analytics with actionable intelligence are positioned to capitalize on rising regulatory pressure for demonstrable resiliency across critical sectors.

Cloud-based defenses captured 49.02% of the DDoS protection market size in 2025, offering elastic bandwidth pools and global anycast routing to absorb multi-Tbps assaults. Always-on models ensure response within seconds, a necessity amid sub-minute "pulse" attacks. Meanwhile, hybrid architectures are projected to expand at a 15.25% CAGR through 2031 as enterprises merge low-latency, on-premises detection with cloud-scale scrubbing during surge periods. This flexible posture satisfies jurisdictional data constraints while minimizing capex and operational complexity.

On-premises appliances retain niche traction among financial trading platforms, defense agencies, and media broadcasters that demand micro-second mitigation. However, even these verticals are layering cloud capacity for volumetric overflow. Continuous API-driven telemetry exchange between sites, scrubbing nodes, and SIEM platforms is becoming table stakes across the DDoS protection market.

The Distributed Denial of Service (DDoS) Protection Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (Government and Defense, Banking, Financial Services and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD),

Geography Analysis

North America's 39.05% share underscores a mature yet volatile landscape. High-value targets include finance, SaaS, and energy. CISA directives increasingly require real-time telemetry sharing and zero-trust alignment, prompting deeper vendor-customer collaboration on incident response. Investments prioritize encrypted-traffic inspection and machine-learning-driven anomaly scoring.

Asia Pacific exhibits the strongest growth trajectory at 14.65% CAGR. Digital economies are onboarding tens of millions of new broadband and mobile subscribers annually, amplifying botnet recruitment potential. Regional telcos partner with security vendors to deploy edge scrubbing nodes across 5G core networks, reducing hop latency and improving customer experience. Regulatory agencies in Japan and Australia now mandate quarterly resilience reporting for critical infrastructure operators, reinforcing demand across the DDoS protection market.

Europe balances stringent privacy mandates with elevated attack sophistication. NIS2 imposes fines up to 2% of global turnover for inadequate defenses, accelerating migration toward certified, multi-tenant mitigation services. Central and Eastern European utilities face politically motivated flood attacks, driving adoption of AI-guided traffic classification coupled with sovereign data-hosting guarantees. Latin America, the Middle East, and Africa represent emerging vectors both for botnet origination and targeted campaigns, necessitating localized, context-aware defense strategies within the DDoS protection market.

- NETSCOUT Systems, Inc.

- Akamai Technologies, Inc.

- F5, Inc.

- Imperva, Inc.

- Radware Ltd.

- Corero Network Security plc

- Neustar, Inc.

- Cloudflare, Inc.

- Nexusguard Limited

- DOSarrest Internet Security Limited

- VeriSign, Inc.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- A10 Networks, Inc.

- Fastly, Inc.

- Alibaba Cloud Computing Co., Ltd.

- StackPath, LLC

- GCore Labs S.A.

- Link11 GmbH

- Lumen Technologies, Inc.

- Sucuri, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating frequency of multi-vector, terabit-scale attacks

- 4.2.2 Rapid migration to cloud and hybrid mitigation models

- 4.2.3 Expansion of IoT-, 5G- and edge-connected devices

- 4.2.4 AI-powered "DDoS-as-a-Service" marketplaces lowering entry barriers

- 4.2.5 Critical-infrastructure regulations mandating resiliency (e.g., NIS2, CISA)

- 4.2.6 Adoption of programmable SDN-based scrubbing at the network edge

- 4.3 Market Restraints

- 4.3.1 High TCO of on-prem appliances for SMEs

- 4.3.2 Shortage of skilled cyber-security professionals

- 4.3.3 Rising share of encrypted attack traffic limiting visibility

- 4.3.4 Risk of false-positive mitigation causing self-inflicted downtime

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Use Case and Case Studies

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Network-layer protection

- 5.1.1.2 Application-layer protection

- 5.1.1.3 DNS protection

- 5.1.1.4 Advanced bot mitigation

- 5.1.2 Service

- 5.1.2.1 Professional services

- 5.1.2.2 Managed services

- 5.1.1 Solution

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 Government and Defense

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Information Technology and Telecommunications

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Retail and E-commerce

- 5.4.6 Media and Entertainment

- 5.4.7 Energy and Utilities

- 5.4.8 Manufacturing

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NETSCOUT Systems, Inc.

- 6.4.2 Akamai Technologies, Inc.

- 6.4.3 F5, Inc.

- 6.4.4 Imperva, Inc.

- 6.4.5 Radware Ltd.

- 6.4.6 Corero Network Security plc

- 6.4.7 Neustar, Inc.

- 6.4.8 Cloudflare, Inc.

- 6.4.9 Nexusguard Limited

- 6.4.10 DOSarrest Internet Security Limited

- 6.4.11 VeriSign, Inc.

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Microsoft Corporation

- 6.4.14 Google LLC

- 6.4.15 Check Point Software Technologies Ltd.

- 6.4.16 Fortinet, Inc.

- 6.4.17 A10 Networks, Inc.

- 6.4.18 Fastly, Inc.

- 6.4.19 Alibaba Cloud Computing Co., Ltd.

- 6.4.20 StackPath, LLC

- 6.4.21 GCore Labs S.A.

- 6.4.22 Link11 GmbH

- 6.4.23 Lumen Technologies, Inc.

- 6.4.24 Sucuri, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment